Key Stats for Intel Stock

- Current Price: $109.62

- Target Price (Mid): ~$231

- Street Target: ~$82

- Potential Total Return: ~111%

- Annualized IRR: ~17% / year

- Earnings Reaction: +23.60% (April 24, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Intel (INTC) is up roughly 190% in 2026, including a 23.60% single-day surge after Q1 earnings and a further 13% jump on May 5 after Bloomberg reported that Apple is in early-stage discussions with Intel and Samsung about manufacturing its main device chips in the U.S. Bulls say Intel’s foundry is finally becoming real, with Apple, Tesla’s Terafab, and Google all in the picture. Bears note that external foundry revenue was just $174 million in Q1 against $5.4 billion in total foundry revenue; the segment is still losing $2.4 billion per quarter, and the stock already trades 34% above the Street’s consensus target of around $82. The core question: can Intel’s foundry convert high-profile partnerships into actual wafer revenue fast enough to justify current prices?

Why the Apple News Matters

Apple’s reported interest follows directly from TSMC capacity pressure. With Google, NVIDIA, and Amazon all competing for TSMC’s leading-edge manufacturing, Apple is getting squeezed on supply. That creates an opening for Intel.

This is not a return to the old Intel-Apple design relationship, which ended in 2020 when Apple launched its own in-house chips. What Apple is reportedly exploring is using Intel purely as the manufacturer for Apple-designed chips. That distinction matters: foundry revenue, at scale with improved utilization, carries a structurally different margin profile than product revenue.

Intel’s foundry pitch centers on its Intel 18A process node (its most advanced chip manufacturing technology, roughly equivalent to a 2-nanometer-class chip) and the follow-on Intel 14A. CFO David Zinsner confirmed on the Q1 2026 earnings call that 18A yields are running ahead of internal projections. CEO Lip-Bu Tan added that 14A maturity and performance are already outpacing 18A at a comparable stage. Tan also said external 14A design commitments are expected to begin emerging in the second half of 2026. A confirmed pilot tape-out with Apple would be Intel Foundry’s highest-profile external win to date.

See historical and forward estimates for Intel stock (It’s free!) >>>

What the Q1 Transcript Reveals

Several details from the April 23 earnings call deserve more attention than they received.

Advanced packaging is inflecting toward billions. Packaging technology, which combines multiple chips into a single module for better performance and efficiency, is generating demand Zinsner described as “more in the billions of dollars per year” on the earnings call, larger than he originally expected. Intel added to its packaging backlog in Q1 and announced a multi-year expansion of back-end facilities in Malaysia, with committed demand converting to revenue beginning in 2027.

The ASIC business hit a $1 billion annual run rate. Intel’s ASIC segment, which builds custom silicon tailored to specific customer workloads, nearly doubled year-over-year in Q1. Zinsner confirmed the business is running “north of $1 billion” annually. Tan described Intel’s competitive advantage as the ability to combine CPU design, packaging, and foundry in ways pure-play chipmakers cannot.

SambaNova cleared antitrust review. On May 1, Reuters reported that U.S. authorities completed their review of Intel’s $35 million investment in SambaNova, an AI chip startup focused on generative AI inference, raising Intel’s stake from 6.8% to approximately 8.2%. Intel plans to invest a further $15 million. The clearance removes a regulatory overhang and formalizes a multi-year collaboration pairing SambaNova’s AI processors with Intel’s Xeon CPUs for agentic AI workloads.

Google signed a multi-year CPU deal. Intel signed multiple long-term agreements in Q1, with Google publicly named. Zinsner described the typical structure as three to five years, with volume and pricing fixed on both sides. Xeon was also confirmed as the host CPU for NVIDIA’s DGX Rubin NVL8 systems, placing Intel’s chips inside NVIDIA’s most advanced AI compute platforms.

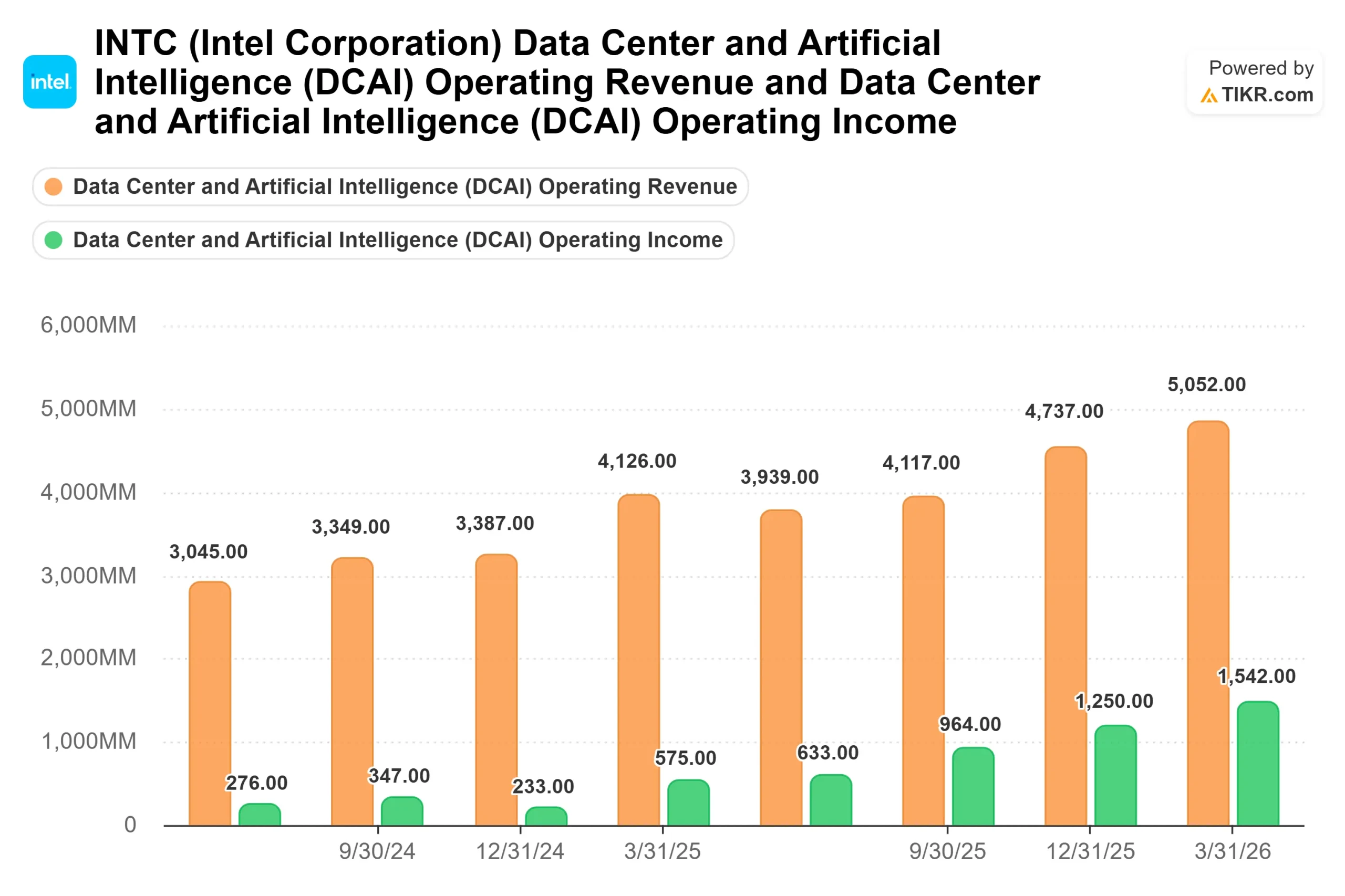

The CPU-to-GPU ratio is shifting. Tan told analysts that the ratio of CPUs to GPUs in AI deployments has moved from approximately 1:8 in training environments to 1:4 in inference, with the direction toward parity as workloads shift to agentic AI. DCAI revenue of $5.1 billion in Q1, up 22% year-over-year, shows that the shift is already in the results.

Valuation vs. Peers

At $109.62, INTC trades at 9.61x NTM EV/Revenue and 28.24x NTM EV/EBITDA, per TIKR. Broadcom trades at 16.66x NTM EV/Revenue and 24.33x NTM EV/EBITDA. AMD trades at 11.86x NTM EV/Revenue and 40.10x NTM EV/EBITDA. Arm Holdings commands 37.55x NTM EV/Revenue and 80.49x NTM EV/EBITDA. On revenue multiples, Intel trades at a discount to all three peers, partly reflecting the foundry drag on margins.

The bear case is specific. Trailing twelve-month free cash flow is negative $8.2 billion. TIKR’s forward estimates project a return to positive free cash flow in 2027. If Apple’s talks stall, if 14A external commitments slip past the first half of 2027, or if rising substrate and memory costs pressure gross margins in the second half of 2026 as Zinsner explicitly flagged, the foundry assumptions underpinning the current multiple become harder to defend. The Street’s consensus of around $82 suggests most analysts have not yet embedded an Apple or large-scale external foundry scenario into their models.

The bull case rests on three assets no single peer replicates in combination: an x86 CPU franchise at the center of AI infrastructure demand, advanced packaging already generating multi-billion-dollar annual demand, and domestic U.S. wafer fabrication with government backing. A confirmed Apple deal, even a limited pilot, would likely pull forward additional external customer conversations.

See how Intel performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $109.62

- Target Price (Mid): ~$231

- Potential Total Return: ~111%

- Annualized IRR: ~17% / year

See analysts’ growth forecasts and price targets for Intel stock (It’s free!) >>>

The mid-case uses a revenue CAGR of around 8% through 2030, driven by sustained DCAI growth as CPU-to-GPU ratios normalize in inference and agentic workloads, and foundry revenue growth as external commitments convert from backlog to production. The margin driver is gross margin recovery as 18A exits the loss-making ramp phase and advanced packaging scales toward corporate-average margins, consistent with Zinsner’s guidance on the Q1 call. The high case targets around $370 per share by 2030. The low case targets around $229, reflecting a slower external ramp and continued input cost headwinds.

Conclusion

Watch Intel Foundry’s external revenue line at Q2 2026 earnings on July 23. It came in at $174 million in Q1. Sequential growth in that number is the clearest near-term signal that Apple discussions and other external engagements are converting from conversations into contracted production. That single metric is what turns the foundry story from a thesis into a business.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Intel?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Intel, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Intel alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!