Key Stats for Citigroup Stock

- 52-Week Range: $72 to $135

- Current Price: $126

- Street Mean Target: $144

- Street High Target: $162

- Analyst Consensus: 13 Buys / 6 Outperforms / 4 Holds / 0 Underperforms / 1 Sell

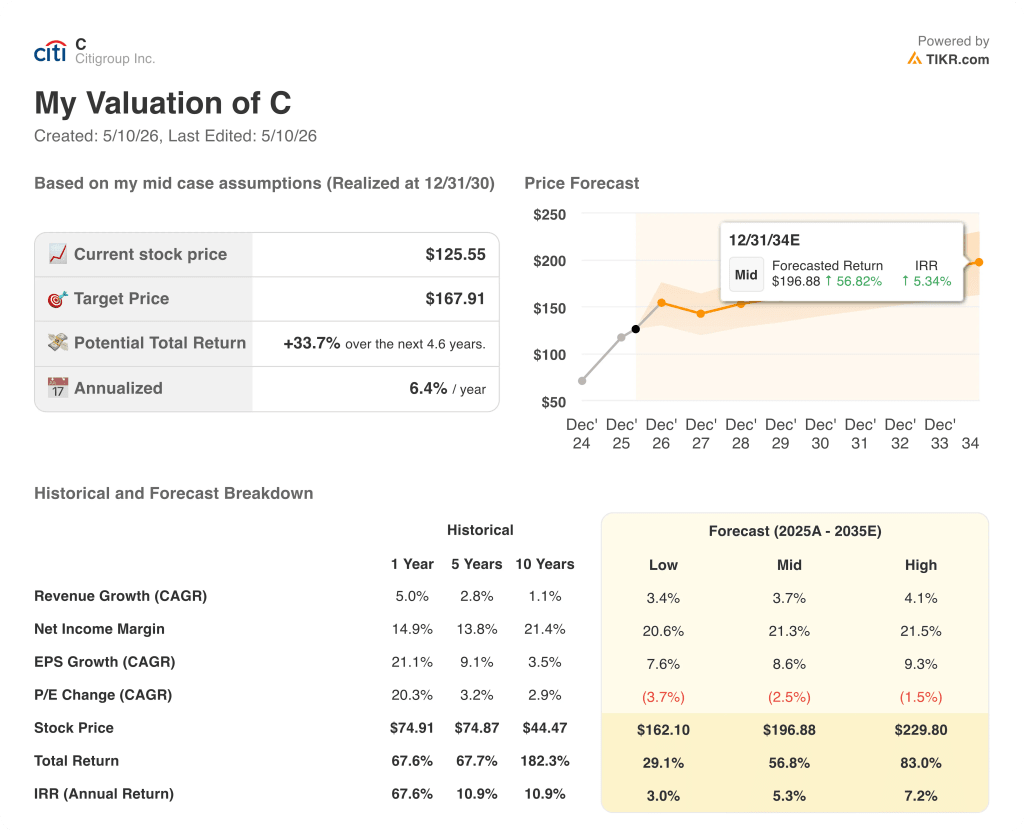

- TIKR Model Target (Dec. 2030): $168

What Happened?

Citigroup Inc. (C) is one of the largest global banks in the world, operating across five core businesses: Services, Markets, Banking, Wealth, and U.S. Consumer Cards.

The bank delivered its best quarterly revenue in a decade in Q1 2026, reporting $24.63 billion in revenues, up 14.1% year over year.

Net income came in at $5.8 billion with EPS of $3.06 and a return on tangible common equity of 13.1%, up sharply from 9% in the same quarter a year earlier.

Services, which CEO Jane Fraser calls the “crown jewel,” posted a 17% revenue increase with new client mandates up 40% and cross-border transaction volumes up 12%.

Markets crossed $7 billion in revenues for the first time in a decade, with Equities up nearly 40% year over year as prime balances surpassed $500 billion.

The bank also completed its exit from Russia in Q1, releasing approximately $4 billion in capital, which helped fund a record $6.3 billion quarterly share buyback and brought the bank within reach of completing its $20 billion repurchase program.

At its May 7 Investor Day, Citi raised its near-term return target to 11% to 13% ROTCE for 2027 and 2028, and laid out a medium-term path to 14% to 15%, driven by continued revenue growth across all five businesses, structural expense reduction, and accelerating DTA utilization.

Fraser also announced a new $30 billion share buyback program, underscoring management’s confidence that the transformation the bank has spent five years executing is now generating durable, compounding results.

The consent orders imposed by regulators in 2020 remain in place, though Fraser noted that 90% of transformation programs are now at or near their target state, with the remaining work focused on data governance for regulatory reporting.

Wall Street’s Take on C Stock

The first quarter did what Investor Day needed it to do. Citigroup stock entered the May 7 presentation with live proof that the transformation is not a promise anymore, and the revenue jump validated every near-term return target management put on the board.

Citigroup’s normalized EPS came in at $3.06 for Q1 2026, a 56% year-over-year surge, and consensus estimates see full-year 2026 normalized EPS reaching around $10 as buybacks compress the share count while operating leverage continues to build.

The EPS trajectory matters here because Citigroup stock trades on a P/E basis, and the combination of a rising earnings run rate and a $30 billion buyback authorization compresses that multiple faster than organic growth alone would.

Conviction among covering analysts has tightened meaningfully: 13 of the 22 analysts tracking Citigroup stock rate it a Buy, with 6 Outperforms alongside them, a mean price target of $144, and implied upside of around 15% from current levels. The most bullish target sits at $162, reflecting a scenario where Citi closes more of the gap with peers on return on tangible equity.

The high-end target of $162 and the low-end floor of $125 capture the central debate: Citi is producing near-peer returns now, but the market is still pricing in execution risk around consent order removal and the pace of DTA burn-down. Watch for any Fed or OCC signal on the consent orders. A formal closure would be the single fastest re-rating catalyst this stock has.

The risk is regulatory timing. If consent order removal extends into 2027 or beyond, the market will continue to apply a discount that compresses any multiple expansion from the earnings growth.

Q2 2026 earnings will confirm whether the 14% revenue growth rate in Q1 was a structural shift or partly a high-water mark from exceptional trading conditions.

What Does the Valuation Model Say?

The TIKR model targets $167.91 for Citigroup stock under a mid-case scenario that assumes around 4% annual revenue growth and net income margins expanding toward 21%, consistent with Citi’s stated targets of 11% to 13% ROTCE in 2027-2028 and the $30 billion buyback program compounding per-share earnings at a roughly 9% annual rate through 2030.

The single question this investment hinges on: Can Citi sustain double-digit EPS growth long enough for the market to close the 30-to-40 basis point gap in ROTCE that still separates it from Bank of America and Wells Fargo?

What Has to Go Right:

- Services continues growing at mid-single-digit revenue CAGR, sustaining mid-20s ROTCE through the interest rate cycle

- Equities prime balances sustain above $500 billion, pushing Markets ROTCE toward 13%+

- Banking gains further Investment Banking share, reaching the stated 6%+ IB wallet share target

- The $30 billion buyback executes through 2027-2028, compressing shares outstanding and mechanically lifting EPS

- Consent orders are lifted by year-end 2026, removing the valuation discount the market has applied since 2020

What Could Go Wrong:

- Macro deterioration (unemployment rising toward the 7% downside scenario Citi reserves against) pressures U.S. Consumer Cards, which generates 19% ROTCE and anchors North American profitability

- Middle East conflict headwinds persist, weighing on Q2 and Q3 trading conditions and slowing Investment Banking pipeline conversion

- Consent orders extend beyond 2027, keeping the structural P/E discount in place even as earnings compound

- DTA utilization runs below the guided $800 million annual pace, reducing the capital benefit that supports both buybacks and CET1 management

- Wealth builds slower than projected, as Citigold adoption and Citi Sky rollout face typical friction in a new technology deployment

Should You Invest in Citigroup Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Citigroup Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Citigroup Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze C stock on TIKR for Free →