Key Stats for Abbott Laboratories Stock

- 52-Week Range: $84 to $139

- Current Price: $84

- Street Mean Target: $119

- Street High Target: $143

- Analyst Consensus: 16 Buys / 5 Outperforms / 7 Holds / 1 No Opinion

- TIKR Model Target (Dec. 2030): $

What Happened?

Abbott Laboratories (ABT), a diversified medical device, diagnostics, and nutrition company trading at $84.32, closed its $23 billion acquisition of cancer-test maker Exact Sciences on March 23, giving it access to Cologuard, the leading non-invasive colorectal cancer screening test, and Oncotype DX, a precision oncology tool used in therapy selection.

The deal is the largest acquisition in Abbott’s recent history, funded through a $20 billion senior notes offering completed in March, and it immediately added what CEO Robert Ford called “approximately $3 billion of incremental sales in 2026” to the Abbott portfolio.

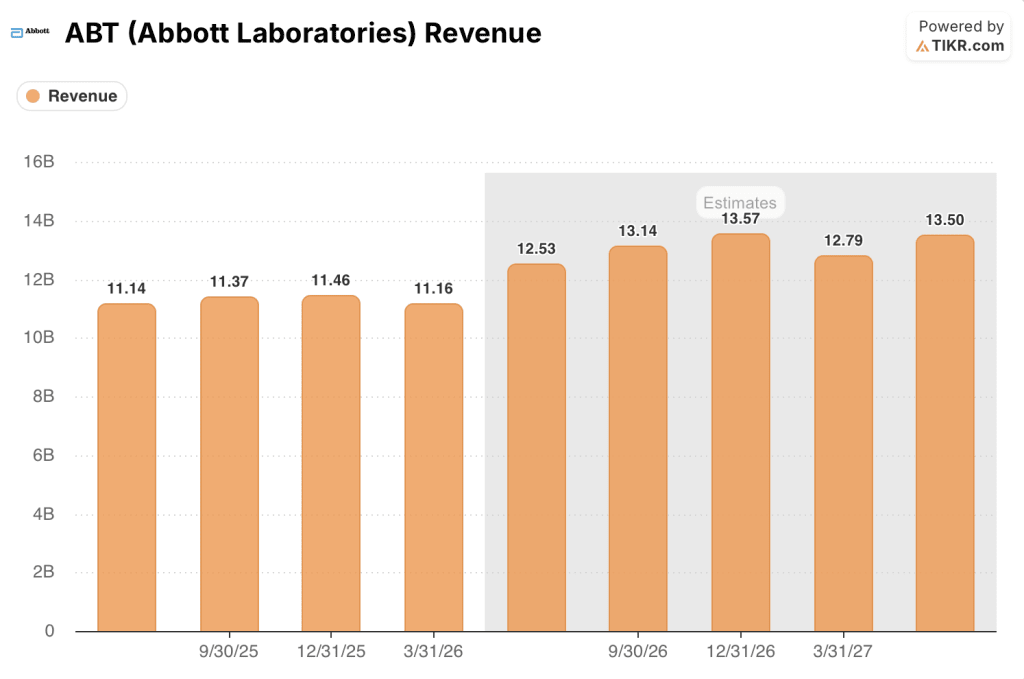

Q1 2026 results confirmed the acquisition hit its near-term targets: Abbott reported adjusted EPS of $1.15 against a Street estimate of $1.14, and revenue of $11.164 billion against an estimate of roughly $11 billion, with Cancer Diagnostics delivering 13% comparable sales growth led by mid-teens Cologuard volume growth and high-teens international diagnostics gains.

Ford stated on the Q1 2026 earnings call that “this acquisition adds a new high-growth business to the Abbott portfolio further strengthening our leadership position in Diagnostics and expanding our presence into one of the fastest-growing areas of health care,” framing Exact Sciences not as a bolt-on but as a beachhead into a $60 billion U.S. cancer screening and precision oncology market.

The Exact Sciences deal also positions Abbott to offset two structural pressures: declining COVID-19 testing revenue (down 60.2% in FY 2025 to $297 million) and near-term headwinds in its Nutrition segment, where pricing resets implemented in Q4 2025 are gradually rebuilding volume but remain a drag entering mid-2026.

The acquisition’s dilutive near-term impact (roughly $0.20 per share in 2026) triggered a guidance reduction: Abbott now guides full-year 2026 adjusted EPS to $5.38 to $5.58, down from $5.55 to $5.80, sending Abbott stock down roughly 5% on April 16 to its current level near the 52-week low of $84.08.

Wall Street’s Take on ABT Stock

The Exact Sciences acquisition compresses 2026 EPS on paper, but it accelerates Abbott stock’s long-term revenue profile into one of the highest-growth segments in diagnostics.

Abbott’s revenue is forecast to grow around 13% in Q2 2026 and around 15% in Q3 2026 on a comparable basis, driven by Cologuard volume expansion, a broadening PFA catheter rollout in electrophysiology, and the ongoing recovery in Core Lab Diagnostics as China’s volume-based procurement headwinds roll off, with the combined business now tracking toward around $54 billion in annual revenue by 2027.

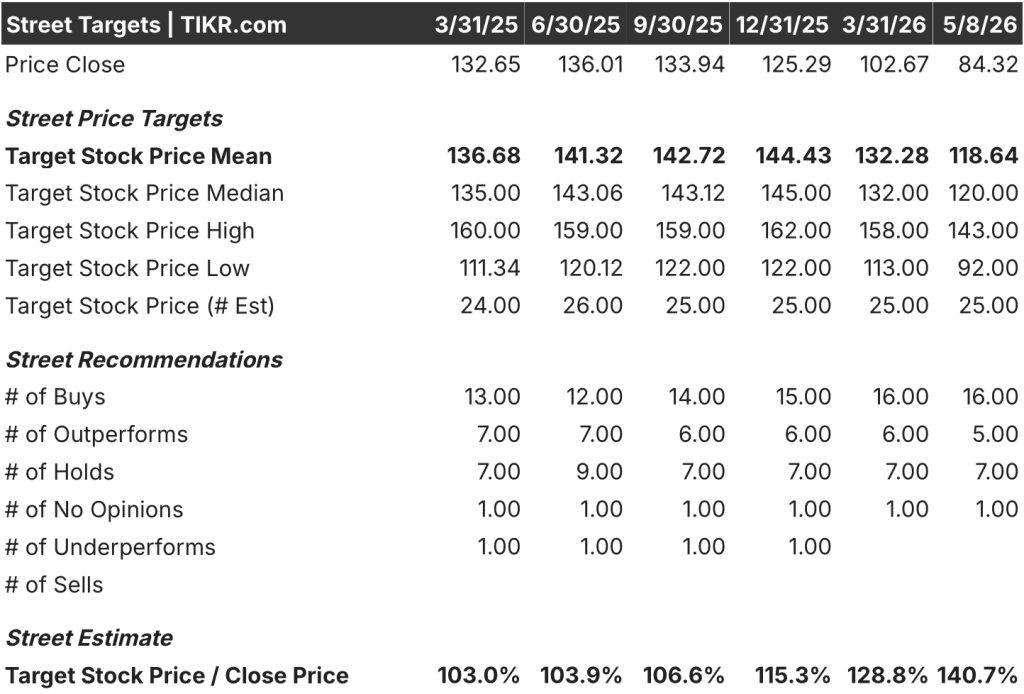

Covering analysts have 16 buys, 5 outperforms, and 7 holds against a mean price target of $118.64, implying roughly 41% upside from the current $84.32 price, with the Street waiting specifically for evidence that Cologuard’s rescreen momentum and international diagnostics expansion can offset Nutrition softness in the back half of 2026.

The target spread from $92 to $143 reflects a genuine debate: bears anchor to near-term EPS dilution, nutrition weakness, and the NEC infant formula litigation overhang (including a $70 million verdict in April), while bulls argue the Cologuard rescreen flywheel (25% of tests today, growing annually) and the underpenetrated CGM market (10 to 12 million users against a 70 to 80 million addressable population) create compounding revenue streams the current price ignores.

The risk is Nutrition: if volume recovery stalls beyond Q3 2026 and the pricing reset fails to restore the business to its historical mid-single-digit growth rate, the diversification thesis weakens materially.

Q2 2026 earnings (expected July 2026) are the first real test: watch whether CGM returns to double-digit growth as Ford guided, whether Cologuard holds mid-teens comparable growth, and whether Nutrition shows measurable sequential volume improvement.

What Does the Valuation Model Say?

TIKR’s mid-case model projects Abbott stock reaching $197 by December 2030, built on a revenue CAGR forecast of around 8% and net income margins expanding from 19.5% (1-year historical) to around 21%, a plausible trajectory if Cologuard scales internationally and CGM penetration extends into type 2 non-insulin patients, a reimbursement expansion Ford flagged as imminent on the Q1 call.

Against a mid-case IRR of around 10% annually through 2034 and a target of $141, priced at $84 today, Abbott stock appears undervalued with the market effectively pricing in permanent deal dilution rather than the higher-growth diagnostics business the Exact Sciences acquisition was built to create.

The central tension is timing: the bull thesis requires Abbott to execute on Cologuard international expansion, CGM reimbursement broadening, and Nutrition recovery simultaneously over the next 18 months, while absorbing $20 billion in new debt from the Exact Sciences financing.

What Has to Go Right:

- Cologuard hits double-digit comparable growth through 2027, supported by rescreens (currently 500,000 annually), care gap programs, and a potential reduction in CRC screening age guidelines from 45 to 40 (adding around 20 million eligible Americans)

- CGM returns to double-digit growth in Q2 2026 as guided, supported by type 2 non-insulin proposed reimbursement language Ford expects “coming soon”

- Core Lab Diagnostics sustains mid-single-digit growth as China VBP headwinds (roughly $1 billion drag in 2025) fully roll off, with U.S. contract renewal rates above 90% and win rates above 55% already established

- Electrophysiology accelerates through H2 2026 with broadened launches of Volt PFA (U.S.) and TactiFlex Duo (Europe), with Abbott targeting market share above the mid- to high-teens market growth rate by year-end

What Could Go Wrong:

- NEC infant formula litigation (nearly 1,000 lawsuits pending, including a $70 million April verdict and a prior $495 million verdict under appeal) creates escalating financial and reputational exposure that diverts management focus and cash

- Nutrition pricing resets fail to restore volume growth by Q3 2026, eliminating a key segment from the portfolio-level diversification argument

- The $20 billion senior notes offering raises Abbott’s debt load to levels that constrain capital return (currently $6.7 billion remaining in buyback authorization) if Exact Sciences integration runs behind on its $3 billion 2026 incremental revenue target

- Structural Heart faces competitive pressure from Edwards Lifesciences’ expanding mitral portfolio, with Abbott’s U.S. execution acknowledged as needing improvement on the Q1 call

Should You Invest in Abbott Laboratories?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Abbott Laboratories stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Abbott Laboratories alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ABT stock on TIKR for Free →