Key Stats

- Current Price: ~$23 (May 8, 2026 close)

- Q1 2026 Revenue: $689M, +12% YoY

- Q1 2026 Adjusted EPS: $0.28

- Q1 2026 Adjusted EBITDA: $206M, 30% margin

- Q2 2026 Revenue Guidance: At least $750M

- Q2 2026 Adjusted EBITDA Guidance: ~$260M

- Full-Year 2026 Adjusted EBITDA Margin Guidance: At least 40%

- TIKR Model Price Target: ~$36

- Implied Upside: ~57%

The Trade Desk Stock Q1 2026 Earnings: 12% Revenue Growth Masks a Deteriorating Margin Story

The Trade Desk (TTD) posted Q1 2026 revenue of $689M, up 12% year-over-year, while adjusted EBITDA came in at $206M at a 30% margin.

The growth deceleration is the headline pressure: The Trade Desk stock has posted YoY revenue growth rates of 25.4%, 18.7%, 17.7%, and 14.3% across the prior four quarters, and Q1’s 12% marks the lowest growth rate in that sequence.

CTV and audio were the channel-level drivers, with video (including CTV) representing a low-50s percent of business and audio growing faster than any other channel in the quarter, according to Interim CFO Tahnil Davis on the Q1 earnings call.

Geographically, the United States represented approximately 82% of Q1 revenue, with international at approximately 18%, per Davis, with EMEA and APAC both showing strong momentum.

Among verticals, medical health, automotive, and events posted particularly strong growth, while Home & Garden and Food & Drink faced ongoing pressure from CPG brands navigating geopolitical uncertainty and input cost inflation, according to Davis.

March was the biggest month on record for Joint Business Plan signings, according to CEO Jeff Green: 45 JBPs signed in March alone, total Q1 JBP count up 55% year-over-year, and new JBP deal spend (excluding renewals) up 40% year-over-year.

Green also highlighted a competitive win in pharma, where The Trade Desk recaptured a major client from Amazon’s PG platform and signed a JBP for 2026 that will increase the client’s spend on the TTD platform by 114% year-over-year.

The company used $164M to repurchase Class A common stock in Q1 and ended the quarter with approximately $1.4B in cash, cash equivalents, and short-term investments.

Q2 2026 guidance calls for revenue of at least $750M and adjusted EBITDA of approximately $260M, with full-year adjusted EBITDA margin expected to be at least 40%, approximately in line with 2025, per Davis.

On the Publicis partnership question raised during the Q&A, Green confirmed negotiations are ongoing but declined to provide further detail, stating only that the company has done billions of dollars of business with Publicis since 2018 and continues to discuss the next chapter of the relationship.

Chief Strategy Officer Samantha Jacobson’s departure to OpenAI was confirmed during the call; Green noted she will remain on The Trade Desk’s Board of Directors.

The Trade Desk Stock: Financials

The Trade Desk stock’s income statement shows a margin profile under steady compression, with gross margin declining from a recent peak while operating leverage remains thin at the start of the year.

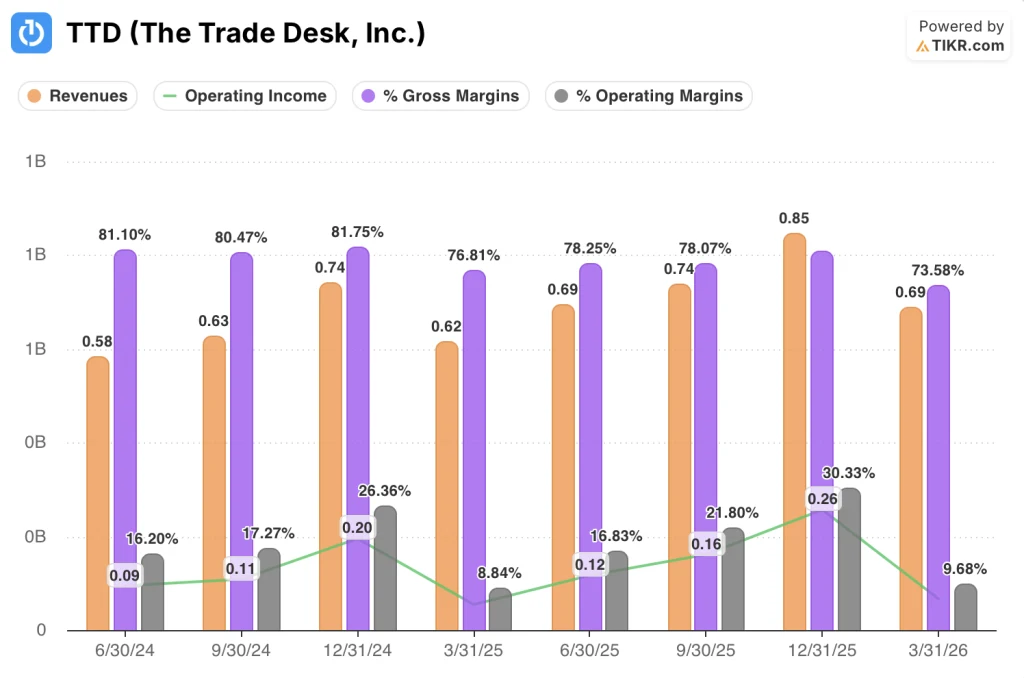

Revenue ran at $620M in Q1 2025, $690M in Q2 2025, $740M in Q3 2025, and $850M in Q4 2025 before stepping back to $690M in Q1 2026, consistent with seasonal patterns but at a slower growth pace than prior first quarters.

Gross margin peaked at 82% in Q4 2024, compressed to 77% in Q1 2025, partially recovered to 78% through Q2 and Q3 2025, reached 81% in Q4 2025, and stepped back to 74% in Q1 2026, the lowest in the eight-quarter sequence shown.

Operating margin followed a similar trajectory: 9% in Q1 2025, recovering to 17%, 22%, and 30% across the following three quarters, before dropping back to 10% in Q1 2026.

Operating income in Q1 2026 was $70M, up from $50M in Q1 2025, reflecting 22% year-over-year growth in operating income despite the margin contraction.

Davis attributed continued Q1 investment to platform operations, AI-powered tooling, and headcount growth, while reaffirming that full-year headcount growth will remain below revenue growth.

What Does the Valuation Model Say?

TIKR’s valuation model prices The Trade Desk stock at a target of ~$36, representing approximately 57% upside from the current price of ~$23.

The mid-case model assumes a revenue CAGR of 8.1% and a net income margin of 31% over the forecast period, with an EPS CAGR of 9%.

Q1’s 12% revenue growth sits above the mid-case CAGR assumption, which means the model does not require reacceleration to hit its target; it requires only that the current deceleration stabilizes rather than deepens.

At ~$23 against a mid-case target of ~$36 and a high-case target of ~$63, the risk/reward skews meaningfully toward the upside, but the path to $36 runs through sustained mid-to-high single-digit revenue growth and continued margin discipline, neither of which Q1 definitively proved.

The investment case is not broken by this report, but it is not strengthened either. This is a hold-the-line quarter in a year management has explicitly labeled one of disciplined reinvestment.

The real question for The Trade Desk stock is whether 12% growth is the floor of a macro-driven trough or the opening move in a structural deceleration.

Near-term, the Q1 result and Q2 guide suggest a softer first half before any macro tailwind re-emerges; long-term, the structural drivers remain intact but require execution against a larger opportunity than the current results reflect.

Near-Term Case

- Q2 guidance of at least $750M implies approximately 8% to 9% growth, the lowest quarterly growth guided in the visible history, with no guidance raise accompanying the Q1 beat

- Gross margin compressed to 74% in Q1 2026 from 77% in Q1 2025, a 3 percentage point decline year-over-year, with no management guidance on when it recovers

- CPG and auto vertical pressure, cited as ongoing in Q2 prepared remarks, continues to weigh on two of the platform’s largest spending categories

- Publicis negotiations remain unresolved and publicly acknowledged, creating agency-side uncertainty that management declined to quantify

Long-Term Case

- Q1 JBP count grew 55% year-over-year, with new JBP deal spend (excluding renewals) up 40% year-over-year, representing durable structural demand commitments that extend beyond any single quarter

- CTV and audio continue to grow as a share of channel mix, with video at a low-50s percent share and audio outgrowing every other channel in Q1, per Davis

- The TIKR model’s mid-case revenue CAGR of 8.1% is already conservative relative to Q1’s 12% growth, meaning the $36 target does not require reacceleration

- Retail data marketplace, Audience Unlimited, and agentic AI partnerships (including Stagwell and expanded OpenTTD access) represent near-term unlocks management identified as platform investment priorities for 2026

Should You Invest in The Trade Desk, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up The Trade Desk, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Trade Desk, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TTD stock on TIKR for Free →