Key Stats for Alphabet Stock

- Current Price: $400.80

- Target Price (Mid): ~$610

- Street Consensus Target: ~$428

- Potential Total Return: ~53%

- Annualized IRR: ~10% / year

- Earnings Reaction: +9.96% (April 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Alphabet (GOOGL) crossed $400 for the first time this week, sitting at an all-time high roughly 10 days after its strongest earnings quarter in years. The Wall Street reaction has been one-sided. JP Morgan’s Doug Anmuth raised his target to $460 from $395 and called Alphabet the firm’s Top Overall Pick for 2026. Citizens Jmp set the Street-high target at $515. Mizuho maintained Outperform with a $460 target. More than 40 analysts raised their price targets following the report, per FactSet.

The lone dissent: Freedom Broker downgraded GOOGL from Buy to Hold while still raising its target to $400, citing valuation stretch at record prices. That tension between the bulls and the holdouts is what makes the stock worth examining right now.

Bulls point to 63% Cloud revenue growth and a backlog that nearly doubled in a single quarter. Bears point to free cash flow compression from surging capex and an NTM P/E of around 32x per TIKR. With Google I/O on May 19, 10 days away, the next catalyst is close.

What JP Morgan Is Actually Saying

Anmuth described the Cloud backlog expansion as “the single-most impressive metric this earnings season thus far.” His core argument is that Alphabet has moved from AI experimentation to contracted AI revenue, and the market has not yet priced in the full earnings impact.

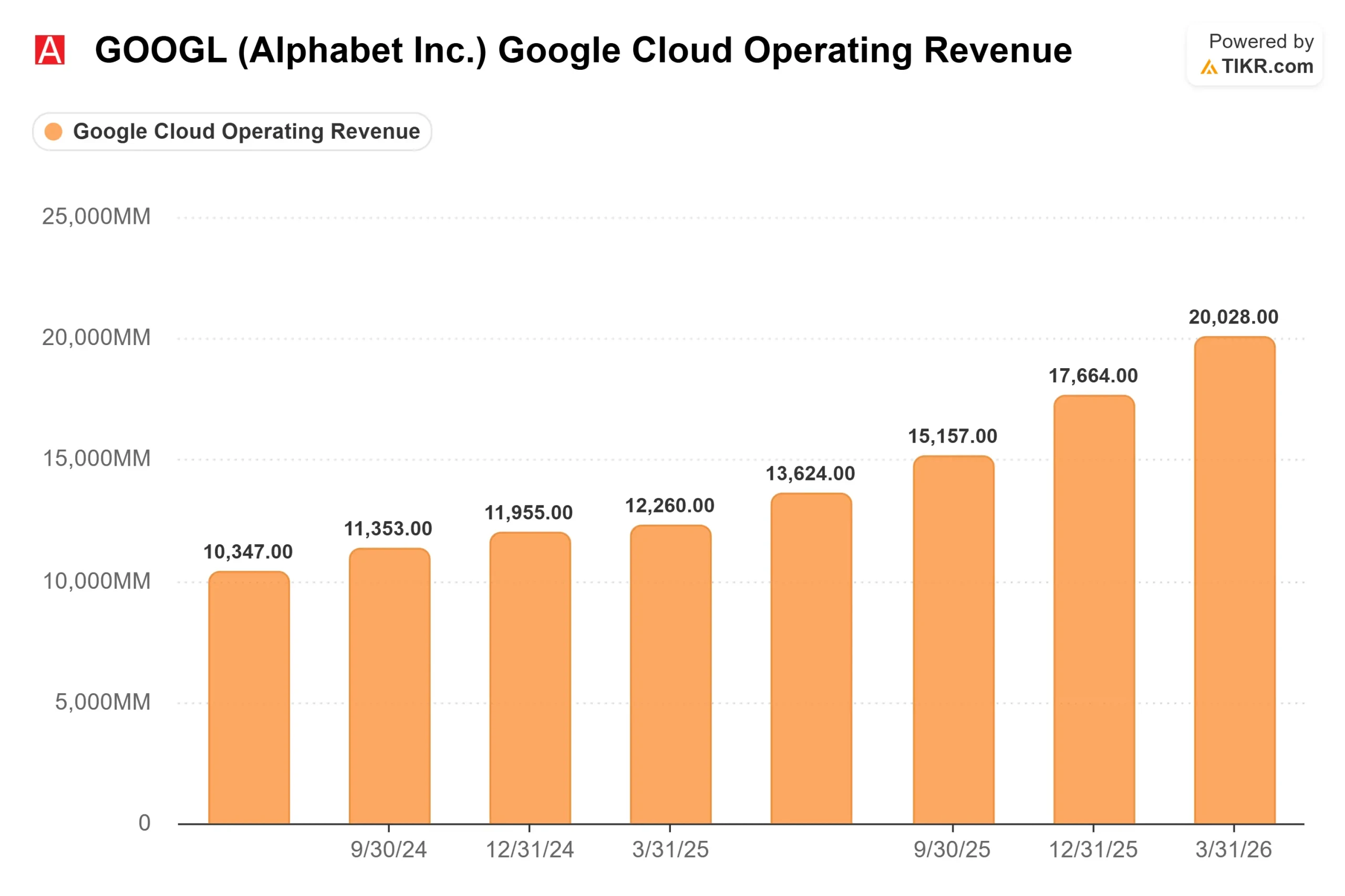

The Q1 numbers back that up. Cloud operating margin expanded from 17.8% to 32.9% in a single year, per CFO Anat Ashkenazi on the April 29 earnings call. Revenue from Cloud products built on Gemini models grew “nearly 800% year-over-year,” per CEO Sundar Pichai. New customer acquisition doubled year-over-year, and the number of $100 million-to-$1 billion deals signed also doubled. Anmuth’s thesis is that these metrics drive both earnings revisions and multiple expansion from here.

See historical and forward estimates for Alphabet stock (It’s free!) >>>

The Backlog Is the Real Story

Google Cloud’s committed future revenue nearly doubled sequentially to $462 billion at the end of Q1, per Ashkenazi. For context, Alphabet’s entire 2025 revenue was $402.8 billion per TIKR. More than half of the backlog is expected to convert to revenue within 24 months.

Pichai was direct about the constraint: “We are compute-constrained in the near term. Our cloud revenue would have been higher if we were able to meet the demand.” That is why Alphabet raised its 2026 capex guidance to $180–$190 billion and flagged that 2027 capex will “significantly increase” from that level.

The free cash flow picture reflects the investment: TIKR’s forward estimates show 2026 FCF at approximately $21 billion, down from $73.3 billion in 2025, before recovering to approximately $28 billion in 2027 and approximately $64 billion in 2028 as the infrastructure matures. The FCF trough is the bear argument, and it is real. The bull counter is that the $462 billion backlog makes the recovery trajectory visible.

Search and the Rest of the Business

The AI chatbot disruption bear case took another hit in Q1. Search and Other revenue grew 19% to $60.4 billion, and search queries hit an all-time high, per Pichai. AI Overviews and AI Mode are pulling more queries rather than displacing them. Schindler said Gemini’s improved understanding now enables monetization of “longer, more complex searches that were previously really difficult to monetize,” pointing to upside in Alphabet’s ad coverage rate.

The broader business adds context. Total paid subscriptions reached 350 million, driven by YouTube and Google One. Subscription, Platforms, and Devices revenue grew 19% to $12.4 billion. Subscriptions are growing faster than YouTube ads. Waymo surpassed 500,000 fully autonomous rides per week. These are not side businesses anymore.

On valuation, per TIKR’s Competitors page, Alphabet trades at 9.49x NTM EV/Revenues and 19.96x NTM EV/EBITDA, compared to Meta Platforms at 5.89x and 10.25x, respectively. Alphabet carries a significant premium, but it reflects a business that spans enterprise cloud, consumer AI subscriptions, digital advertising, and autonomous vehicles, not just social media ads.

See how Alphabet performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $400.80

- Target Price (Mid): ~$610

- Potential Total Return: ~53%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Alphabet stock (It’s free!) >>>

The TIKR mid-case uses a revenue CAGR of around 15% and a net income margin of around 34% through 12/31/30, arriving at a target of approximately $610. That is around 53% above today’s price, or roughly 10% annualized.

The two revenue drivers are Google Cloud, backed by a $462 billion backlog and constrained demand, and Search, which is accelerating as AI features drive query volume. The margin driver is Cloud’s operational leverage, which has already moved from 17.8% to 32.9% in a year and has further room as the backlog converts.

The primary risk is FCF compression persisting longer than the model assumes. If capex overshoots and revenue growth stalls before the infrastructure matures, the current multiple contracts. The upside: Cloud momentum accelerates as capacity comes online, and FCF recovers sharply from 2028 onward. Street sentiment reflects conviction: 44 Buys, 13 Outperforms, 6 Holds, 2 No Opinions, 0 Underperforms, and 0 Sells per TIKR’s Street Targets page, with a mean target of $427.89. JP Morgan’s $460 implies they see further multiple expansion that the consensus has not priced in.

Conclusion

The next catalyst is Google I/O on May 19, where Alphabet is expected to announce a next-generation Gemini model and new AI hardware. The number to watch is Gemini Enterprise’s paid monthly active user growth, which came in at 40% quarter-over-quarter in Q1. An acceleration going into Q2 validates the enterprise AI thesis. A deceleration gives the bears their argument.

Alphabet has answered whether its AI investments are working. The question now is whether the $462 billion Cloud backlog, 19% Search growth, and 350 million paid subscribers justify buying at an all-time high. The TIKR mid-case says yes at around 10% annually through 2030.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Alphabet?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Alphabet, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Alphabet alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Alphabet on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!