Key Stats for Lucid Stock

- Current Price: $6.34

- 52-Week High / Low: $33.70 / $5.62

- Max Drawdown: 81% on 4/29/26

- Street Target (Mean): ~$9 (10 analysts)

- Target Price (High Case): ~$10

- Potential Total Return (High Case): ~62%

- Annualized IRR (High Case): ~6% / year

- Earnings Reaction: (0.96%) on 5/5/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Lucid Group (LCID) has lost 82% of its value since its 52-week high of $33.70 in July 2025, and sits near its all-time low. The stock fell another 33% in April 2026 alone, even as the company announced a $500 million Uber investment and a 35,000-vehicle robotaxi commitment. That gap between the headline and the price action captures where investor sentiment stands. Q1 2026 results, reported May 5, did not close that gap.

Revenue came in at $282.47 million, a 21% miss against the $358.51 million estimate. The net loss widened to approximately $1 billion, up from $366 million in Q1 2025. Management suspended full-year guidance, citing an ongoing review by incoming CEO Silvio Napoli. LCID slipped another 0.96% on the reporting date. Post-earnings, Morgan Stanley cut its price target to $5 (Underweight) and Baird slashed its target to $6 from $12 (Neutral), while Benchmark downgraded from Buy to Hold.

The bull case rests on what happens in 2027: the Midsize platform ramp, the Uber commercial robotaxi launch, and Napoli’s cost-cutting mandate. For investors willing to look past the quarterly damage, the question is whether any of that is priced in at $6.05.

See historical and forward estimates for Lucid stock (It’s free!) >>>

The Stop Sale Explains Q1. The Margin Problem Is Older.

Lucid produced 5,500 vehicles in Q1, up 149% year-over-year, but converted only 3,093 into deliveries. The shortfall came from a 29-day stop sale on the Gravity SUV triggered by a supplier-quality issue with second-row seat belt anchor welds. Finished vehicles sat in inventory rather than being converted to revenue.

CFO Taoufiq Boussaid laid out the gross margin damage precisely on the call: lower volume against a fixed manufacturing cost base, overhead underabsorption, and the absence of a large regulatory credit that boosted Q4. Gross margin came in at (110.4%) versus (80.7%) in Q4 2025 and (97.2%) in Q1 2025. Boussaid said the costs tied to the stop sale do not carry forward, and that the company’s structural unit cost reduction target a 50% to 60% improvement over the coming years remains intact.

Inventory stood at approximately $1.47 billion at quarter’s end. Over $200 million in inventory impairments were taken in Q1, with management expecting those to decline. As stop-sale vehicles convert to deliveries through the year, cash generation should improve materially.

The deeper problem predates the supplier issue: Lucid’s fixed manufacturing cost base is too large for its current delivery volumes. The company loses money on every vehicle it builds. Gross margin breakeven requires meaningful scale that does not arrive until the Midsize platform and M2, Lucid’s Saudi Arabia factory currently under construction, begin contributing to output.

See how Lucid performs against its peers in TIKR (It’s free!) >>>

What the Uber Deal and New CEO Actually Mean

On April 14, 2026, Lucid expanded its partnership with Uber via an SEC 8-K filing. Uber raised its total investment to $500 million, adding $200 million on top of its original $300 million from July 2025. That stake gives Uber an 11.52% ownership position, making it the second-largest shareholder after Saudi Arabia’s Public Investment Fund (PIF), which controls more than 54% of the company. The robotaxi fleet commitment grew from 20,000 to at least 35,000 vehicles.

The Q1 call added operational detail that the announcement alone could not. Winterhoff confirmed Lucid has met all milestones in the joint program with Uber and autonomous driving partner Nuro: 75 engineering vehicles delivered, driverless testing active across several U.S. cities, and California DMV approval received for driverless Gravity testing. Uber and Nuro employees are now testing the end-to-end rider experience within the Uber app. Production validation builds begin this quarter, completing in Q3. Regular commercial production for the robotaxi fleet targets early Q4.

Winterhoff’s exact words on the call: “We have met all milestones so far in our joint project with Nuro to provide autonomous Lucid Gravities to Uber for commercial launch by the end of the year, and remaining milestones are on track.”

Incoming CEO Silvio Napoli, formerly of Schindler Group, set one overriding priority: “A central objective over time is to build a more self-sufficient company, one that progresses towards funding its own growth.” He declined to update the financial outlook pending his review, with more detail expected at Q2. One recent incremental positive: Lucid began rolling out Apple CarPlay and Android Auto to existing Gravity owners this week via over-the-air update, a step that strengthens the ownership experience as the company tries to drive order intake momentum.

TIKR Advanced Model Analysis

- Current Price: $6.34

- Target Price (High Case): ~$10

- Potential Total Return (High Case): ~62%

- Annualized IRR (High Case): ~6% / year

See analysts’ growth forecasts and price targets for Lucid stock (It’s free!) >>>

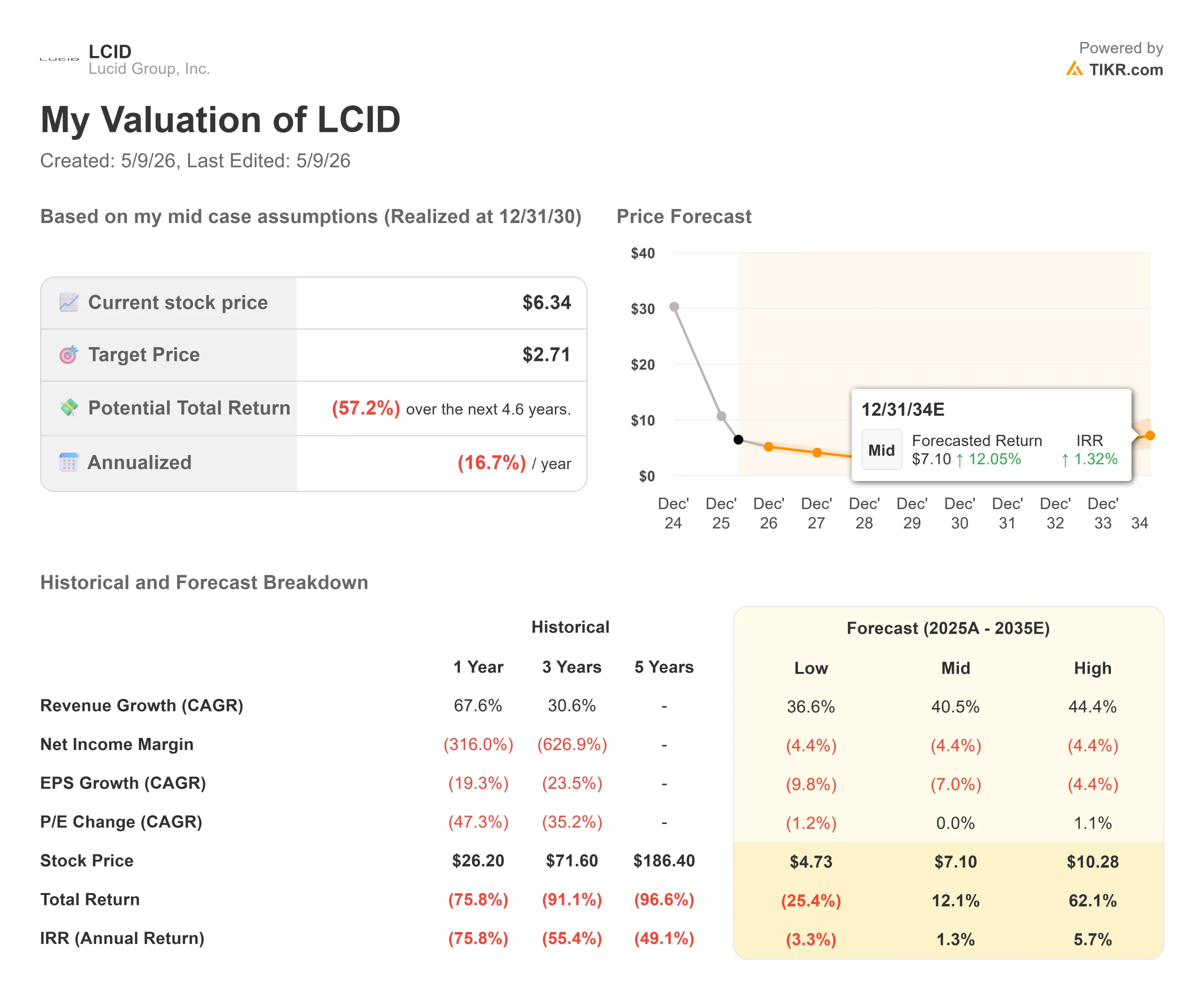

The TIKR valuation model for LCID runs through December 31, 2034. I’m using the high case because it is the scenario that would make buying LCID at $6.34 worth the risk. The mid-case target of approximately $7 by 12/31/34 implies a total return of roughly 12% over more than eight years, less than 2% annualized. That does not justify the execution risk here. At the mid-case, LCID is not cheap.

The high case requires revenue to grow at a compound annual growth rate (CAGR) of around 44% through 2035, implying a target of approximately $10 per share, roughly 62% total return, and ~6% annualized IRR. The two revenue CAGR drivers are the Midsize platform ramp starting in 2027 and the Uber robotaxi fleet revenue stream. The margin driver is M2 manufacturing efficiency combined with BOM (bill of materials, the cost of all components needed to build each vehicle) reduction, targeted at 50% to 60% over the coming years. Winterhoff confirmed on the call that the Midsize BOM cost is “still tracking below our initial cost estimates,” one of the few clean positives in the quarter.

The primary risk is running out of capital before Midsize volumes scale, forcing further dilutive equity raises. The secondary risk is regulatory or execution delays in the robotaxi program, which anchors much of the long-term demand visibility. Free cash flow (FCF) is projected to remain deeply negative through at least 2028 per TIKR estimates, narrowing as M2 capital expenditure winds down after 2027.

The downside: a stock that dilutes shareholders, misses Midsize timing, and never builds enough volume to absorb its cost base. The upside: Napoli succeeds where prior leadership fell short, the Midsize launch in 2027 goes more smoothly than Gravity did, and robotaxi revenue begins to diversify the top line by late 2026.

Conclusion

The metric to watch at Q2 earnings, expected around early August 2026, is the production-to-delivery conversion rate. If Lucid delivers at least 4,500 vehicles in Q2, the stop-sale disruption reads as isolated, and the Gravity ramp is back on track. Anything materially below that, absent a new one-time disruption, signals a demand problem that capital and partnership announcements cannot fix. At $6.05, LCID is priced for skepticism. What it needs to turn the corner is proof.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Lucid?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Lucid, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Lucid alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!