Key Stats

- Current price: ~$94 (FWON.K, as of May 8, 2026)

- Q1 2026 revenue: $711M, +59% YoY

- Q1 2026 EBIT: $64M vs. ($67M) loss in Q1 2025

- Q1 2026 net income: $57M vs. $83M in Q1 2025

- Q1 2026 adjusted OIBDA: $181M, +148% YoY

- Full-year team payment leverage: ~200 bps improvement expected (per management guidance)

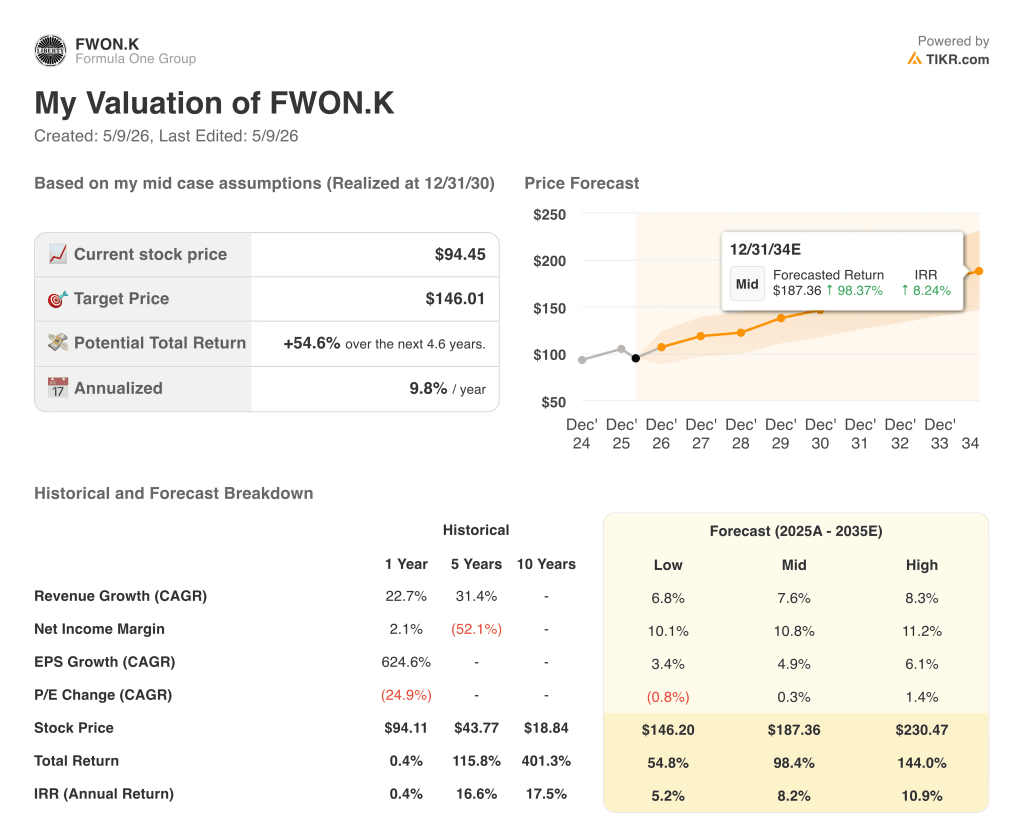

- TIKR model price target: ~$146 (mid case, 12/31/30)

- Implied upside: ~55% over 4.6 years (~10% annualized)

Formula One Group Stock: Q1 2026 Earnings Breakdown

Formula One Group stock (FWONK) reported Q1 2026 revenue of $711M, up 59% year over year, as the company held three races in the quarter versus two in Q1 2025.

Adjusted OIBDA came in at $181M, more than doubling from $73M in the prior-year period, driven by an additional race event and underlying contractual fee increases across all revenue streams, according to Chief Accounting and Principal Financial Officer Brian Wendling on the Q1 2026 earnings call.

F1 media rights and sponsorship revenue both benefited from the calendar shift: with three of 22 scheduled races recognized in Q1 (roughly 14% of season-based revenue) versus two of 24 races in Q1 2025 (roughly 8%), a larger proportion of season-based revenue flowed into the quarter.

Hospitality revenue outpaced expectations, driven by strong Paddock Club performance, with over 65,000 tickets already sold to date and the Paddock Club nearly sold out for the remainder of the 2026 season, according to Formula One President and CEO Stefano Domenicali on the earnings call.

Sponsorship revenue also grew from new partners including Standard Chartered, with Domenicali noting on the call that renewal momentum is accelerating, with partners now entering negotiations well ahead of contract expiry dates.

Formula One Group stock carries a meaningful calendar risk into Q2: the Bahrain and Saudi Arabian Grand Prix were not held in April due to the Middle East situation, and Q2 is expected to feature only five races versus nine held in Q2 2025, according to Wendling.

Management is evaluating the possibility of rescheduling one of the two cancelled races to the end of the season, which would be incremental upside relative to the current 22-race base case.

F1 TV revenue grew 28% year over year, and YouTube content generated almost 600 million views through the Japanese Grand Prix, up 46% year over year, according to Domenicali on the earnings call.

Apple’s first season as the exclusive U.S. media rights partner delivered higher average viewership across track sessions in the first three races relative to last season, with the viewer base skewing younger and more female, according to Domenicali.

Formula One Group stock also received a significant long-term commercial anchor: F1 announced a five-year renewal with Sky in the U.K. through 2034 and in Italy through 2032, locking in one of the sport’s largest broadcast partners for the next decade.

Retail sales grew 125% during the quarter, driven by the Disney and F1 partnership launch in the Asia-Pacific region and specialty F1 Disney stores deployed at the Chinese and Japanese Grand Prix fan zones.

Net leverage at Liberty Media stood at 3x at quarter end, with $862M of cash at F1 and total principal debt of approximately $5B, including $3.3B at F1, according to Wendling.

Formula One Group Stock: Financials

The income statement tells a year-over-year recovery story, with operating income swinging from a $60M loss in Q1 2025 to $120M in Q1 2026, though the sequential picture from the stronger Q4 periods reveals a predictable race-calendar rhythm.

Total revenues were $440M in Q1 2025, a quarter with only two races, making direct YoY comparison less informative than looking at the full trend.

Revenue moved from $580M in Q1 2024 (two races) to $980M in Q2 2024, $900M in Q3 2024, $1.13B in Q4 2024, $440M in Q1 2025, $1.34B in Q2 2025, $1.08B in Q3 2025, and $711M in Q1 2026 (three races), reflecting a business where quarterly revenue is a function of race count and mix more than underlying demand erosion or acceleration.

Gross margin in Q1 2026 was 26%, below the Q2 2025 peak of 35% and the Q3 2025 level of 38%, which is consistent with race-mix effects as hospitality, freight, and travel costs scale with events held.

Operating margin reached 9% in Q1 2026, recovering sharply from the (13%) recorded in Q1 2025, though it remains below the 21% delivered in Q2 2025, when nine races drove higher operating leverage.

SG&A was elevated in Q1 2026 due to unfavorable foreign exchange rates, higher personnel costs, and technology investment, partially offset by lower marketing expense compared to Q1 2025, which included costs related to F1’s 75th anniversary event, according to Wendling on the earnings call.

The full-year 200 basis point improvement in team payment leverage, which management confirmed remains on track, is the key operating income lever for 2026 and is best evaluated on a full-year basis given quarterly fluctuations in team payments as a percentage of adjusted OIBDA.

What Does the Valuation Model Say?

TIKR’s valuation model prices Formula One Group stock at a mid-case target of ~$146 as of December 31, 2030, implying approximately 55% total upside from the current price of ~$94, or roughly 10% annualized over 4.6 years.

The mid-case assumes a revenue CAGR of 7.6% and a net income margin of 11% through 2035.

Q1 2026 demonstrated that the core commercial engine is intact: sponsorship momentum, broadcast partnerships, and premium hospitality demand all reinforced the model’s underlying revenue growth assumptions.

The two cancelled Middle East races introduce a near-term drag, and Q2 2026 will see a significant revenue shortfall versus Q2 2025 due to five versus nine races, which creates quarterly noise around an otherwise solid fundamental thesis.

At current levels, Formula One Group stock offers a mid-case path to ~55% upside with a base that management is actively reinforcing through long-term contract renewals and hospitality expansion, making the risk/reward modestly favorable for investors with a multi-year horizon.

The Q1 beat arrived despite calendar disruption, but whether that momentum extends to a full-year result depends entirely on how the Middle East situation resolves and whether management can execute on rescheduling.

What Has to Go Right

- A rescheduled Saudi Arabian or Bahrain Grand Prix in late 2026 would recover race promotion, hospitality, and freight revenue that was lost in Q2, with management explicitly noting a potential end-of-season slot is being evaluated

- The Apple partnership must sustain and grow U.S. viewership: early data from three races showed higher average viewership than the prior linear season, but the full-season impact on F1 TV revenue and downstream sponsorship pricing is not yet visible

- Paddock Club expansion at Silverstone, Austin, and Monza, alongside House 44 (already sold out at eight race locations), must convert elevated demand into incremental high-margin hospitality revenue that supports the 200 bps team payment leverage target

- The Sky renewal through 2034 (U.K.) and 2032 (Italy) must anchor broadcast revenue per race without displacing open-market upside in other territories

What Could Still Go Wrong

- Q2 2026 is structurally impaired: with only five races expected versus nine in Q2 2025, the quarter will show a material year-over-year revenue decline that could create investor concern around the full-year guide

- MotoGP’s cost structure carries foreign exchange exposure with no revenue offset: Wendling flagged that rising fuel costs flow through cost of revenue at MotoGP without a corresponding top-line pass-through mechanism, unlike F1 where freight and fuel costs are passed to teams

- Formula One Group stock carries $5B in total debt, including $3.3B at F1 and $1.2B at MotoGP, and net leverage of 3x could increase modestly during Q2 on lower trailing-12-month OIBDA from the race cancellations

- SG&A remains elevated from FX headwinds, personnel growth, and technology investment, and these costs are front-end loaded; if revenue recovery in the second half is partial rather than full, operating margin improvement could lag the full-year guide

Should You Invest in Formula One Group?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Formula One Group stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Formula One Group stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FWONK stock on TIKR for Free →