Key Stats for Micron Stock

- Current Price: $746.81

- Target Price (Mid Case): ~$525

- Target Price (High Case): ~$657

- Street Target (Mean): ~$556

- Potential Total Return (Mid Case): ~(29.6%) over 4.3 years

- Annualized IRR (Mid Case): ~(7.8%) / year

- Annualized IRR (High Case): ~(1.5%) / year

- Earnings Reaction: (3.78%) on March 18, 2026

- Max Drawdown: (30.31%) on March 30, 2026

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

The memory chip market has not felt like this in a long time. Micron Technology (MU) just posted its best week since December 2008, surging 38% to close at $746.81 on May 9, with the stock hitting a new all-time intraday high of $759.50. The market cap crossed $840 billion. Bulls say this is the start of a multi-year AI memory supercycle that the market still has not fully priced in. Bears point to a model target well below the current price and a CEO who sold $21.5 million in shares in early May. The question the rally is not answering: has the stock run so far that even a genuinely exceptional fundamental case can no longer keep up?

The Shortage Is Real, and Management Spelled It Out

The week’s move was a convergence. On May 5, Micron launched the 245TB 6600 ION SSD, the highest-capacity data center drive available. The next day, Mizuho analyst Vijay Rakesh raised his price target to $740 from $545, citing agentic AI (autonomous software that plans and acts without human input) as a new structural demand driver for memory. Retail net buying, according to Vanda Research, hit its highest level in two years in mid-April.

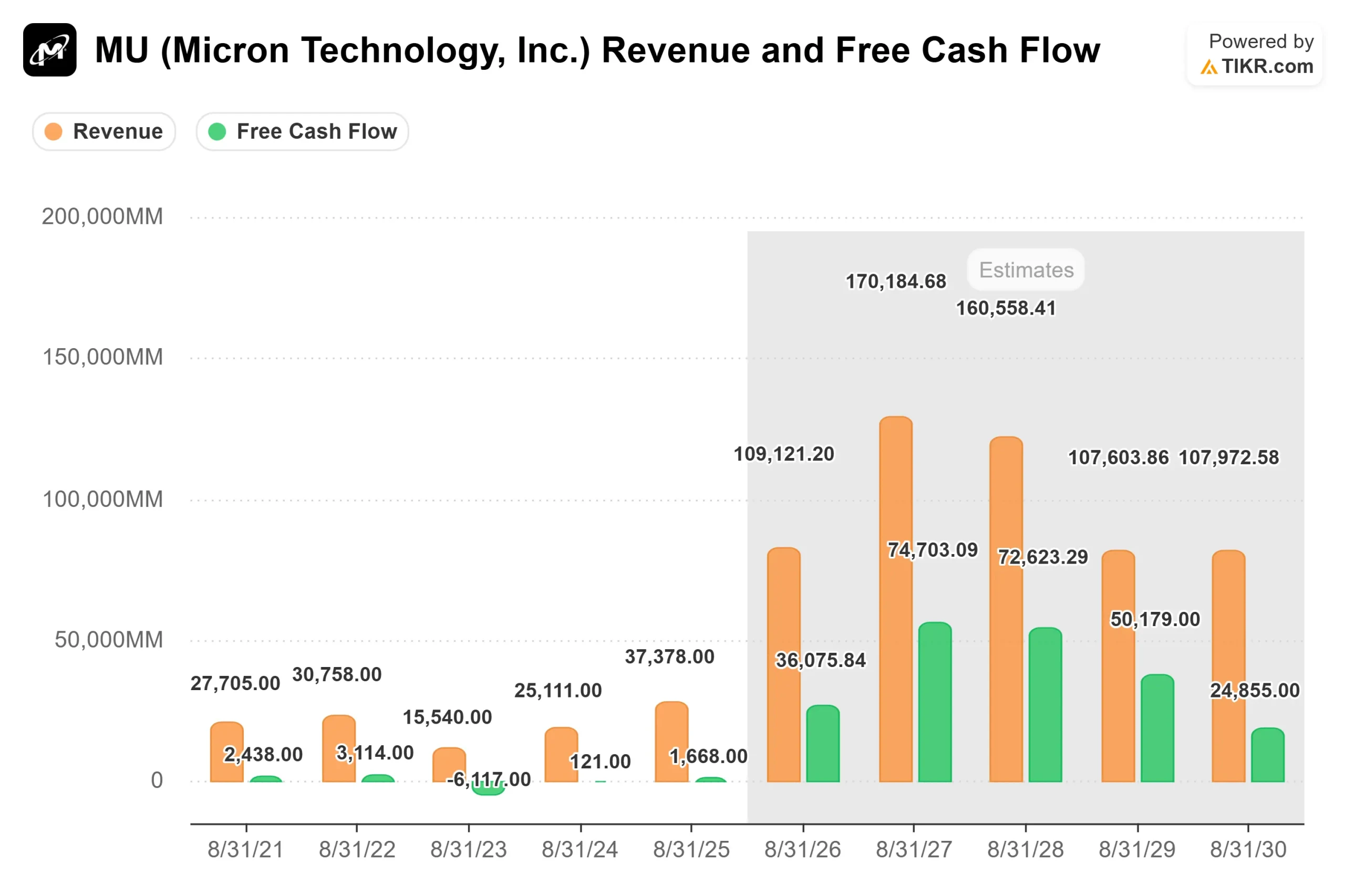

The earnings foundation is not manufactured. On March 18, Micron reported fiscal Q2 2026 results that shattered expectations. Revenue hit $23.86 billion, up 196% year over year, against the LSEG consensus of $20.07 billion. Non-GAAP EPS of $12.20 beat the Street’s $9.16 estimate by 33%. Q3 guidance of approximately $33.5 billion implies over 200% year-over-year growth. Yet the stock fell (3.78%) on the day, because even a historic result raised the question of what comes next.

The Q2 post-earnings analyst call answers that. Chief Business Officer Sumit Sadana said supply constraints will persist “for the foreseeable future and certainly beyond 2026.” CFO Mark Murphy confirmed, “demand far exceeds supply.” Micron’s entire 2026 high-bandwidth memory (HBM) capacity, the memory type vertically stacked to deliver the extreme bandwidth AI accelerators require, is contracted out. EVP of Global Operations Manish Bhatia confirmed the new Singapore cleanroom will not contribute meaningful supply until the second half of 2028. On how long the shortage lasts, Sadana put it plainly: “We don’t have a high confidence view yet as to when the supply will be able to catch up with demand because the escalation of demand from these various vectors is just very phenomenal.”

Robotics, multi-agent AI, and KV cache (how AI models temporarily store computation during inference) are all adding demand on top of the data center buildout. This came directly from management on the Q2 call, not from investor-relations slides.

See historical and forward estimates for Micron stock (It’s free!) >>>

The NAND Story That Gets Overlooked

The NAND business is being drowned out by the HBM narrative. Micron is the first company in the world to ship a Gen6 SSD, and Sadana said on the Q2 call that demand for it is “nowhere close to being met.” The 245TB 6600 ION drive targets AI data lakes and large-scale storage workloads, and Micron says it delivers equivalent storage capacity using 82% fewer server racks than hard-drive alternatives. KV cache demand has also grown into a meaningful source of data center NAND orders over the past year.

Where the Street Stands, and Where the Model Diverges

Of 46 analysts covering MU on TIKR’s Street Targets page, 30 rate it a Buy, 9 an Outperform, 4 a Hold, 1 No Opinion, 1 an Underperform, and 1 a Sell. The mean price target is $556.05. D.A. Davidson’s Gil Luria set a Street-high $1,000 target on May 4, arguing this memory cycle is structurally different from prior ones. TD Cowen’s Krish Sankar raised his target to $660 on April 28. Even the bulls are below where the stock trades today.

On valuation, TIKR’s Competitors page shows SK Hynix trading at 2.96x NTM EV/Revenues and 3.58x NTM EV/EBITDA, both well below Micron’s 5.21x and 6.12x. Kioxia sits at 4.75x NTM EV/Revenues. The sector mean across comparable semiconductor names is 7.70x NTM EV/Revenues, so Micron is not expensive relative to the broader group. The SK Hynix discount partly reflects a real competitive risk: according to semiconductor analysis firm SemiAnalysis, SK Hynix and Samsung together hold the majority of initial HBM4 supply share on NVIDIA’s Vera Rubin platform, with Micron resubmitting its qualification in Q2 2026. Winning that slot is the most important unresolved product question for the next twelve months.

See how Micron performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $746.81

- Target Price (Mid Case): ~$525

- Target Price (High Case): ~$657

- Potential Total Return (Mid Case): around (29.6%) over 4.3 years

- Annualized IRR (Mid Case): around (7.8%) / year

- Annualized IRR (High Case): around (1.5%) / year

See analysts’ growth forecasts and price targets for Micron stock (It’s free!) >>>

This is the number the rally does not want to discuss.

The TIKR scenario analysis uses a mid-case revenue CAGR of around 11% and a net income margin of around 84% through 8/31/30, arriving at $525.45, a total return of around (29.6%) and an annualized IRR of around (7.8%). The high case, using around 12% revenue growth and a margin of around 89%, reaches $656.82, with an IRR of around (1.5%). Every scenario ends in the red.

The model’s two revenue drivers: continued AI server DRAM content growth and HBM mix expansion, both confirmed by management on the Q2 call. The margin driver: the 1-gamma DRAM and G9 NAND node transitions, which Bhatia confirmed are running ahead of schedule on cost reductions. Micron’s balance sheet is the strongest in company history at Q2 close, with $6.5 billion in net cash. The primary risk is the cycle itself: TIKR consensus estimates show free cash flow peaking around FY2027 and declining materially through FY2029 and FY2030 as new capacity comes online and pricing normalizes. The stock is priced as if that normalization never arrives.

To be clear on what the model is not saying: the demand destruction thesis (where AI efficiency gains eliminate memory procurement) does not find support in the Q2 transcript. Sadana addressed CXL memory pooling concerns directly and argued the supply-demand gap is large enough that every available solution gets deployed alongside conventional DRAM, not instead of it. The model’s concern is simpler: even a prolonged shortage eventually ends, and the valuation multiples at $746 leave no margin for that history to repeat.

The bull case requires cleanroom constraints to stay binding through 2028, HBM content per accelerator to keep growing, robotics and agentic AI to deliver the new demand Sadana described, and Micron to win its HBM4 Vera Rubin requalification. Even if all of that goes right, the high-case model still does not get investors back to even over 4.3 years.

Conclusion

Watch Q3 FY2026 gross margin when Micron reports on June 24, 2026. Management guided approximately 81%. If it prints below 79%, that is the first concrete signal that non-HBM DRAM pricing is softening faster than the shortage thesis can support. The thesis in one sentence: Micron’s AI memory franchise has never been stronger, but at $746.81, the stock is priced for a scenario the TIKR model cannot reach under any of its three cases, and that gap is the risk investors accept when they buy the all-time high today.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Micron?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Micron, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Micron alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!