Key Stats

- Current Price: $197 (May 8, 2026)

- Q1 2026 Revenue: $881M, up 23% YoY

- Q1 2026 Non-GAAP EPS: $2.72, up 53% YoY

- Q1 2026 Non-GAAP Operating Margin: 18%, up 4 points YoY

- Total Customers: ~300,000, up 16% YoY

- Full-Year 2026 Revenue Guidance: $3.7B to $3.708B, up 18% YoY

- Full-Year 2026 Non-GAAP EPS Guidance: $13.04 to $13.12

- Full-Year 2026 Non-GAAP Operating Margin Guidance: ~21%

- TIKR Model Price Target: $448 (mid case)

- Implied Upside: ~127%

HubSpot Q1 2026 Earnings Breakdown

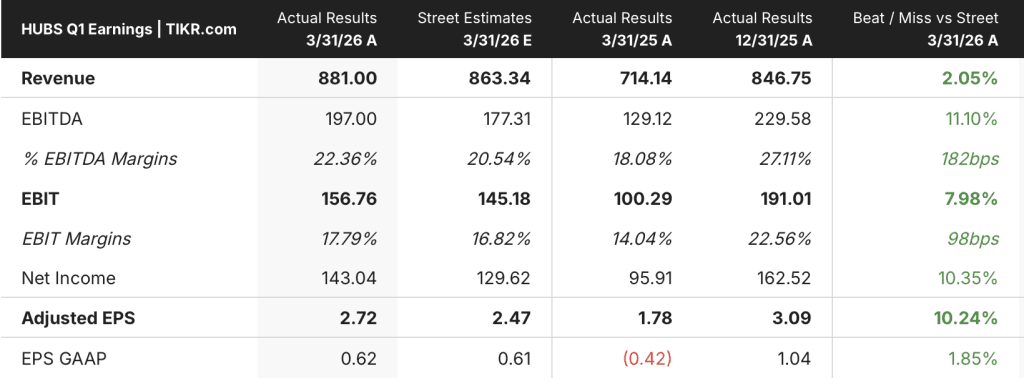

HubSpot stock (HUBS) delivered Q1 revenue of $881M, up 23% year-over-year, with non-GAAP EPS of $2.72, up 53% from $1.78 in the prior-year period.

Non-GAAP operating margin expanded 4 points year-over-year to 18%, according to CFO Kate Bueker on the Q1 earnings call, reflecting disciplined hiring, FX tailwinds, and changes to the partner commissions program.

The customer count milestone was significant: total customers reached nearly 300,000, a 16% year-over-year increase, driven by nearly 10,800 net additions in the quarter.

Upmarket momentum was the strongest growth driver, with deals over $60,000 ARR growing 37% year-over-year and deals over $120,000 ARR growing 64% year-over-year, according to CEO Yamini Rangan on the Q1 earnings call.

Multi-hub adoption continued its climb, with 63% of new Pro+ customers landing with multiple hubs in Q1, up 3 points year-over-year, and 42% of the Pro+ installed base by ARR now owning 4 or more hubs, up 6 points year-over-year.

AI monetization is gaining measurable traction: active core seat users grew 90% year-over-year, and total credits consumed grew 67% quarter-over-quarter, according to Rangan on the Q1 earnings call.

HubSpot stock’s forward guidance reflected both strength and near-term friction.

Full-year 2026 revenue guidance was raised to $3.7B to $3.708B, up 40 basis points from the prior guide, while full-year non-GAAP operating margin guidance was raised to 21%, reaching the company’s 2027 target a year ahead of schedule, according to Bueker on the Q1 earnings call.

Q2 2026 revenue guidance was set at $897M to $898M, representing 18% year-over-year growth, with non-GAAP operating margin guided to 19% and non-GAAP EPS of $3.00 to $3.02.

The near-term friction: in April, HubSpot made deliberate pricing and go-to-market changes tied to its Spring Spotlight product launch, including lowering the price of Customer Agent, moving to outcome-based pricing for Customer and Prospecting Agents, and introducing 28-day free trials for agents and HubSpot AEO, according to Bueker on the Q1 earnings call.

Those changes reduced sales capacity in April as reps were retrained, leading to a slow start to Q2, which is already embedded in the guidance.

HubSpot repurchased $211M of stock in Q1 under its current $1B share repurchase program, and generated $154M in free cash flow, representing 17% of revenue.

HubSpot Stock Financials: Operating Leverage Taking Hold

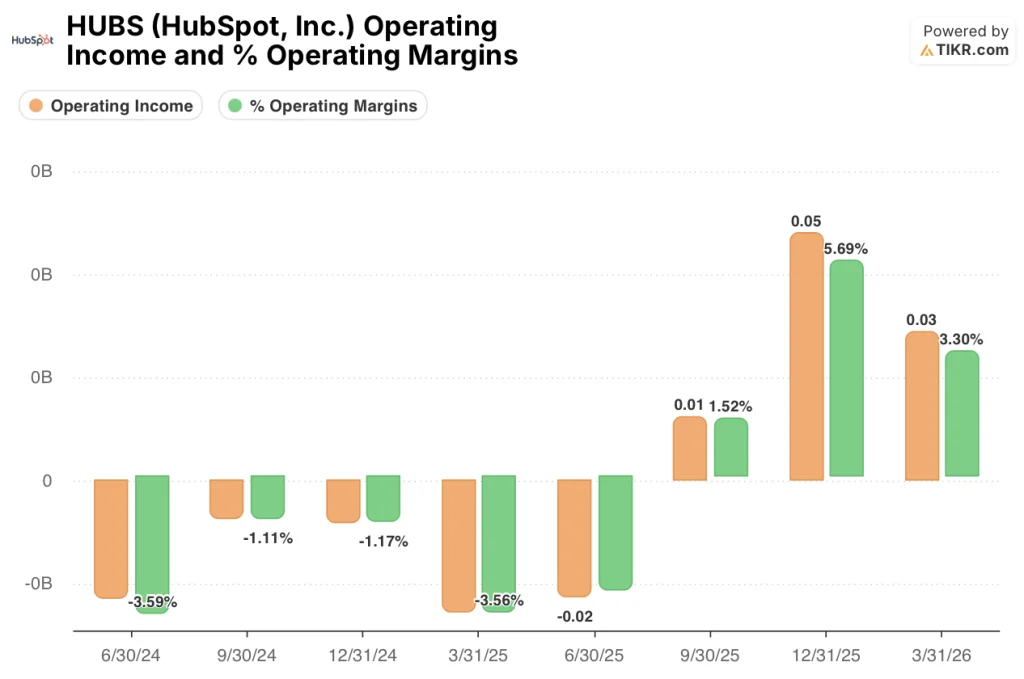

The Q1 2026 income statement tells a clear operating leverage story: GAAP operating income turned positive and held, even as the company accelerated investment in AI.

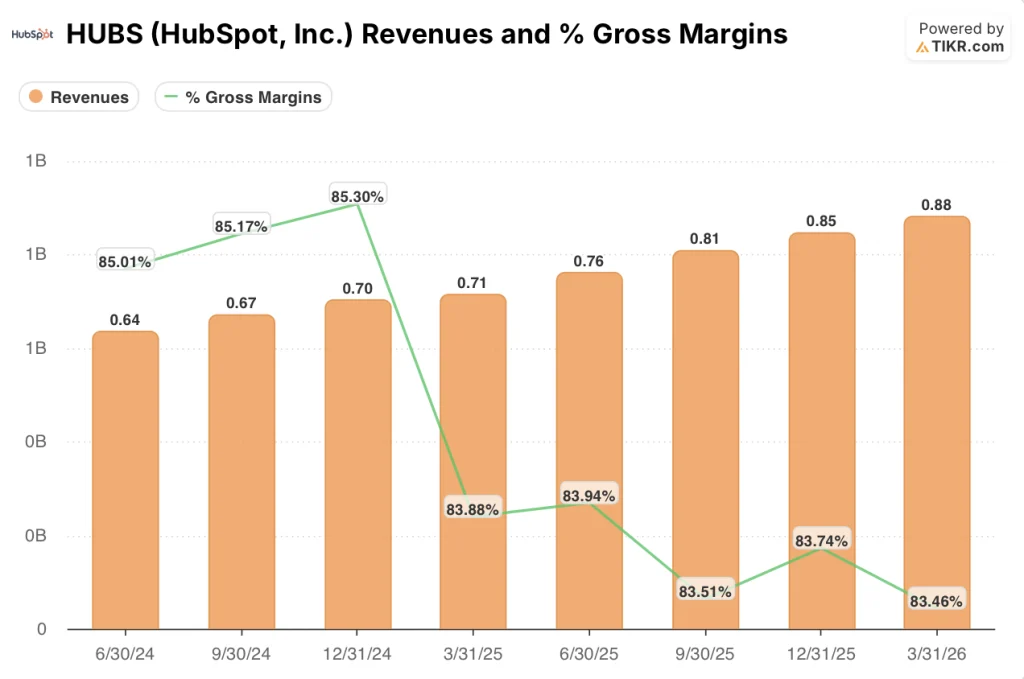

Revenue has grown steadily across eight quarters, from $640M in Q2 2024 to $880M in Q1 2026, with YoY growth accelerating to 23% in Q1 2026 from 16% in Q1 2025.

Gross margin has compressed modestly, moving from 85% in Q2 2024 and Q3 2024 to 84% in Q1 2025 and Q1 2026, as COGS rose with platform scale.

HUBS stock’s operating income moved from a loss of $20M in Q2 2024 to positive $30M in Q1 2026, with operating margin improving from negative 3.6% to 3.3% over that span.

The most notable move came in Q3 and Q4 2025, where GAAP operating margin reached 1.5% and 5.7% respectively before settling at 3.3% in Q1 2026, a typical seasonal step-down from Q4 peaks.

Non-GAAP operating margin reached 18% in Q1 2026, up from 14% in Q1 2025, a 4-point expansion, according to Bueker on the Q1 earnings call, who described it as “investing aggressively in AI innovation while expanding operating margins at the same time.”

What Does the Valuation Model Say?

The TIKR model sets a mid-case price target of $448 for HubSpot stock, implying roughly 127% upside from the current price of $197.

The mid-case assumes a revenue CAGR of 16.8% through 2035, a net income margin of 21.3%, and an EPS CAGR of 19.7%, with P/E contraction of 9.7% annually factored in.

The high case reaches $1,141 on an 18.5% revenue CAGR and a 22.5% net income margin, while the low case implies $613 on 15.1% revenue growth and a 19.9% net income margin.

Q1’s combination of a clean revenue beat, 4 points of non-GAAP margin expansion, and a raised full-year guide strengthens the base of the model’s assumptions, even as the April pricing reset introduces execution risk in the near term.

At roughly $197, HubSpot stock is priced for a scenario where the AI transition stumbles. The model suggests investors are leaving meaningful return on the table if the credit and core seat monetization ramp plays out as guided.

The investment case for HubSpot stock now hinges on whether April’s pricing reset and go-to-market disruption is a one-quarter friction cost or the start of a longer recalibration.

What Has to Go Right

- Credit consumption, up 67% quarter-over-quarter in Q1, needs to sustain momentum in Q2 and beyond; Bueker cited seats and credits as the primary drivers of the guided 1 to 2 point net revenue retention expansion for full-year 2026

- Upmarket wins, with deals over $120,000 ARR growing 64% year-over-year in Q1, must continue providing a durable revenue floor as mid-market linearity shifts back-end loaded

- Over 15,000 Pro+ customers activated HubSpot AEO in trial during Q1; converting those trials to paid credit consumption is required to validate the new outcome-based pricing model

- Non-GAAP operating margin must hold at or above 21% for full-year 2026, reaching the 2027 target a year early, as the company absorbs increased AI infrastructure investment

What Could Still Go Wrong

- Q2 got off to a slow start due to sales retraining in April, and extended deal evaluation periods from 28-day agent trials could push revenue recognition into Q3, compressing the first half

- Q1 net new ARR growth came in below constant currency revenue growth, against what Bueker described as a more difficult comp; the full-year assumption requires net new ARR to recover and exceed constant currency revenue growth by year-end

- Organic search traffic across HubSpot’s customer base is down 27% this year, according to Rangan on the Q1 earnings call, which pressures demand generation if AEO adoption does not scale fast enough to offset the decline

- Customer Agent resolution rates, now at 70%, are a key proof point for outcome-based pricing credibility; any degradation in resolution quality or model performance would undercut the pricing thesis before it matures

Should You Invest in HubSpot, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HubSpot, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track HubSpot, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HUBS stock on TIKR for Free →