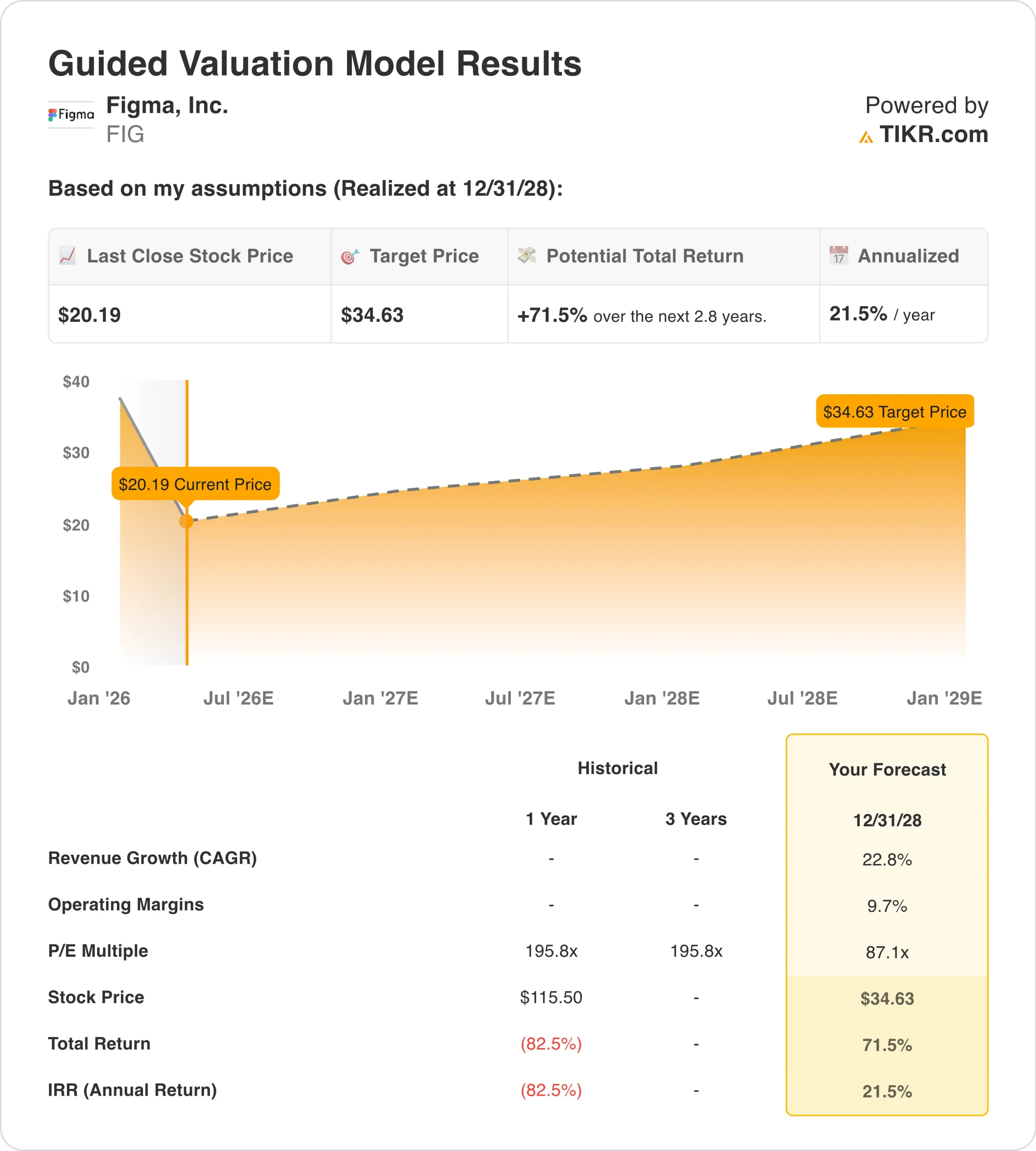

Key Stats for FIG Stock

- Past week’s performance: +3.5%

- 52-week range: $17 to $143

- Valuation model target price: $35

- Implied upside: +70.5% over 2.6 years

Value your favorite stocks like FIG with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Figma (FIG) is a cloud-based design and collaboration software platform used by product teams, designers, and developers worldwide. The company went public in August 2025 at $33 per share. But shares have since fallen to $21, well below the IPO price. The stock is down roughly 83% from the year’s high of $143.

The biggest recent catalyst for the selloff was Anthropic’s announcement of Claude Design in April 2026. Claude Design is an AI-powered design tool that competes directly with Figma’s core product offering. The announcement implied that large AI companies could begin displacing Figma’s design workflow. Shares dropped sharply after the news, and sentiment has remained cautious.

Mike Krieger, the Instagram co-founder and a Figma board member, also resigned from the board effective immediately in April. No formal reason was given. But the timing just before the Claude Design announcement added uncertainty and heightened investor concern about leadership stability.

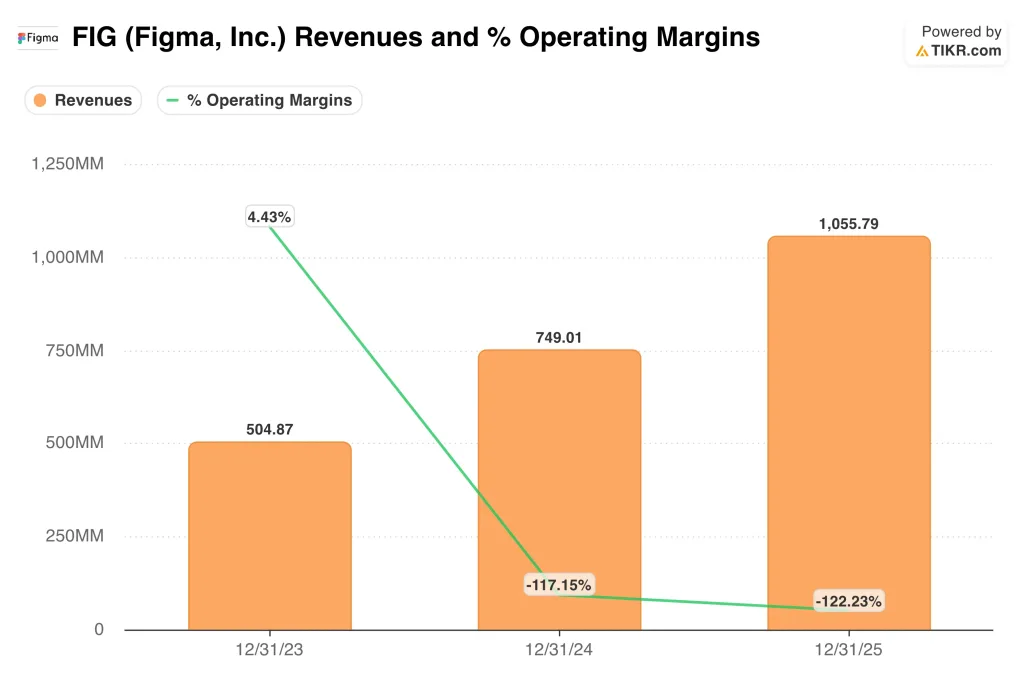

Despite the noise, Figma’s Q4 2025 revenue came in at $304 million, beating analyst estimates of $293 million. So the core business is still growing. Going forward, management must articulate a credible AI strategy to rebuild investor trust and stabilize the stock.

See analysts’ growth forecasts and price targets for FIG (It’s free) >>>

Is FIG Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 22.8%

- Operating Margins: 9.7%

- Exit P/E Multiple: 87.1x

Based on these inputs, the model estimates a target price of $35, implying 70.5% total upside from the current share price of $21 and a 22.3% annualized return over the next 2.6 years.

A 22.3% annual return is compelling on paper and puts Figma squarely in undervalued territory by this measure. But the assumptions carry meaningful risk given the AI competition from Anthropic, Adobe, and other well-capitalized players. Execution matters more than usual in this environment.

The revenue growth assumption of 22.8% requires continued customer retention and expansion. Figma’s Q4 revenue beat is a positive data point, and the company’s installed base of design professionals is enormous. But if AI-native tools successfully pull users away, those estimates could come under pressure quickly.

Gross margins at 82.4% reflect the efficiency of Figma’s subscription model. SaaS, or software-as-a-service, means customers pay recurring fees rather than one-time licenses, creating predictable revenue. However, operating losses remain large, and the path to profitability requires revenue to keep scaling faster than costs.

What’s Driving FIG Stock Going Forward?

The AI competition risk is the most important variable to monitor. Figma is rolling out its own AI tools, including Figma AI and the Figma Weave integration launched in April 2026. How quickly Figma’s AI features can match competing tools will determine market share outcomes.

Revenue growth remains strong in the near term. Fiscal 2025 revenue reached $1.06 billion, and the forward two-year revenue CAGR estimate stands at approximately 24.9%. But those estimates predate the Claude Design announcement and may be revised downward as analysts assess competitive risk.

Q1 2026 results arrive on May 14. Investors will be watching subscriber retention trends, management commentary on AI competitive impact, and full-year guidance. A strong quarter with reassuring commentary on AI could spark a meaningful recovery rally.

Figma’s partnership ecosystem is also worth monitoring. The platform integrates deeply with the product development stack, and switching costs are real. So the AI threat may prove easier for Figma to defend against than the market currently fears.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Figma?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FIG, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track FIG alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze FIG stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!