Key Stats for Cisco Stock

- 52-Week Range: $61 to $97

- Current Price: $97

- Street Mean Target: $90

- Street High Target: $110

- Analyst Consensus: 13 Buys / 4 Outperforms / 9 Holds / 1 No Opinion

- TIKR Model Target (Jul. 2031): $103

What Happened?

Cisco Systems (CSCO) is the world’s largest enterprise networking company, building the routers, switches, optics, and security software that connect the internet and corporate data centers.

Cisco stock has surged roughly 59% from its 52-week low of $60.85, reaching near-record levels as a wave of AI infrastructure spending has transformed the investment case.

The inflection point came in Q2 FY2026, when Cisco reported revenue of $15.35 billion, up 10% year over year, and non-GAAP EPS of $1.04, both above the high end of guidance.

Product orders told the real story: total orders rose 18% year over year, including a staggering 65% jump from Service Provider and Cloud customers driven by hyperscaler demand.

The hyperscaler number that reframed everything was $2.1 billion in AI infrastructure orders taken in a single quarter, equal to the total AI orders Cisco booked across all of fiscal year 2025.

CEO Chuck Robbins framed the scale plainly on the Q2 earnings call: “We shipped our 1-millionth Silicon One chip in Q2, and plan to deploy our Silicon One architecture across our high-performance networking systems by fiscal year ’29.”

Cisco now expects to take AI orders exceeding $5 billion and recognize over $3 billion in AI revenue from hyperscalers in FY2026, a guidance raise that lifted the full-year revenue outlook to $61.2 billion to $61.7 billion.

The AI buildout is running on two parallel tracks: hyperscaler infrastructure powered by Silicon One chips and optics, and an enterprise refresh cycle as corporate customers modernize campus networks for agentic AI workloads.

At Cisco’s February AI Summit, Robbins called 2026 “the year of agentic applications,” arguing that legacy infrastructure was not designed for the performance, latency, and security demands of AI agents running across enterprise networks.

Networking product orders accelerated to over 20% growth in Q2, marking six consecutive quarters of double-digit growth, as Wi-Fi 7, new campus switches, and industrial IoT products ramped faster than any prior product cycle in Cisco’s history.

Beyond hyperscalers, Cisco disclosed a separate AI pipeline exceeding $2.5 billion for neocloud, sovereign, and enterprise customers, representing upside not included in current guidance.

Wall Street’s Take on CSCO Stock

The debate around Cisco stock has shifted entirely: this is no longer a question of whether the AI buildout benefits Cisco, but whether the stock at $96.57 has already priced in the magnitude of that benefit.

CSCO’s revenue is the right lens here. Consensus estimates project quarterly revenue accelerating through FY2026, with Q3 guided at $15.4 billion to $15.6 billion and full-year revenue at $61.2 billion to $61.7 billion, up roughly 7% year over year, as hyperscaler AI orders convert to recognized revenue at an accelerating clip.

The 22 analysts covering Cisco stock are split in a way that tells its own story: 13 Buys, 4 Outperforms, 9 Holds, and 1 No Opinion, with a mean price target of $89.54 and a high target of $110. The consensus is constructive but the mean target sits 7% below the current price, meaning the Street as a whole has not yet updated its models to reflect the AI order acceleration.

The target spread runs from $75 to $110 and reflects genuine disagreement over the pace of AI revenue recognition and gross margin recovery. The lower end assumes memory cost headwinds persist and security segment drag continues; the upper end assumes hyperscaler orders accelerate into FY2027 and enterprise campus refresh compounds the AI story through FY2028 and beyond.

The signal worth watching is CFO Mark Patterson’s gross margin commentary. Non-GAAP product gross margin fell 130 basis points in Q2 due to memory cost inflation and hardware mix shift, and Q3 guidance implies further pressure, but Patterson was explicit that advanced purchase commitments for memory are up $1.8 billion in 90 days and price increases are now in effect with partners and customers.

The risk is straightforward: if the handful of hyperscaler customers placing nonlinear, lumpy AI infrastructure orders slow their pace of orders in any single quarter, Cisco’s headline growth numbers compress sharply with little cushion from the Security segment, which remains in a Splunk-driven transition headwind.

The catalyst is the Q3 FY2026 earnings call on May 13, where the number to watch is total AI orders taken: anything meaningfully above the $2.1 billion Q2 pace confirms the acceleration thesis is intact.

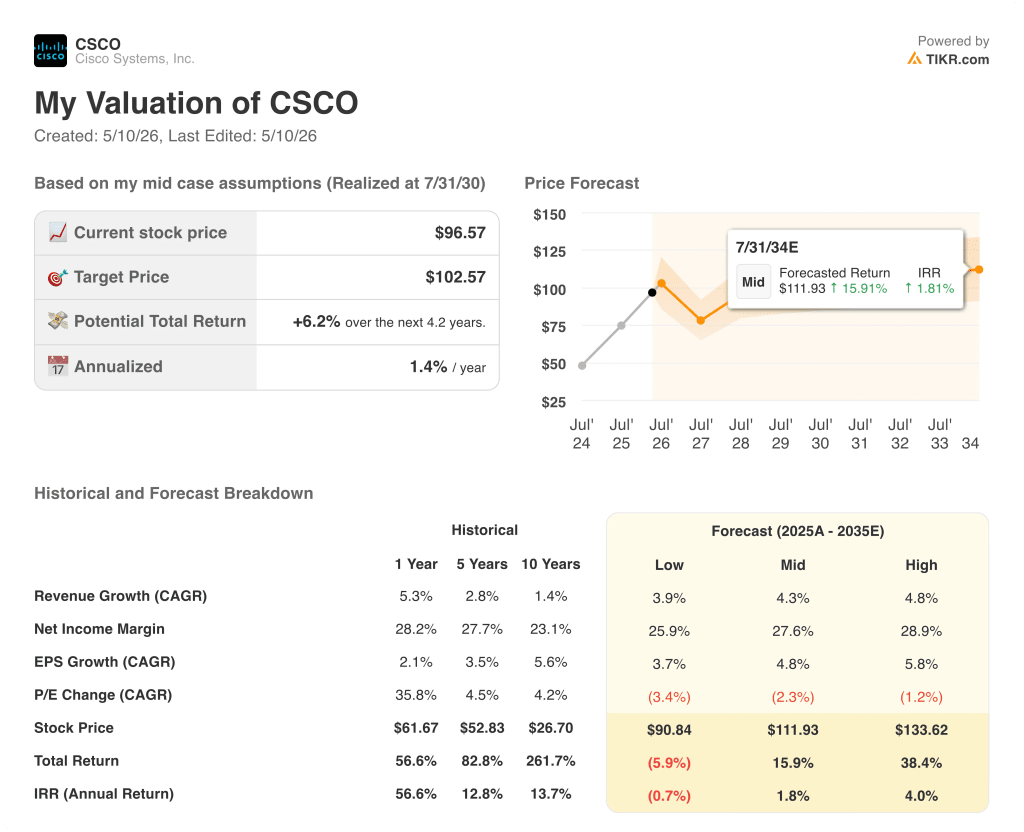

What Does the Valuation Model Say?

The TIKR model prices Cisco stock at $102.57, assuming a mid-case revenue CAGR of around 4% through FY2030 and net income margins holding near 28%, a conservative set of inputs that does not fully reflect the AI order inflection or the upside from campus refresh compounding over a multi-year cycle.

At $97 against that $103 model target, with a mid-case total return of around 16% by 2034 but an annualized IRR of just 1.8%, Cisco stock is fairly valued at current levels: the near-term AI story is real, but the stock’s 59% run from its lows has already absorbed much of it, leaving the long-term return dependent on whether AI order volumes hold or accelerate into FY2027 and beyond.

The AI order pace is either the beginning of a multi-year compounding cycle or a front-loaded surge that moderates, and the answer to that question determines whether Cisco stock earns a premium to its current price or revisits the mean analyst target of $90.

What Has to Go Right

- Hyperscaler AI orders exceed $5 billion in FY2026 and continue to scale in FY2027, with Silicon One gaining share across both scale-out and scale-across architectures

- Campus enterprise refresh continues to ramp faster than prior product cycles across all four platforms (campus switching, routing, wireless, industrial IoT), supporting double-digit networking order growth through FY2027

- Gross margin headwinds from memory costs are offset by price increases and contractual Ts and Cs revisions over the next two to three quarters, stabilizing product gross margin above 66%

- Splunk cloud transition completes its revenue recognition drag by mid-FY2027, with organic security revenue approaching double-digit growth as Secure Access, XDR, Hypershield, and AI Defense reach scale across 4,000-plus enterprise customers

What Could Go Wrong

- Hyperscaler AI orders are nonlinear and lumpy; any single-quarter pause by the fewer than five major customers placing orders compresses both reported growth and forward guidance visibility significantly

- Memory cost inflation persists longer than management expects, keeping product gross margin below the 66% to 67% range that supports the historical operating margin profile

- Security segment recovery takes longer than guided: the Q4 FY2026 exit rate approaching double-digit organic growth depends on Splunk transition headwinds clearing and new product ramp continuing at current pace

- At 59% off the lows, the stock is trading within dollars of its 52-week high and above the consensus mean target of $89.54; any guidance miss or order deceleration at the May 13 earnings call would remove the momentum premium quickly

Should You Invest in Cisco Systems, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Cisco Systems stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Cisco Systems alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CSCO stock on TIKR for Free →