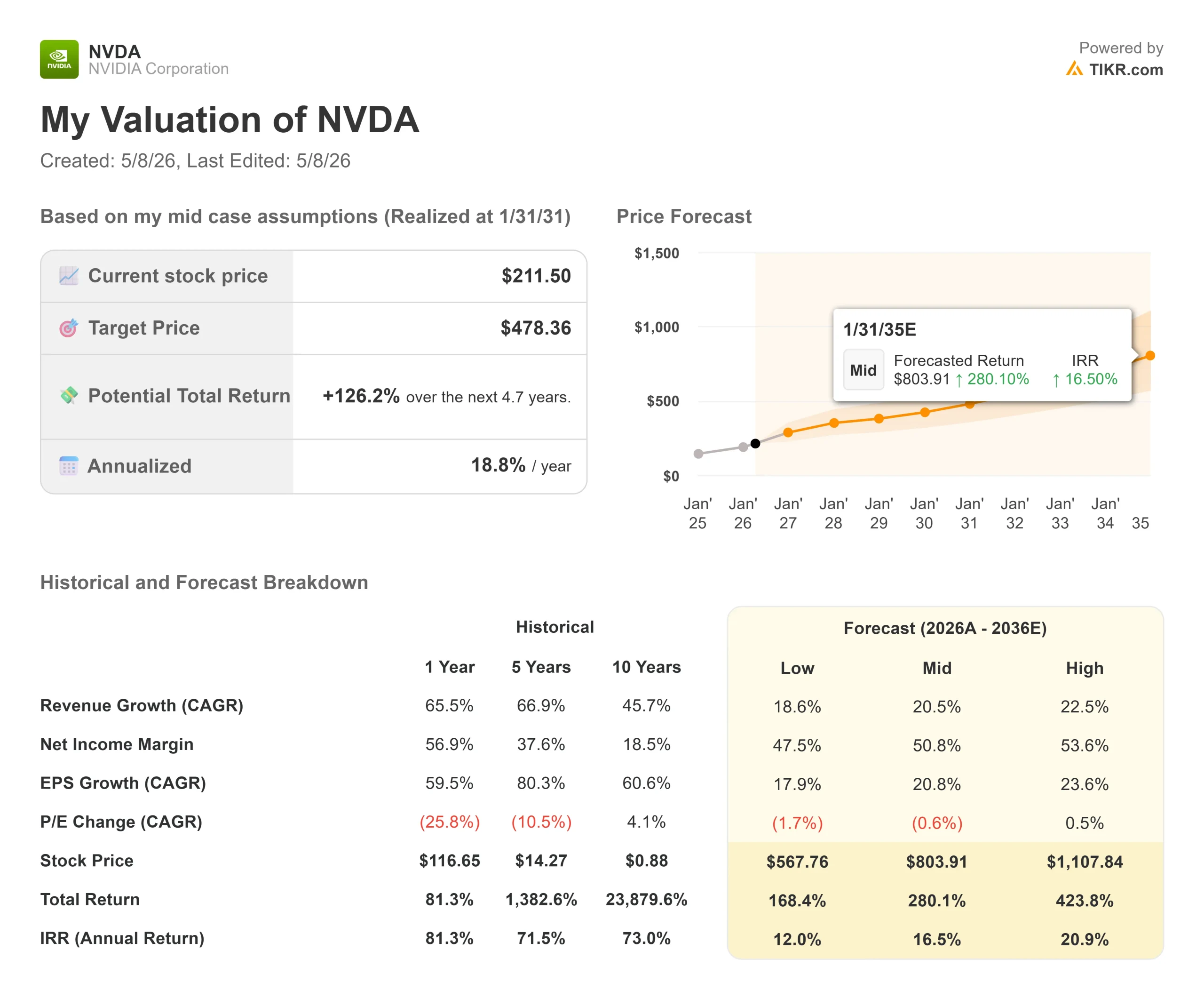

Key Stats for NVIDIA Stock

- Current Price: $211.50

- Target Price (Mid): ~$478

- Street Target: ~$269

- Potential Total Return: ~126%

- Annualized IRR: ~19% / year

- Earnings Reaction: -5.46% (February 26, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

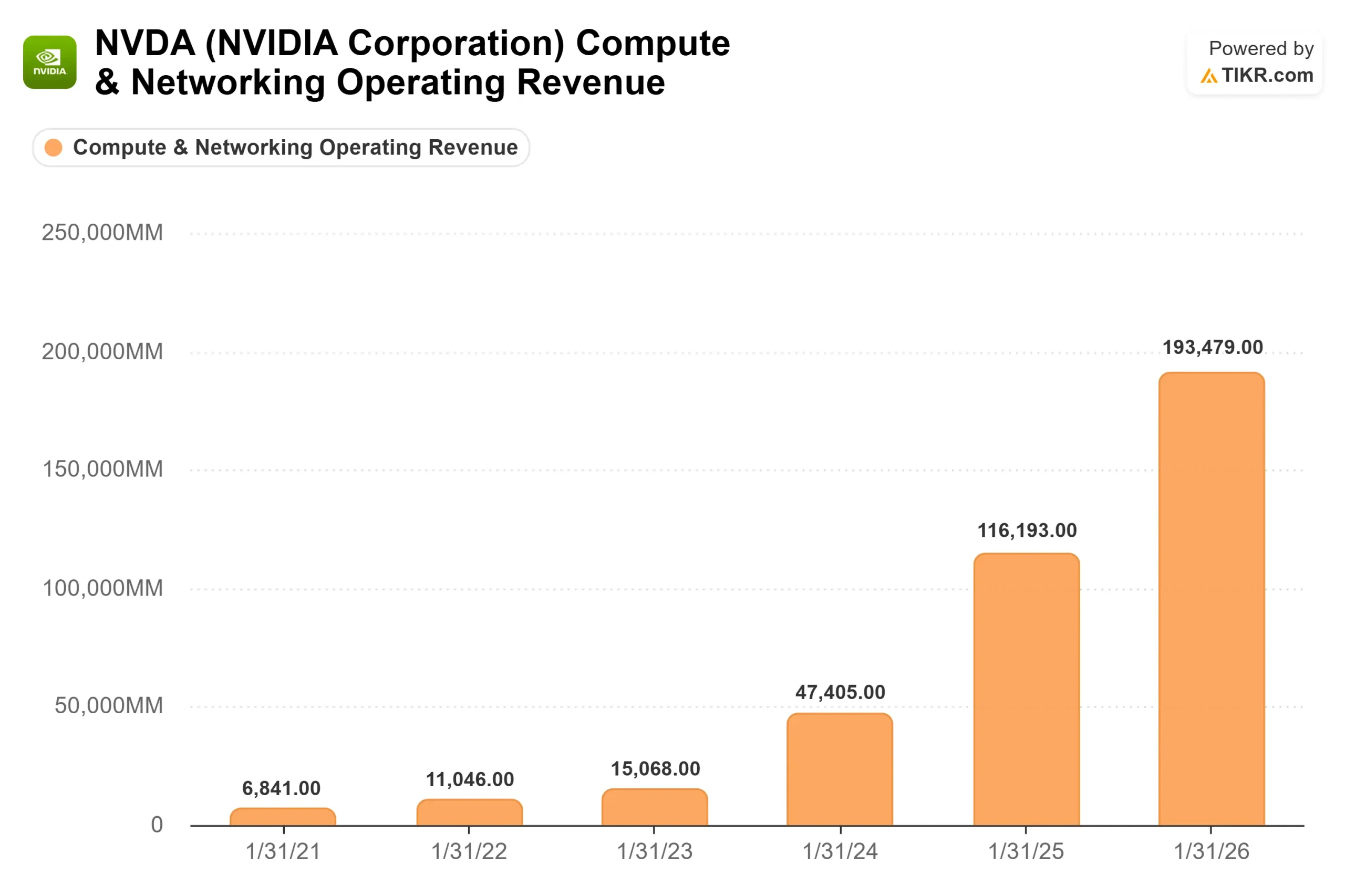

Semiconductor stocks are back in focus, and NVIDIA (NVDA) is leading. After a 20.22% peak drawdown on March 30, 2026, the stock has recovered sharply and now sits near its 52-week high of $216.83. Bulls see a company that has moved beyond selling chips and is now physically building the infrastructure layer every AI factory will run through. Bears argue the stock is priced for a hyperscaler spending cycle that has never been this large or this concentrated. The unresolved question heading into May 20 earnings is whether the trillion-dollar demand Jensen Huang described at GTC 2026 is as locked in as he says. The Corning deal, announced May 6, gave bulls another concrete data point.

A $3.2 Billion Bet on Fiber Over Copper

On May 6, NVIDIA and Corning announced a multiyear partnership to expand U.S. manufacturing of optical connectivity for AI infrastructure. The deal includes a $500 million upfront investment from NVIDIA, three new manufacturing facilities in North Carolina and Texas, and a tenfold increase in Corning’s optical connectivity manufacturing capacity, with NVIDIA holding the right to invest up to $3.2 billion in total. Corning shares jumped 12% on the news, and NVIDIA gained nearly 6%.

The technology is co-packaged optics (CPO), which places fiber-optic data transmission directly alongside the compute chip instead of routing signals through copper wiring. NVIDIA’s Vera Rubin AI server racks currently hold roughly 5,000 copper cables. Corning’s glass fiber cables move data as photons and can use up to 20 times less power than copper, according to Corning CEO Wendell Weeks. Jensen Huang, Founder and CEO of NVIDIA, framed the strategic intent directly in the joint announcement: “AI is driving the largest infrastructure build-out of our time, and a once-in-a-generation opportunity to reinvigorate American manufacturing and supply chains.”

See historical and forward estimates for NVIDIA stock (It’s free!) >>>

Why Jensen Said This Was Coming

The GTC 2026 analyst session on March 18 explains the logic. Huang told analysts that NVIDIA is no longer building computing tools. It is building a token manufacturing equipment. “A computer used to be just a tool,” he said. “A computer of the future is manufacturing equipment. The energy efficiency of it, the production efficiency of it, matters everything because it drives your revenues.” Replacing copper cables with fiber inside Vera Rubin is not a component swap. It is the energy efficiency improvement that keeps AI factory economics viable as clusters scale.

On demand, Huang was direct: “We have strong confidence and visibility of $1 trillion plus of Blackwell plus Rubin” in purchase orders and firm demand through the end of 2027. He specified that the figure excludes Rubin Ultra, Feynman, and standalone Vera products entirely, making it a floor, not a ceiling. Vera Rubin is already in production. Groq, NVIDIA’s acquired low-latency inference chip, is expected in Q3 2026.

Huang also described how adding Groq to a subset of AI factory customers’ workloads would increase those customers’ compute spend by approximately 25%, representing demand that is not yet visible in Street models.

What the Valuation Says

At $211.50, NVIDIA trades at 25.4x next twelve months (NTM) P/E and 20.3x NTMEV/EBITDA, both well below where the stock traded in 2024 and early 2025. The Street has 48 Buys, 9 Outperforms, 2 Holds, 0 Underperforms, and 1 Sell, with a mean price target of around $269, implying about 27% upside from current levels.

Among semiconductor peers on the TIKR Competitors page, Broadcom trades at 24.3x NTM EV/EBITDA and 30.6x NTM P/E, while Marvell Technology trades at 36.2x NTM EV/EBITDA and 41.8x NTM P/E. Both carry slower near-term revenue CAGR forecasts than NVIDIA’s Wall Street consensus of around 50% for the next two years. NVIDIA trades at a discount to Marvell on EV/EBITDA despite growing at roughly twice the rate. QUALCOMM’s 15.8x NTM EV/EBITDA reflects far lower AI infrastructure exposure, which explains the gap.

See how NVIDIA performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $211.50

- Target Price (Mid): ~$478

- Potential Total Return: ~126%

- Annualized IRR: ~19% / year

See analysts’ growth forecasts and price targets for NVIDIA stock (It’s free!) >>>

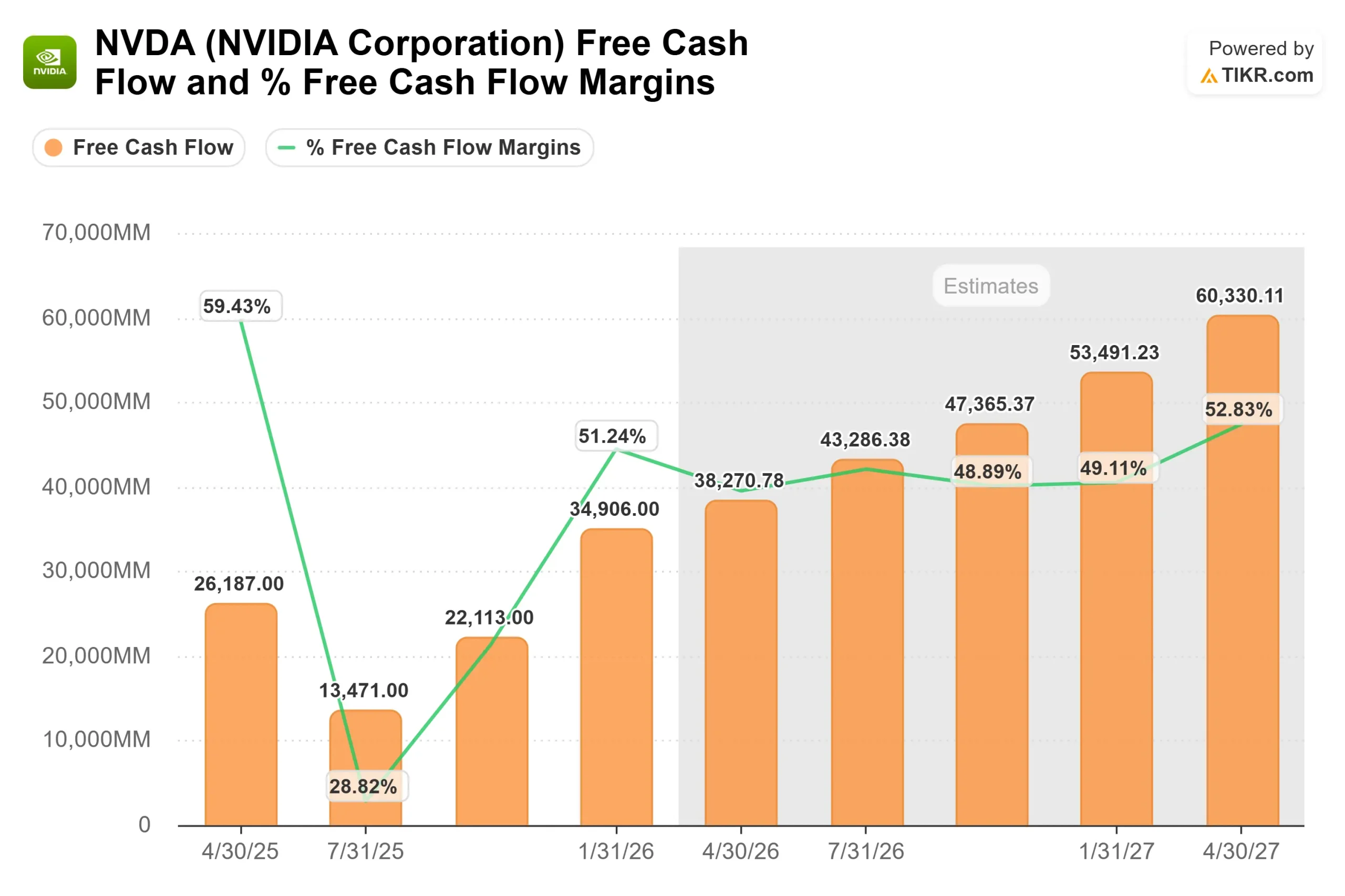

The mid case is built on two revenue drivers: sustained hyperscaler buildout, with Microsoft planning around $190 billion and Meta up to $145 billion in 2026 capital expenditures, and NVIDIA’s expanding non-hyperscaler segment covering enterprise on-premises, regional clouds, and physical AI. The margin driver is operating leverage, with projected net income margins of around 51%, a modest normalization from NVIDIA’s current trailing twelve months (LTM) net margin of 56.9%.

The high case (around 23% revenue CAGR, around 54% net income margin) projects around $1,108 by 2031, a return of around 424%. The primary risk is multiple compressions. If hyperscaler capex slows, export restrictions eliminate remaining Chinese market revenue, or a competitor matches NVIDIA’s token throughput at lower cost, the stock reprices toward the low case of around $568 by 2031, still roughly 168% upside but with more time and volatility required. At GTC 2026, CFO Colette Kress confirmed NVIDIA targets returning approximately 50% of free cash flow to shareholders through buybacks and dividends once first-half supply chain commitments are complete.

Conclusion

Watch Data Center revenue and Q2 guidance at NVIDIA’s Q1 fiscal 2027 earnings on May 20, 2026. Wall Street consensus currently projects around $87 billion in Q2 revenue, representing roughly 85% year-over-year growth. Guidance at or above that level confirms the $1 trillion demand pipeline is converting into reported results on schedule. NVIDIA is not cheap at around 25x forward earnings, but the GTC 2026 transcript reveals demand layers the current stock price does not yet fully reflect.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in NVIDIA?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NVIDIA, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NVIDIA alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!