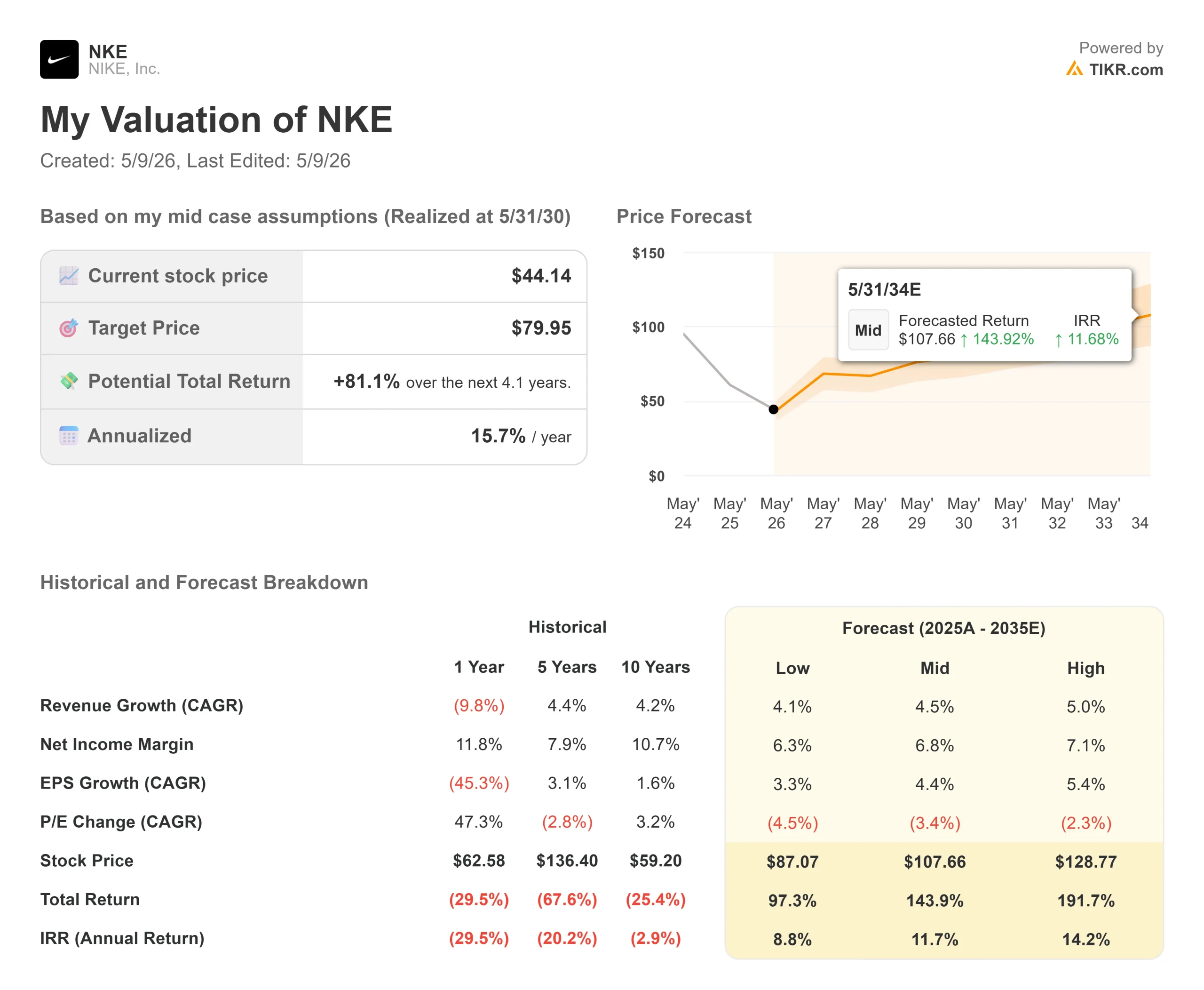

Key Stats for Nike Stock

- Current Price: $44.14

- Target Price (Mid): ~$80

- Street Target: ~$61

- Potential Total Return: ~81%

- Annualized IRR: ~16% / year

- Earnings Reaction: -15.51% (March 31, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Nike (NKE) has now lost 32% year to date, and on May 8, Wells Fargo added a new argument for why it could stay down longer.

The bank cut NKE to Equal Weight from Overweight and trimmed its price target to $45 from $55. Analyst Ike Boruchow argued that the rapid adoption of GLP-1 weight-loss medications, including Ozempic, Wegovy, and Zepbound, is shifting consumer wallets away from athletic footwear and toward traditional clothing, structurally weakening the category Nike dominates.

The timing is striking. Goldman Sachs, JPMorgan, and Piper Sandler all downgraded the stock in April, and NKE hit a 12-year low after its Q3 earnings in late March. Bulls argue Nike is a generational brand at a rare entry price. Bears argue the turnaround keeps missing its own timeline. The unresolved question is whether everything that could go wrong is already reflected in a stock trading near its 52-week low of $42.09.

The Q3 FY2026 earnings call and the TIKR model offer the clearest frame for answering that.

See historical and forward estimates for Nike stock (It’s free!) >>>

The Wells Fargo Thesis and What It Actually Targets

Wells Fargo’s downgrade was not primarily about Nike’s turnaround pace. It was about the category.

According to Wells Fargo’s research note, GLP-1 adoption is reshaping consumer wardrobes as users lose weight and replace athletic wear with traditional clothing. The firm estimated the trend added roughly 100 basis points to apparel spending growth in 2024 and around 120 basis points in 2025, with further lifts projected over the next two years. That shift benefits traditional clothing brands and cuts against athletic footwear makers like Nike.

The thesis is real, but it applies most directly to casual athletic spending, which maps to Nike’s Sportswear segment (classics-based footwear and streetwear). That is precisely the segment Nike has been deliberately cutting for four quarters. CEO Elliott Hill confirmed on the Q3 call that Nike has intentionally removed over $4 billion of revenue from peak Classics levels. Wells Fargo identified a structural risk in a part of the portfolio that Nike has already decided to shrink.

The performance categories Nike is actively rebuilding running, football, training, and basketball are tied to active exercise, which the GLP-1 framework would least penalize.

What the Earnings Call Revealed

Nike’s Q3 FY2026 results, reported March 31 for the quarter ended February 28, beat estimates and still sent the stock down 15.51%.

EPS came in at $0.35 against a consensus of $0.28, a 24% beat. Revenue of $11.28 billion edged past the $11.23 billion estimate. The drop came from guidance: management projected Q4 revenue down 2% to 4%, with Greater China guided down approximately 20%.

Inside the numbers, a sharp geographic split is taking shape. North America, which drives roughly half of total revenue, grew 3% in Q3, and wholesale surged 11%. According to Nike’s investor relations materials, CEO Elliott Hill noted that February marked the first time in two years that Nike drove positive growth across all channels in North America simultaneously. Running, Nike’s largest performance category, grew over 20%. Hill called it “the road map for other sports to follow.”

Outside North America, the picture is harder. Greater China fell 10% in Q3 and is guided down ~20% in Q4 as Nike cleans up its marketplace, a process Hill said will continue through fiscal 2027. EMEA revenue fell 7%, with elevated inventory expected to persist through Q4. Globally, Sportswear declined by low double digits.

CFO Matt Friend told investors: “While our comeback is taking longer than we would like, we are confident we are on the right path.”

Valuation: Still Premium, But the Dividend Is at a Rare Level

At $44.14, Nike trades at 27.01x next-twelve-months earnings and 18.63x NTM EV/EBITDA. Peers are substantially cheaper: On Holding AG trades at 12.80x NTM EV/EBITDA and ANTA Sports at 7.48x. The median NTM EV/EBITDA across Nike’s 23 comparable peers on TIKR is 8.72x. Nike trades at more than double that.

That premium is only defensible if Nike executes the recovery. On the income side, the stock now yields around 4.1%, a level rarely available in Nike’s history, and a byproduct of how far the stock has fallen.

See how Nike performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $44.14

- Target Price (Mid): ~$80

- Potential Total Return: ~81%

- Annualized IRR: ~16% / year

See analysts’ growth forecasts and price targets for Nike stock (It’s free!) >>>

The TIKR mid-case model targets approximately $80 by May 31, 2030, for around 81% total return at an annualized rate of roughly 16% per year.

The two revenue drivers are North America wholesale reacceleration, where Q3 already provides early evidence, and eventual Greater China stabilization as the inventory cleanup concludes. Together, they support a mid-case revenue CAGR of around 4.5%. The margin driver is the unwinding of Win Now restructuring costs: a $230 million severance charge in Q3 was part of converting Nike’s bloated fixed cost base to a more variable structure. Friend said benefits begin in fiscal 2027 and build through fiscal 2028. The mid-case net income margin recovers to around 7% by 2030, up from 4.8% reported in Q3.

The upside: North America momentum holds, the Sport Offense spreads to football and basketball on management’s timeline, and the fall Investor Day in Beaverton gives institutional investors the long-term framework they’ve been waiting for. The downside: Greater China extends past fiscal 2027, the GLP-1 shift blocks a Sportswear rebound before it starts, and a still-elevated multiple compresses further.

Of the 38 analysts covering NKE, 15 rate it Buy, 2 Outperform, 19 Hold, 1 Underperform, and 1 Sell. The mean Street target of approximately $61 implies around 38% upside, less than half the TIKR mid-case projection. The Street-low sits at $23, reflecting how wide the range of outcomes remains.

Conclusion

At the Q4 FY2026 earnings report on June 25, 2026, watch Greater China revenue against the guided ~20% decline. A shallower drop signals the cleanup is running ahead of schedule and is the most direct catalyst for a re-rating.

Nike is a 62-year-old brand trading at a 12-year low, absorbing deliberate pain to restore marketplace health. The TIKR mid-case model sees around 81% upside to May 2030. Whether that path opens depends on whether the North America playbook travels to EMEA, Greater China, and a Sportswear segment that needs to do more than stabilize.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Nike?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Nike, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Nike alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!