Key Stats

- Current price: ~$75 (May 8, 2026)

- Q1 2026 gross profit: $2.91B, +27% YoY

- Q1 2026 adjusted diluted EPS: $0.85, +52% YoY

- Q1 2026 adjusted operating income: $728M, +56% YoY; 25% margin (all-time high)

- Q1 2026 adjusted EBITDA: $1.0B (all-time high)

- Full-year 2026 gross profit guidance (raised): $12.33B, +19% YoY

- Full-year 2026 adjusted operating income guidance (raised): $3.34B, 27% margin

- Full-year 2026 adjusted diluted EPS guidance: $3.85, +62% YoY

- TIKR model price target: $138 | Implied upside: ~85% over 4.6 years (14% annualized)

Block Stock Delivers All-Time Highs on Gross Profit and Margins in Q1 2026

Block stock (XYZ) surged 7% on May 8 after the company reported Q1 2026 adjusted diluted EPS of $0.85, up 52% year-over-year, and gross profit of $2.91B, up 27% year-over-year, both exceeding its own guidance.

Cash App drove the headline result, with gross profit growing 38% year-over-year as Commerce Enablement and Financial Solutions accelerated simultaneously.

Monthly transacting actives grew 4% year-over-year to approximately 59 million, with inflows per transacting active up 10% and Primary Banking Actives rising 18% to 9.7 million.

According to CFO Amrita Ahuja on the Q1 2026 earnings call, adjusted operating income reached $728M at a 25% margin, and adjusted EBITDA crossed $1.0B — each representing all-time highs on both a dollar and margin basis.

Square delivered gross profit growth of 9% and GPV growth of 13% year-over-year in Q1, with constant-currency GPV up 12%.

Food and beverage GPV grew 21% year-over-year and mid-market GPV grew 22%, both the strongest growth rates since Q1 2023, according to Ahuja on the Q1 2026 call.

International GPV grew 35% year-over-year, or 26% on a constant-currency basis, as Block expanded its field sales presence across the U.S., U.K., Australia, and Canada.

Block raised its full-year 2026 gross profit guidance to $12.33B (19% growth), up one percentage point from its prior outlook, and raised adjusted operating income guidance to $3.34B at 27% margin, also up one point.

Full-year adjusted diluted EPS guidance was set at $3.85, representing 62% growth year-over-year.

For Q2 2026, Block guided to gross profit of $3.04B (+20% YoY), adjusted operating income of $740M (+35% YoY), and adjusted diluted EPS of $0.86 (+39% YoY).

Moneybot reached general availability across Cash App, and Managerbot was enabled for more than 1 million sellers, with full rollout to all Square sellers targeted for June 2026, according to CEO Jack Dorsey on the Q1 2026 call.

Neighborhoods, Block’s seller-consumer connection program, scaled to $320M in annualized GPV as of March 2026, up 190% since December, with April adding more sellers than the program’s entire prior history.

According to Owen Jennings, Business Lead, on the Q1 2026 call, production code changes per engineer at Block increased more than 2.5x from January to April, with production changes by non-engineers up nearly 60% over the same period.

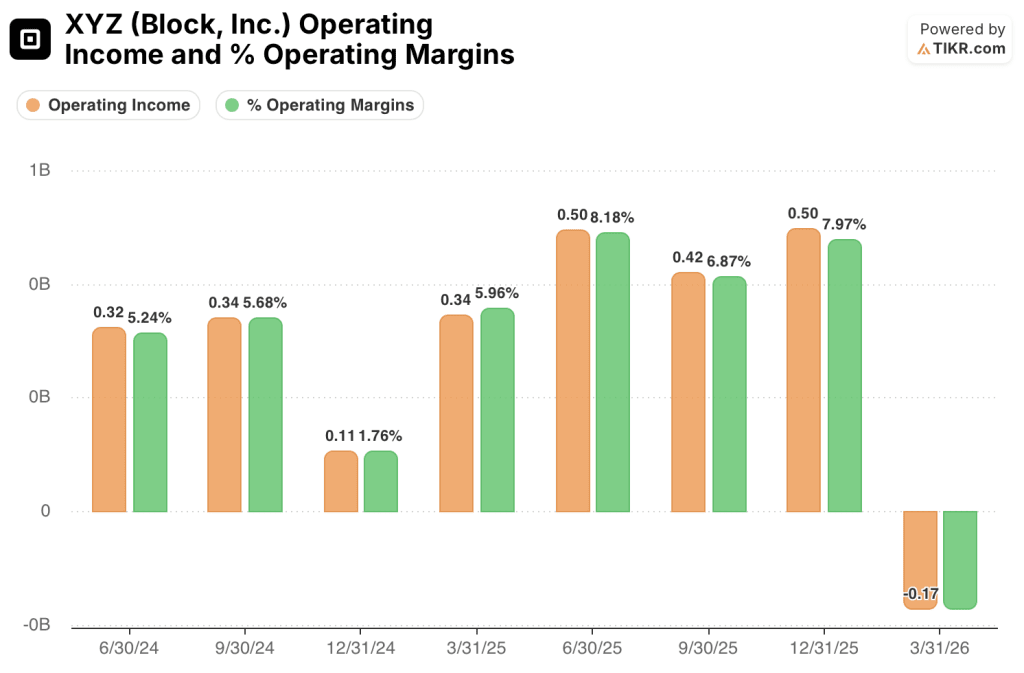

Income Statement: Gross Profit Compounding as GAAP Operating Loss Widens

The income statement tells two concurrent stories: gross profit expanding at an accelerating rate across eight consecutive quarters, while operating expenses in Q1 2026 produced a GAAP operating loss.

Gross profit grew from $2.25B in Q2 2024 to $2.27B, $2.33B, $2.30B, $2.55B, $2.68B, $2.89B, and $2.92B through Q1 2026, with gross margin expanding from 37% in Q2 2024 to 48% in Q1 2026.

YoY gross profit growth accelerated from 9% in Q3 2024 to 14% in Q4 2024, then to 13%, 18%, 24%, and 27% in the four most recent quarters.

Total operating expenses surged to $3.09B in Q1 2026 from $2.39B in Q4 2025 and $1.93B in both Q2 and Q3 2024, driven by increases across SG&A ($1.51B), R&D ($1.04B), and other operating expenses ($500M).

That operating expense spike pushed operating income from $500M in Q4 2025 to a loss of $172M in Q1 2026, with operating margin swinging from 8% to (3%).

According to Ahuja on the Q1 2026 call, excluding hardware costs (a key customer acquisition driver), Square gross profit growth was 11% in Q1, much closer to the 12% GPV growth rate on a constant-currency basis.

Block’s consumer lending portfolio showed improving credit quality by cohort: customers on the platform 13-plus months carried a 2.67% risk loss rate versus 3.16% for the newest customers, per Ahuja on the Q1 2026 call.

What Does the Valuation Model Say?

The TIKR model sets a price target of $138 for Block stock, implying approximately 85% total return from the current price of ~$75, or about 14% annualized over ~5 years.

The mid-case model assumes a revenue CAGR of around 8% through 2035 and a net income margin of ~11%, reaching a forecast stock price of $172 by December 2034 under that scenario.

The low case assumes 7% revenue CAGR and near 10% net income margin, yielding a forecast price of $133 and a 78% total return; the high case assumes ~8% CAGR and 12% margin, implying a forecast price of $215 and 187% total return.

Q1’s gross profit acceleration and margin records strengthen the bull case, but the GAAP operating loss and Q1 operating expense jump introduce near-term execution risk that the model’s margin assumptions will need to absorb.

Block stock’s risk/reward is asymmetric to the upside if gross profit growth sustains at mid-to-high 20% rates while the elevated operating cost base normalizes.

The Q1 report reinforces the investment case: gross profit and adjusted profitability hit all-time highs simultaneously, guidance went up, and AI-led velocity is accelerating. The open question is whether the GAAP operating loss in Q1 is a one-quarter investment spike or the beginning of a sustained cost expansion.

What Has to Go Right

- Cash App gross profit growth, at 38% YoY in Q1, must remain elevated as Borrow growth normalizes in the back half of 2026; management guided to continued low single-digit active growth and maintained its full-year 19% gross profit outlook

- Neighborhoods must convert its April seller inflection into meaningful Cash App active growth in H2 2026, as Dorsey stated on the Q1 call that the program is expected to be more than a rounding error on actives by the second half

- Square ISO partnerships, now at 140-plus active partners, must continue scaling; the volume of deals signed through ISOs already equates to approximately 70 field sales reps, per Jennings on the Q1 call

- The mid-case TIKR model assumption of 11.2% net income margin requires GAAP operating expenses to moderate meaningfully from Q1’s $3.09B level

What Could Still Go Wrong

- The Q1 2026 GAAP operating loss of $172M and operating margin of (3%) represent a sharp reversal from the $500M operating income and 8% margin posted in both Q3 and Q4 2025, and operating expenses must compress for the model’s margin assumptions to hold

- Borrow normalization is explicit in management guidance; Ahuja noted on the Q1 call that tougher comparisons begin in Q2, and Borrow has been driving more than half of Cash App gross profit growth

- Square gross profit growth (9% in Q1) continues to lag GPV growth (13%), and the expected convergence in H2 2026 depends on pricing and packaging initiatives that have not yet fully scaled

- The TIKR model’s revenue CAGR assumption of 7.7% (mid case) runs well below Block’s current gross profit growth trajectory, meaning any deceleration in gross profit growth materially compresses the upside

Should You Invest in Block, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Block, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Block, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze XYZ stock on TIKR for Free →