Key Stats for WM Stock

- Past week’s performance: -5.5%

- 52-week range: $194 to $248

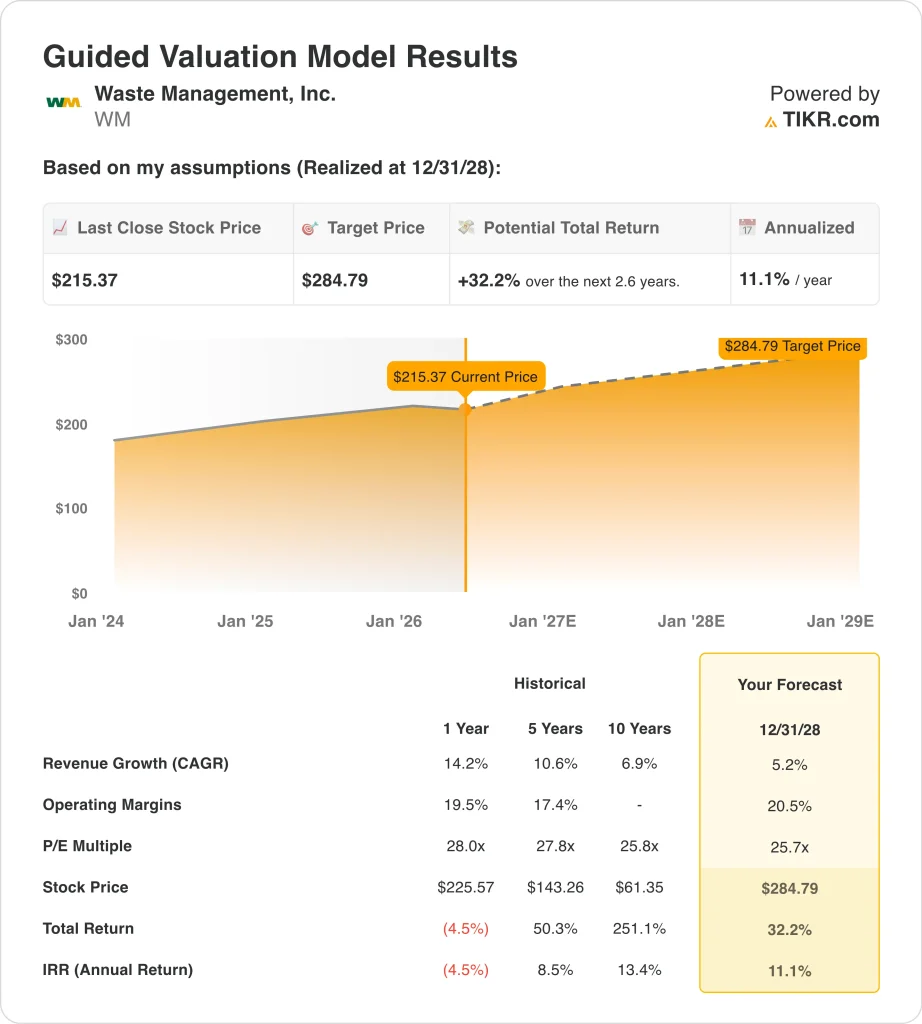

- Valuation model target price: $285

- Implied upside: +32.2% over 2.6 years

Value your favorite stocks like WM with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Waste Management (WM) is North America’s largest environmental services company. It collects, transfers, and disposes of solid waste, and operates landfill gas-to-energy facilities across the continent. WM also completed its $7.2 billion acquisition of Stericycle, a medical waste and secure document destruction company, in late 2024.

The company reported Q1 2026 results on April 29, with revenue of $6.23 billion, just below the $6.29 billion Wall Street estimate. Net income rose 13.5% to $723 million, and adjusted EPS beat estimates on pricing discipline and renewable energy growth.

The revenue miss disappointed investors despite the bottom-line beat. WM has set ambitious long-term targets, including revenue of $28.5 to $29.25 billion by 2027. Reaching that target requires a meaningful acceleration in volumes over the next several quarters, so the Q1 shortfall raised execution questions. Q4 2025 revenue also missed at $6.31 billion versus the $6.39 billion estimate, making this the second consecutive top-line miss.

Leadership changes added to investor caution. CFO Devina Rankin resigned effective November 2025, and David Reed stepped into the role. That transition came during the Stericycle integration, a process where consistent financial leadership is especially important. Investors also noted multiple executive insider share sales in the first quarter of 2026, which added minor but visible selling pressure.

Going forward, the market will focus on whether Q2 volumes recover and whether Stericycle integration delivers the revenue synergies management has promised.

See analysts’ growth forecasts and price targets for WM (It’s free) >>>

Is WM Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 5.2%

- Operating Margins: 20.5%

- Exit P/E Multiple: 25.7x

Based on these inputs, the model estimates a target price of $285, implying a 32.2% total return from the current share price and an annualized return of 11.1% over the next 2.6 years.

At 11.1% annualized, WM clears the 10% threshold that broadly defines an attractive long-term investment. For a slow-growing infrastructure business, that level of return is meaningful, especially when combined with a dividend yield of 1.8% and a solid payout ratio of 49.5%. WM is not a high-growth stock, but it generates very reliable and recurring cash flow.

Revenue CAGR of 5.2% is a conservative assumption relative to the one-year historical growth rate of 14.2%, which was inflated by the Stericycle acquisition. Over ten years, WM grew revenue at a CAGR of 6.9%, so the model’s 5.2% assumption reflects a normalized organic growth picture. WM often operates in regional monopolies or duopolies, and pricing power in those markets provides a durable revenue floor.

The current LTM operating margin of 18.7% sits below the model assumption of 20.5%. That gap implies the market expects meaningful margin expansion over the next two to three years. WM’s automation push, with a target of $450 million in annualized savings, provides the operational support for that improvement. And Stericycle integration synergies should also contribute incremental margin gains through 2027.

What’s Driving WM Stock Going Forward?

Stericycle integration is the most significant near-term catalyst. The $7.2 billion acquisition added medical waste handling, hazardous material management, and secure document destruction to WM’s portfolio.

Full integration synergies are expected to build through 2026 and 2027, contributing both incremental revenue and margin improvement that could accelerate the path toward the model’s 20.5% operating margin target.

Automation remains the other major driver of the margin story. WM is committed to achieving $450 million in annualized savings from automated collection vehicles and route optimization technology. Reducing driver headcount while improving route efficiency directly reduces operating costs, and those savings flow directly into operating margin expansion over time.

Renewable energy from landfill gas continues to grow as a high-margin revenue stream for WM. The company captures methane from its landfills and converts it to electricity or renewable natural gas. That business benefits from regulatory tailwinds supporting clean energy, and it carries very low incremental cost relative to traditional waste collection services.

WM’s $3 billion share repurchase authorization, announced in December 2025, signals management confidence in the stock’s intrinsic value. The annual shareholder meeting on May 12, 2026, could offer additional details on the automation roadmap, Stericycle synergy timeline, and capital return priorities for the remainder of the year.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Waste Management?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up WM, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track WM alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze WM stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!