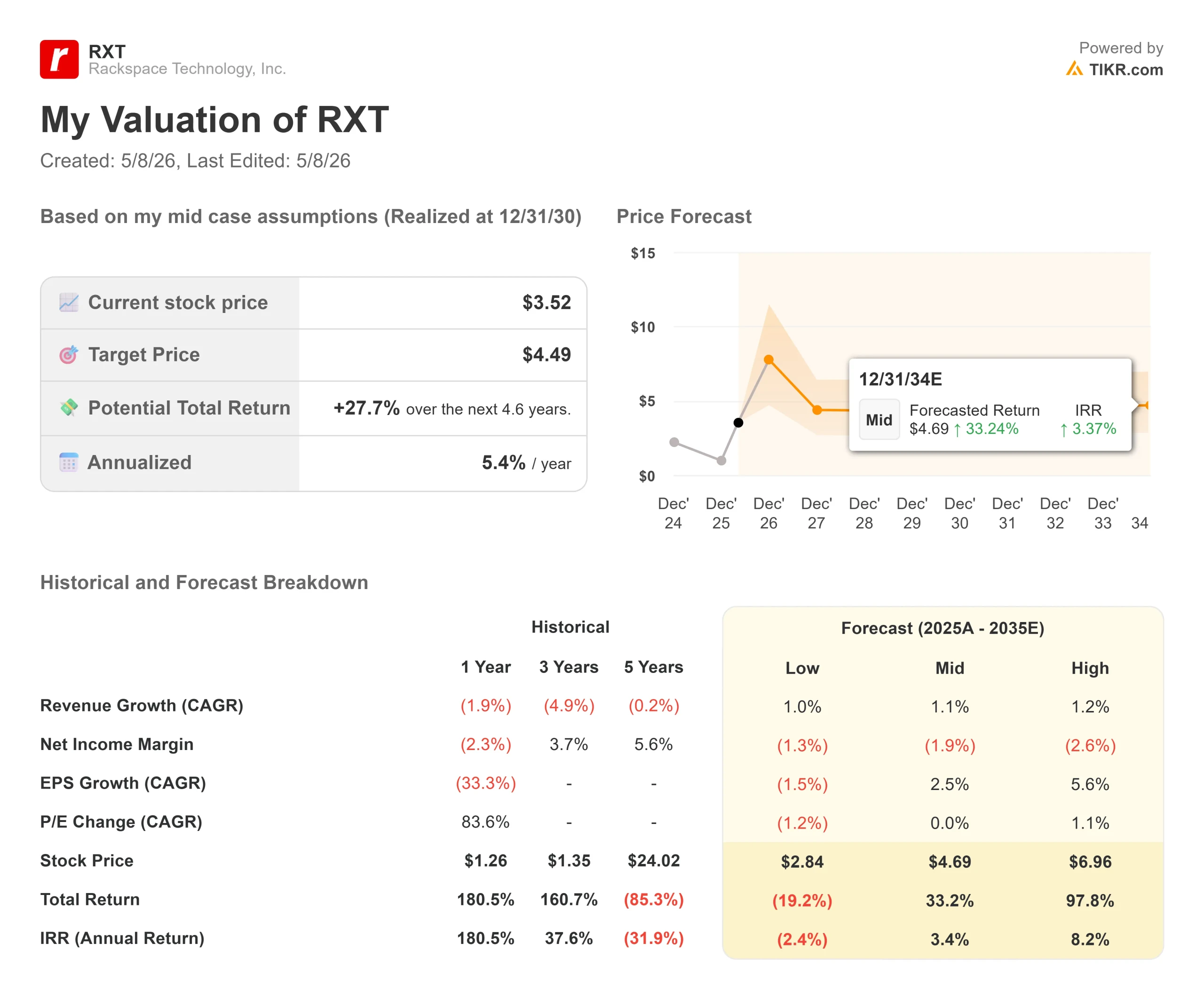

Key Stats for Rackspace Stock

- Current Price: $3.52

- Target Price (Mid): ~$4.50

- Street Target: $2.17

- Potential Total Return (Mid): ~28%

- Annualized IRR (Mid): ~5% / year

- Earnings Reaction: +55.07% (May 7, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

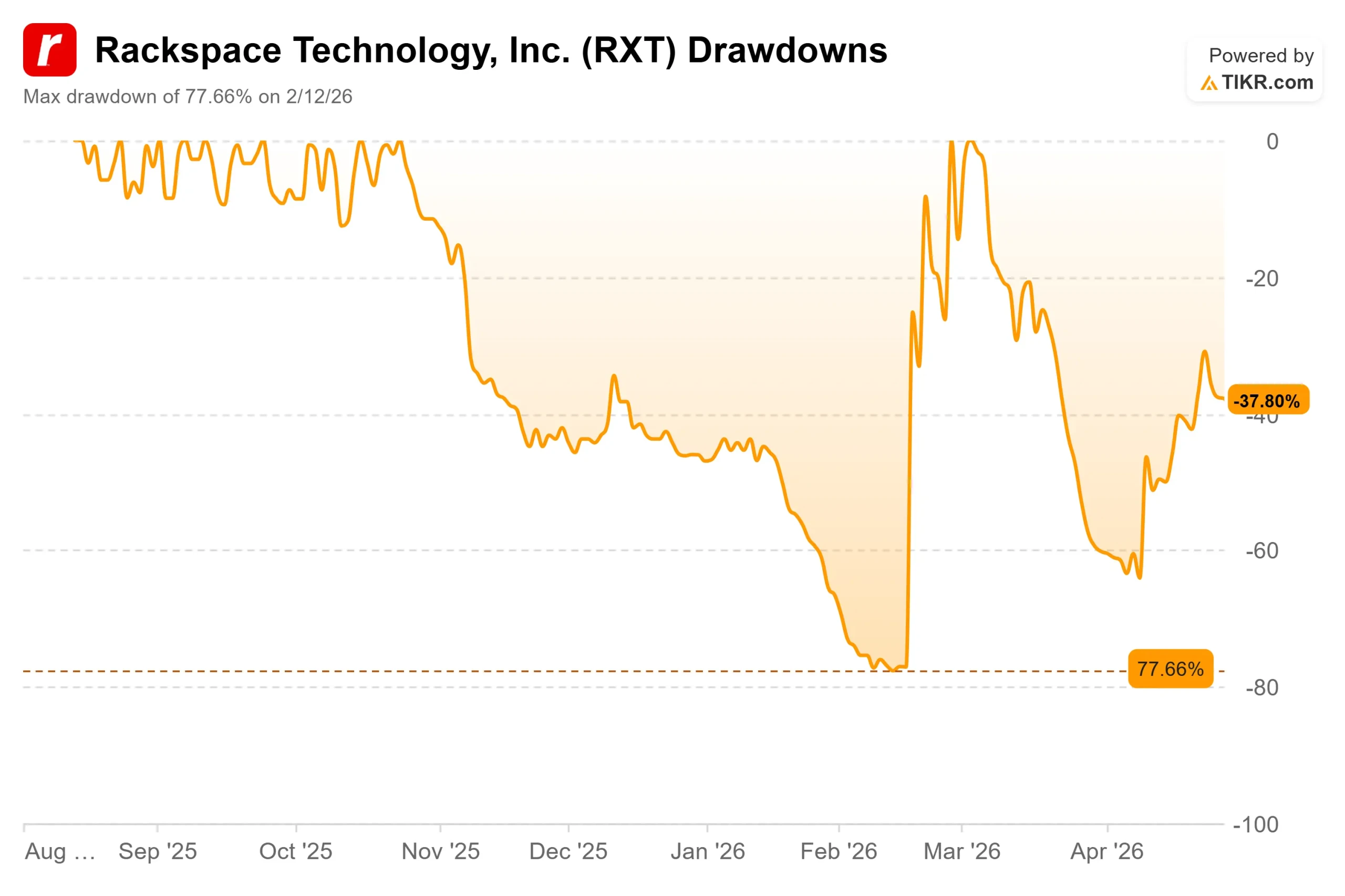

Rackspace Technologies (RXT) just delivered one of the more unusual earnings sessions in recent memory. On May 7, 2026, Rackspace Technology stock surged 55.07% to close at $3.52, after the company simultaneously reported a Q1 revenue beat and announced a memorandum of understanding (MOU) with AMD to build governed enterprise AI infrastructure for regulated industries. The stock had previously collapsed as much as -77.66% from peak to trough, bottoming on February 12, 2026.

Bulls see a company finally executing on a credible AI strategy. Bears point out that the MOU is non-binding, the EPS missed estimates, and the stock now trades well above the Street’s consensus target of $2.17 from three analysts, all carrying Hold ratings.

What the AMD Deal Actually Means

The AMD MOU is not a chip supply agreement. It is a framework for building a full managed AI stack, from silicon to outcome, for customers who cannot use public cloud due to compliance requirements.

CEO Gajen Kandiah explained the logic on the Q1 2026 earnings call: “Production inference is heterogeneous. Frontier models run on GPU, small language models, classical ML embeddings and many domain-specific workloads run more efficiently on CPU. AMD is the partner that brings both Instinct GPUs and EPYC CPUs inside one integrated architecture, which lets us route each workload to the right compute.”

The MOU establishes four integrated capabilities: a fully managed Enterprise AI Cloud for private, public, and sovereign environments; an Enterprise Inference Engine that retains domain knowledge across queries; Inference as a Service as a governed alternative to commodity GPU rental; and Bare Metal Accelerated Compute for deterministic training and inference workloads. The goal is a single accountable operator for regulated customers in health care, financial services, and sovereign government.

The key caveat: the MOU is non-binding. No definitive agreements have been reached, no financing is secured, and CFO Mark Marino confirmed on the call that the AMD arrangement is “not something that we’ve got materially factored into our ’26 guidance.” Investors pricing in immediate AMD revenue are getting ahead of the facts.

See historical and forward estimates for Rackspace stock (It’s free!) >>>

The Q1 Results: Progress, With a Catch

Total GAAP revenue was $678 million, up 2% year-over-year, beating the Wall Street consensus of $660.83 million by 2.61%. Adjusted EBITDA reached $71.2 million, beating estimates of $68.57 million by 3.83%. Non-GAAP operating profit hit $31 million, up 20% year-over-year.

The catch: non-GAAP EPS came in at -$0.06, missing the -$0.03 estimate. GAAP net income swung to $8.3 million from a $71.5 million loss a year earlier, but that improvement included a $55.8 million gain on debt extinguishment (a one-time accounting benefit from repurchasing debt below face value). The underlying business is not yet consistently profitable on a GAAP basis.

Segment results were mixed. Public Cloud revenue grew 7% to $443 million, with services revenue up 10%, reflecting a deliberate push toward higher-value engagements. Private Cloud revenue fell 6% to $235 million due to the timing of large health care deal onboarding. Private Cloud segment operating margin improved 30 basis points to 24.7%, showing cost discipline despite the revenue dip.

The company ended Q1 with $94 million in cash and $295 million in total liquidity. Rackspace repurchased roughly $96 million of debt at a discount during the quarter, advancing its deleveraging strategy ahead of the 2028 debt maturity. Net debt remains over $3 billion.

Management reaffirmed full-year 2026 guidance: $2.6 billion to $2.7 billion in revenue, $160 million to $170 million in non-GAAP operating profit, and $305 million to $315 million in adjusted EBITDA.

Real Customer Wins Behind the Strategy

The earnings call transcript details specific wins that give the AI pivot credibility beyond the AMD headline. In health care, Rackspace expanded its relationship with AdventHealth, already one of the top five Epic EHR (electronic health record) deployments globally, adding over 400 additional workloads to Rackspace Private Cloud. The company also signed a multiyear agreement with a U.K. NHS Foundation Trust for a sovereign health care cloud.

In sovereign cloud, BT selected Rackspace as the foundation for BT Sovereign Cloud, the U.K.’s first full suite of sovereign services hosted and operated entirely within the U.K., with security-cleared operations teams. These are long-term, compliance-driven contracts, not pilots.

The Palantir partnership is also progressing. Rackspace closed its first joint deal in 41 days with a U.S.-based solar tracking manufacturer. Forward-deployed engineers (FDEs), who embed directly inside customer environments, deployed AI workflows on Palantir Foundry and cut the customer’s 16.5-day quoting cycle by 94%. The engagement expanded into EMEA.

How RXT Compares to Peers

RXT trades at 1.49x NTM EV/Revenue and 12.71x NTM EV/EBITDA, above the IT services peer group median of 1.26x EV/Revenue and 6.95x EV/EBITDA. The closest structural peers, Kyndryl (KD) and DXC Technology (DXC), trade at 0.37x and 0.40x EV/Revenue, respectively, and 2.13x and 2.90x EV/EBITDA, respectively. Both carry similar debt-heavy turnaround profiles without a comparable AI infrastructure narrative.

RXT’s premium to those peers is only justified if the AMD partnership closes on favorable terms and the Palantir and Uniphore engagements scale into material revenue. At current prices, the market is betting that they do.

See how Rackspace performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $3.52

- Target Price (Mid): ~$4.50

- Potential Total Return (Mid): ~28%

- Annualized IRR (Mid): ~5% / year

See analysts’ growth forecasts and price targets for Rackspace stock (It’s free!) >>>

The TIKR model uses the mid case as the base, projecting a revenue CAGR of approximately 1% through 2030. The two primary growth drivers are Public Cloud services expansion (already growing at 10% annually) and gradual Private Cloud stabilization as health care and sovereign deals come fully online. The margin driver is operating expense leverage: non-GAAP operating profit is already growing 20% annually on modest revenue, and the model assumes that trajectory continues as higher-value AI engagements displace lower-margin infrastructure work.

The mid case returns roughly 28% total, or around 5% annualized, modest for a company carrying over $3 billion in net debt and negative GAAP margins. The trailing free cash flow of $243.55 million provides real deleveraging capacity and supports the bull case timeline.

The high case projects approximately $6.96 by 12/31/30, a total return of around 98%, and an annualized IRR of approximately 8%. That requires the AMD deal to close on favorable terms and the Palantir and Uniphore partnerships to generate material revenue by 2027 to 2028.

The downside is equally clear. The low case implies approximately $2.84 by 12/31/30, a loss of around 19% from current prices, if revenue stalls and the AMD MOU does not become a binding agreement. Given that RXT already trades well above the Street’s $2.17 consensus target, any reversal on the AMD narrative would likely push the stock back toward that level quickly.

Conclusion

The key metric to watch at Rackspace’s next earnings report (expected around August 2026) is Private Cloud revenue for Q2 2026. Management has reaffirmed the full-year Private Cloud growth outlook and cited signed engagements with AdventHealth, Seattle Children’s, and a Database-as-a-Service partner onboarding through the rest of the year. Sequential revenue recovery in Q2 would confirm that the H1 timing dynamic was real. A continued decline would raise questions about whether the AI pivot is generating actual contract flow or just strategic noise.

Rackspace is building a specific niche: governed enterprise AI infrastructure for regulated and sovereign customers, with a curated partner stack and a single accountable operator model. The Q1 results and the AMD announcement both support that thesis. At $3.52, the stock has already priced in a version of it succeeding.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Rackspace?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Rackspace, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Rackspace alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Rackspace on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!