Key Stats

- Current Price: ~$16 (May 8, 2026 close: $15.69, up 11% on earnings day)

- Q1 2026 Adjusted Revenue: $2.8B, up 118% YoY (from $1.3B in Q1 2025)

- Q1 2026 Adjusted EPS: $0.15, up from $0.04 in Q1 2025

- Q1 2026 Adjusted EBITDA: $738M, margin at 26% vs. 13% in Q1 2025

- Q2 2026 Adjusted Revenue Guidance: $2.7B to $2.9B

- Mr. Cooper Expense Synergies: $400M annualized, now expected fully realized by end of 2026 (one year ahead of original plan)

- TIKR Model Price Target: ~$19 (mid-case)

- Implied Upside: ~19% over ~5 years (4% annualized)

Rocket Companies Stock Q1 2026 Earnings Breakdown

Rocket Companies stock (RKT) reported Q1 2026 adjusted revenue of $2.8B, surpassing the high end of its guidance range and more than doubling year over year from $1.3B in Q1 2025.

Adjusted diluted EPS came in at $0.15, up from $0.04 in the year-ago quarter and above the $0.11 posted in Q4 2025.

Adjusted EBITDA reached $738M, up from $592M last quarter, with margins expanding to 26% from 23% in Q4 2025 and 13% in Q1 2025.

According to CEO Varun Krishna on the Q1 2026 earnings call, this was Rocket’s most profitable quarter in four years.

Net rate lock volume hit $49B, a 19% sequential increase, with market share gains in both purchase and refinance channels quarter over quarter and year over year.

The servicing portfolio, now carrying a $2.1T unpaid principal balance, generated over $1B in servicing fee income during the quarter, according to Krishna on the Q1 2026 earnings call.

Gain on sale margin, excluding correspondent, reached 322 basis points, the highest since Q1 2021, according to President and CFO Brian Brown on the Q1 2026 earnings call.

54% of refinance closings came from existing serviced clients, with recapture rates on Mr. Cooper-originated loans reaching an all-time high, according to Brown on the Q1 2026 earnings call.

The Redfin attach rate is approaching 50%, with the current rate hovering around 45% and continuing to rise, according to Brown on the Q1 2026 earnings call.

Rocket Pro added nearly 180 new broker partners in two months following the launch of Jupiter, a white-labeled loan origination system offered at no cost, collectively representing a $5B annual closed loan volume opportunity, according to Brown on the Q1 2026 earnings call.

AI-powered purchase pre-approvals, launched in late February, now account for 10% of all pre-approvals, with 40% completed outside traditional business hours and conversion running 33% higher than the non-AI baseline, according to Krishna on the Q1 2026 earnings call.

AI prospecting has reduced loan officer prospecting time from up to two hours per day to zero, with conversion improving by double digits, according to Krishna on the Q1 2026 earnings call.

The Compass partnership has generated nearly 10,000 exclusive Redfin listings and approximately 30,000 leads into the Compass ecosystem, with one in four purchase loans in the broker channel now sourced from Compass agents, according to Krishna on the Q1 2026 earnings call.

Origination capacity has reached $300B, double the 2024 baseline, achieved two years ahead of the original schedule with several hundred fewer production team members, according to Brown on the Q1 2026 earnings call.

Loans closed per team member are up 75% compared to two years ago, according to Brown on the Q1 2026 earnings call.

For Q2 2026, Rocket guided adjusted revenue of $2.7B to $2.9B, with expenses expected at approximately $2.2B at the midpoint (excluding amortization, stock-based compensation, and one-time acquisition costs), roughly $60M lower than Q1 due to ongoing synergy realization.

Rocket Companies Stock: What the Income Statement Shows

The Q1 2026 income statement tells a sharp operating leverage story: revenue nearly tripled versus a year ago while the cost structure came down sequentially.

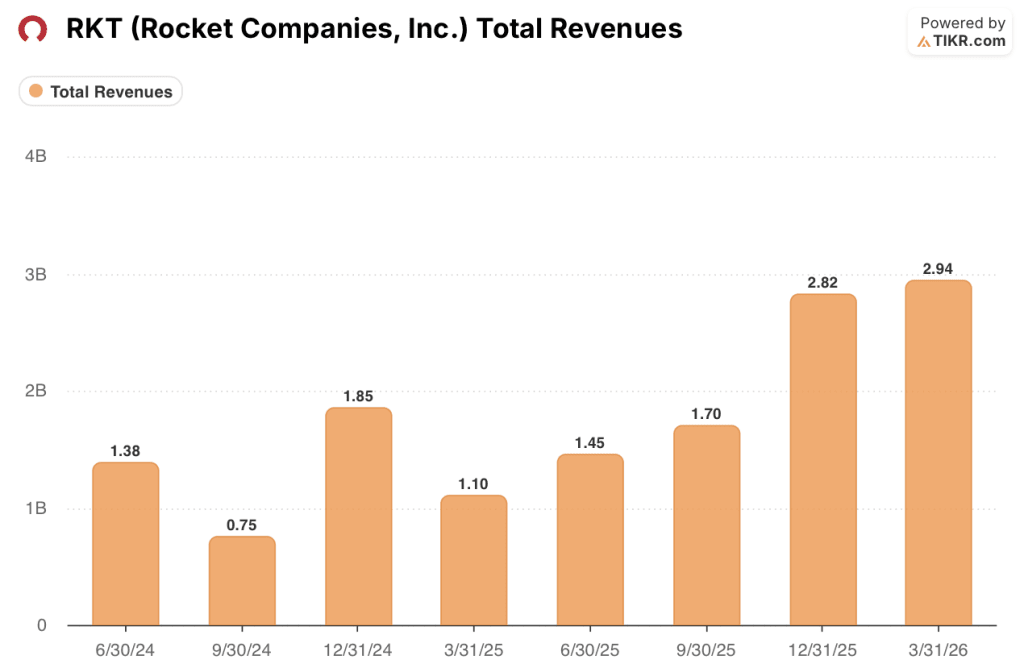

Total revenues reached $2.94B in Q1 2026, up from $2.82B in Q4 2025, $1.70B in Q3 2025, $1.45B in Q2 2025, and $1.10B in Q1 2025, a consistent step-up across every quarter of the past year.

The revenue expansion reflects the weight of the Mr. Cooper and Redfin acquisitions, which meaningfully changed the composition of the top line beginning in Q4 2025.

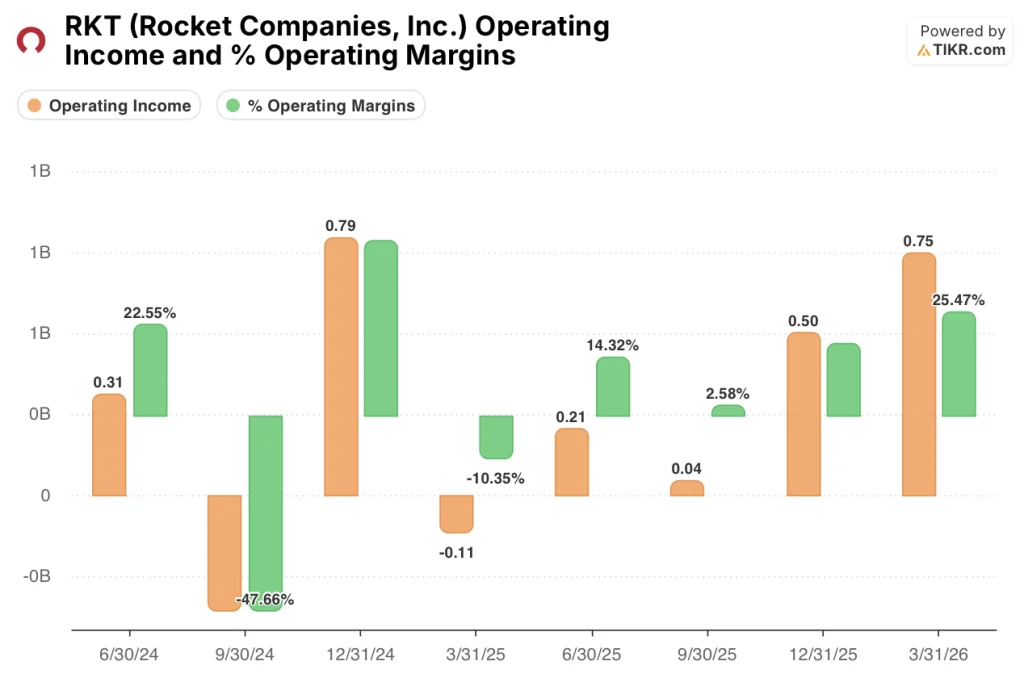

Operating income jumped to $750M in Q1 2026, up from $500M in Q4 2025, $40M in Q3 2025, and $210M in Q2 2025, with the operating margin reaching 26% versus 18% in Q4 2025 and just 3% in Q3 2025.

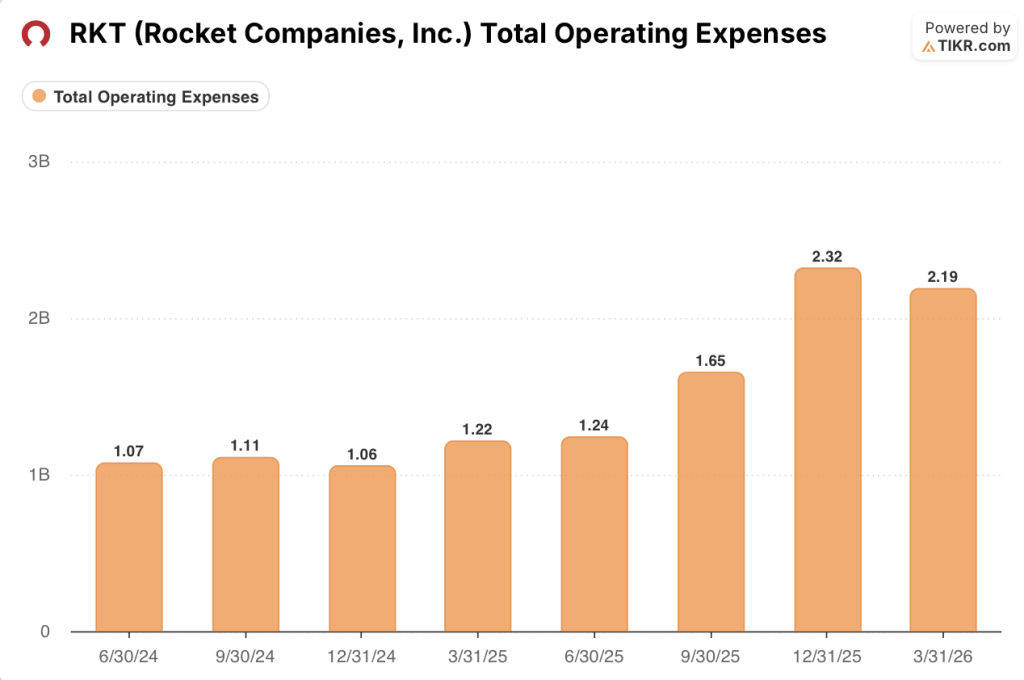

Total operating expenses declined to $2.19B in Q1 2026 from $2.32B in Q4 2025, reflecting early realization of Mr. Cooper synergies and the benefit of AI-driven efficiency improvements confirmed by Brown on the Q1 2026 earnings call.

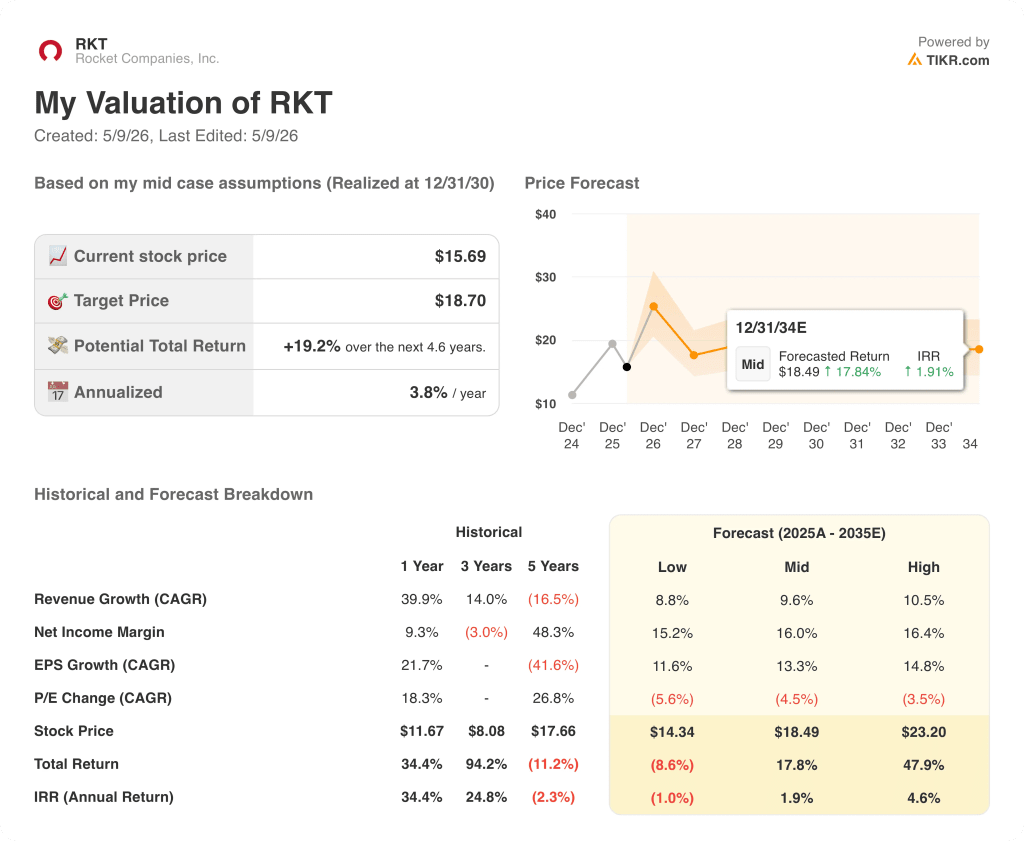

What Does the Valuation Model Say?

The TIKR model prices Rocket Companies stock at a mid-case target of ~$19, implying approximately 19% total upside from the current price of ~$16 over 4.6 years, or 3.8% annualized.

The model’s mid-case assumes a revenue CAGR of 9.6% and a net income margin of 16% through the forecast period.

Q1’s result strengthens the case for both assumptions: the revenue trajectory is running well ahead of that growth rate in the near term, and the 26% EBITDA margin posted this quarter gives the net income margin target real grounding.

The investment case for Rocket Companies stock is incrementally stronger after this report, with operating leverage arriving faster than expected and the synergy timeline pulling forward by a full year.

What the Earnings Report Hinges On: Whether Rocket’s AI-driven efficiency gains and servicing recapture rates sustain through a higher-rate, slower-volume environment in 2026.

What Has to Go Right

- Mortgage rates must stabilize or decline to unlock the rate-sensitive revenue category, which management identified as the greatest source of upside in a rate drop; the pipeline of preapproved purchase clients is at an all-time high

- Mr. Cooper synergies must phase in on schedule: $75M realized through Q1, another $100M targeted by end of Q2, and $225M in H2 2026

- Redfin attach rates must continue toward 50% from the current 45%, extending the platform’s less rate-sensitive revenue base

- AI origination capacity at $300B must translate into sustained gain on sale margin at or near the 322 basis point level posted in Q1 2026

What Could Still Go Wrong

- The spring home buying season is off to a slow start, with homes averaging 51 days on market, the longest stretch since 2019, limiting near-term purchase volume upside

- Mortgage rates are approximately 50 basis points above February lows, pressuring rate-sensitive refinance volumes that management acknowledges have pulled back meaningfully into Q2

- At 3.8% annualized, the TIKR mid-case return is modest for investors expecting rate-driven upside to arrive in 2026; the high-case scenario requires execution on both revenue growth and synergy realization simultaneously

- Gain on sale margin faces downward mix-shift pressure as Pro volumes grow during a purchase-heavy season, per Brown on the Q1 2026 earnings call

Should You Invest in Rocket Companies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Rocket Companies stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Rocket Companies, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze RKT stock on TIKR for Free →