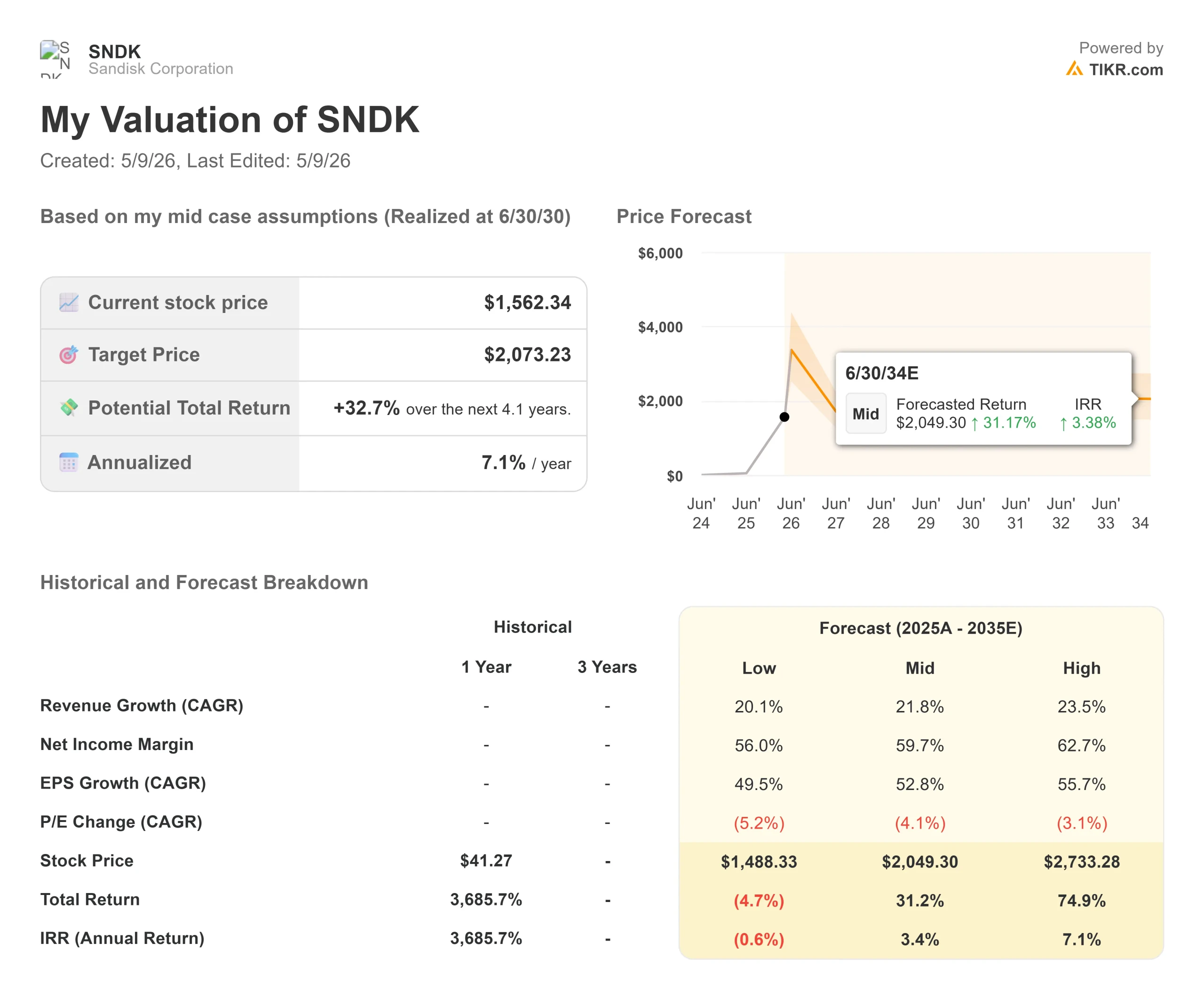

Key Stats for Sandisk Stock

- Current Price: $1,562.34

- Target Price (Mid Case): ~$2,070

- Street Target: ~$1,399

- Potential Total Return (Mid Case): ~33%

- Annualized IRR (Mid Case): ~7% / year

- Earnings Reaction: +8.25% (May 1, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Sandisk (SNDK) is trading above its own Street consensus target, and Western Digital just moved to exit its remaining stake entirely. Investors following the story through investor relations materials can see a company that has become one of the most debated valuation questions in the semiconductor sector. For a stock up more than 460% year-to-date, those two facts could read as warning signs. Bulls argue the opposite: the Street is behind, the overhang is clearing, and the structural demand thesis has gotten stronger. Bears say 80% gross margins in a commodity memory market are a cycle peak. The central question is whether $1,562 is a reasonable price to pay for what comes next.

The answer hinges on three things the earnings transcript made clear: the depth of the new business model contracts, the AI workload thesis pulling NAND demand beyond what most forecasts assumed, and a product ramp in Q4 that adds another growth layer on top of an already record quarter.

Western Digital Clears the Overhang

The most important development since Sandisk’s April 30 earnings report came from Western Digital, not Sandisk. On May 5, 2026, Western Digital disclosed agreements to exchange 653,203 Sandisk shares for approximately 1,865,801 shares of its own stock, settling on May 7. Western Digital retains 1,038,681 SNDK shares and has stated it intends to dispose of those through subsequent exchanges or distributions to shareholders.

Western Digital acquired Sandisk in 2016 for $19 billion and completed a tax-free spinoff in February 2025. Its residual stake had been a known overhang, a large blockholder with no long-term incentive to hold. With WD signaling a full exit, that pressure is resolving. For investors who want pure-play NAND exposure to the AI buildout, Sandisk’s equity story is cleaner today than at any point since it relisted.

See historical and forward estimates for SanDisk stock (It’s free!) >>>

What the Earnings Call Transcript Said That the Market Hasn’t Fully Priced

Sandisk’s Q3 FY2026 numbers were widely covered: revenue of $5,950 million, up 97% sequentially and 251% year-over-year, against guidance of $4,400 to $4,800 million. Non-GAAP gross margin hit 78.4% against a 65% to 67% guide. Non-GAAP EPS was $23.41 against a $14.66 consensus, a 59.67% beat per TIKR. What has been less absorbed is the demand trajectory CEO David Goeckeler described.

On the data center, Goeckeler said: “Before what we saw this week, we would raise even our calendar year ’26 data center growth number to the mid-70s percent from where we were in the 60s percent just three months ago, which is up from the 40s percent three months before that and the 20s percent three months before that.” Every quarter, the forecast gets revised up, and reality still beats it.

The reason ties to how AI infrastructure works. Goeckeler explained KV cache, the temporary memory layer that large language models use to avoid reprocessing input tokens during inference. As models advance toward reasoning and agentic tasks (where the model takes sequences of actions rather than a single output), the KV cache requirement grows with context length and concurrent sessions. The flash requirement, he said, “is well beyond the model itself, as systems must retain context, intermediate data, and large external data sets.” Retrieval-augmented generation, or RAG (which lets AI systems pull from live external knowledge bases rather than relying solely on training weights), adds another storage-intensive layer on top. These are live hyperscale workloads today, and they are why Sandisk’s data center revenue grew 233% sequentially in a single quarter.

The $42 Billion Backlog Is Structured Like Enterprise Software

Five new business model agreements, or NBMs, are signed. Three closed in Q3 FY2026; two more followed in Q4’s opening weeks. The three Q3 contracts carry a minimum contractual revenue of approximately $42 billion, appearing in Sandisk’s 10-Q as remaining performance obligations (RPO), a metric more common in software than NAND. Across all five agreements, financial guarantees exceed $11 billion, with $400 million in prepayments already on the balance sheet. They cover more than one-third of Sandisk’s expected bit shipments in fiscal year 2027.

What sets them apart from ordinary supply deals is the enforcement structure. CFO Luis Visoso said on the call: “There are different financial instruments that we’re using to protect us… if there is a breach in the contract that doesn’t go all the way to the end… that financial commitment immediately comes to us as a compensation.” These are multi-year purchase obligations backed by third-party financial institutions, with durations up to five years and pricing that blends fixed near-term rates with variable longer-term components.

The fixed/variable mix is the bear case. If NAND supply ramps and spot prices fall, the variable portions could reset lower. Goeckeler said the company is “not necessarily interested in trading away that value for certainty,” adding that the goal is getting both fair value and demand certainty simultaneously. The Q4 EPS guide of $30 to $33, roughly double analyst models, is, per management, consistent with the economics of the contracts already locked in. Goeckeler also said NBM bit coverage can reach “above 50%” and potentially higher, with negotiations ongoing. If that happens, the cyclicality argument against the stock weakens considerably.

The Valuation: Cheaper Than It Looks on Forward Multiples

The Street consensus target of $1,399.05 sits below the current price of $1,562.34, but that figure reflects estimates set before Q3. Post-earnings, Bernstein raised its target to $1,700 (Outperform), Susquehanna set a $2,000 target, and Mizuho raised its target to $1,625 (Outperform) on May 7. Per TIKR, the 22 analysts covering Sandisk show 15 Buys, 2 Outperforms, 4 Holds, and 1 Underperform.

The forward multiples from TIKR tell a more current story. Sandisk trades at 5.80x NTM (next twelve months) EV/Revenue and 8.15x NTM EV/EBITDA. Western Digital (WDC) trades at 10.01x NTM EV/Revenue and 20.83x NTM EV/EBITDA. Samsung Electronics trades at 2.19x NTM EV/Revenue and 3.69x NTM EV/EBITDA, reflecting its diversified mix across consumer electronics, displays, and foundry. Sandisk is cheaper than Western Digital on every forward multiple despite carrying a net cash balance sheet of $3,528 million and a forward free cash flow yield of around 8%, per TIKR.

Those multiples look compressed because the forward estimates embed massive growth. TIKR consensus projects a forward 2-year revenue CAGR of around 139% and a forward 2-year EBITDA CAGR of around 500%, driven by the Q4 ramp and NBM revenue flowing through FY2027. At 9.85x NTM P/E, the stock is not pricing in a premium for that growth. The risk is that those estimates assume NAND pricing strength that the variable contract terms may not fully protect against if supply conditions ease in 2027 to 2028.

According to Gartner, NAND flash memory prices are projected to rise 234% in 2026, with supply expected to remain tight through 2028. That supports near-term estimate confidence. The uncertainty is what happens when greenfield capacity eventually arrives.

The Q4 Catalyst: QLC Stargate and the Pipeline Beyond It

Sandisk guided Q4 FY2026 revenue of $7,750 to $8,250 million, with non-GAAP gross margin of 79% to 81% and non-GAAP EPS of $30 to $33.

Two things drive it. First, the QLC Stargate product begins shipping for revenue in Q4. QLC (quad-level cell) stores four bits per cell versus three for TLC, delivering higher storage density at lower cost per bit. Stargate has been in hyperscaler qualification for over a year. TLC remains the go-to for compute-intensive inference workloads; QLC handles high-density AI storage.

Second, Sandisk deliberately built BiCS8 inventory in Q3. BiCS8 is Sandisk’s latest 3D NAND generation, co-developed with Kioxia, which stacks memory cells vertically for higher density. That build is why bit shipments fell in the high-teens sequentially while revenue surged, and it sets up Q4’s ramp.

Longer term, Goeckeler said high-bandwidth flash (HBF), a NAND-based architecture designed for AI inference memory, is on track to have its NAND die ready “late this year” with the full system, including controller, in “early mid next year.”

The $6 billion share buyback has no expiration date. Sandisk closed Q3 with $3,735 million in cash and zero long-term debt after repaying its final term loan balance.

See how Sandisk performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $1,562.34

- Target Price (Mid Case): ~$2,070

- Potential Total Return (Mid Case): ~33%

- Annualized IRR (Mid Case): ~7% / year

See analysts’ growth forecasts and price targets for SanDisk stock (It’s free!) >>>

The TIKR mid-case, realized at 6/30/30, projects a target of ~$2,070, implying ~33% total return and approximately 7% annualized IRR from today’s price. Two revenue drivers underpin it: AI data center SSD demand from inference and agentic workloads, and the NBM structure converting episodic pricing upside into committed recurring revenue. The margin driver is operating leverage, as non-GAAP opex fell from 13.7% to 7.5% of revenue in Q3 alone, a trend that compounds further as high-margin data center revenue grows faster than the cost base.

The high case at ~$2,730 implies ~75% total return, requiring a revenue CAGR of around 24% and a net income margin near 63%. That needs continued NAND pricing strength and NBM coverage above 50%. The low case at ~$1,490 reflects margin compression if variable contract terms reset lower as supply catches up. At 8.15x NTM EV/EBITDA, the market is not pricing Sandisk like a software business. Whether the NBM structure earns that re-rating is the unresolved question: if it does, the mid-case is conservative; if NAND margins mean-revert, the low case is the floor.

Conclusion

Watch NBM bit coverage at Q4 FY2026 earnings, expected in late July 2026. Management says coverage is currently over one-third of FY2027 bits. If it crosses 50%, the de-cyclicalization thesis earns real credibility, and the 9.85x NTM P/E starts looking like a floor. If it stalls below 40%, the variable pricing risk dominates the debate. The WD overhang is clearing, the QLC Stargate ramp is live, and agentic AI workloads are pulling NAND demand beyond what most models assumed. SanDisk is no longer just a storage company. It is a test of whether a NAND manufacturer can permanently command a software-adjacent multiple.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in SanDisk?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SanDisk, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SanDisk alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze SanDisk on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!