Key Stats for AbbVie Stock

- 52-Week Range: $177 to $245

- Current Price: $202

- Street Mean Target: $252

- Street High Target: $328

- Analyst Consensus: 16 Buys / 8 Outperforms / 8 Holds / 1 No Opinion

- TIKR Model Target (Dec. 2030): $311

What Happened?

AbbVie Inc. (ABBV) is a global biopharmaceutical company best known for Humira, the world’s former best-selling drug, which lost U.S. patent exclusivity in 2023 and has faced a wave of cheaper biosimilar competition ever since.

The company’s post-Humira transition is no longer a question mark.

AbbVie reported Q1 net revenues of $15 billion, up 12.4% year over year, beating analyst estimates of $14.72 billion by around $280 million.

The beat was driven by Skyrizi and Rinvoq, the two immunology drugs AbbVie has spent the last three years positioning as Humira’s successors in psoriasis, inflammatory bowel disease, and rheumatoid arthritis.

Skyrizi (risankizumab), which targets the IL-23 pathway to control inflammation, posted Q1 sales of $4.48 billion, growing 30.9% year over year and beating Wall Street estimates of $4.41 billion.

Rinvoq (upadacitinib), a JAK inhibitor approved across rheumatoid arthritis, ulcerative colitis, Crohn’s disease, and atopic dermatitis, generated $2.12 billion in Q1 sales, up 23.3% and ahead of the $2.04 billion consensus.

Humira’s global revenue fell 38.6% to $688 million, slightly below expectations, but the decline is fully expected and already priced into AbbVie’s guidance.

AbbVie’s neuroscience portfolio delivered a surprise, with total revenues of $2.88 billion up 26% year over year, fueled by migraine drugs Ubrelvy and Qulipta alongside Vraylar in psychiatry, with Global Botox Therapeutic crossing the $1 billion quarterly milestone for the first time.

On an adjusted basis, AbbVie earned $2.65 per share for Q1, beating the $2.59 consensus, and the company raised its full-year 2026 adjusted EPS guidance to a range of $14.08 to $14.28 from $13.96 to $14.16, with CEO Robert Michael noting AbbVie is “well positioned to deliver top-tier growth for the long term.”

In parallel, AbbVie submitted a new FDA application for Rinvoq in severe alopecia areata and filed for Skyrizi subcutaneous induction in Crohn’s disease, with an approval decision on the latter expected later in 2026.

AbbVie also announced a $1.4 billion investment to build a 185-acre pharmaceutical manufacturing campus in Durham, North Carolina, expected to be completed by end of 2028, part of a broader $100 billion commitment to U.S. R&D and capital investments over the next decade.

Wall Street’s Take on ABBV Stock

The Q1 beat closes the gap between what skeptics thought possible and what AbbVie’s commercial machine is actually delivering, and it directly strengthens the trajectory of AbbVie’s adjusted EPS heading into the second half of the year.

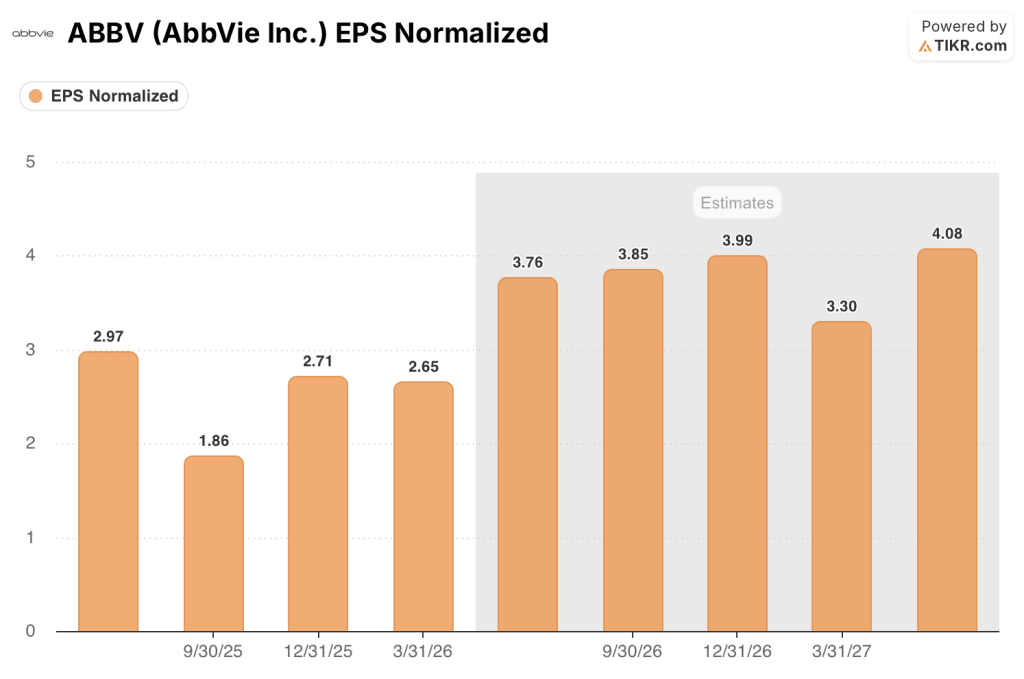

AbbVie’s adjusted normalized EPS of $2.65 in Q1 grew 7.7% year over year, with consensus now projecting around $3.76 for Q2, $3.85 for Q3, and $3.99 for Q4, each representing year-over-year growth accelerating through the back half as the Q3 2025 comparison base was particularly weak at $1.86.

Thirty analysts currently cover ABBV stock, with 16 Buy ratings, 8 Outperforms, 8 Holds, and 1 No Opinion, carrying a mean price target of $252 and a high target of $328, implying around 22% upside from current levels at a median target of $254.

The spread between the $184 low target and $328 high target reflects a genuine debate: bears are anchored to J&J’s Icotyde launch risk and the pace of Humira’s decline, while bulls are pricing in the sustained outperformance of Skyrizi and Rinvoq well past consensus models, with management explicitly stating it sees upside to the sell-side’s $33 billion Skyrizi peak estimate for 2031.

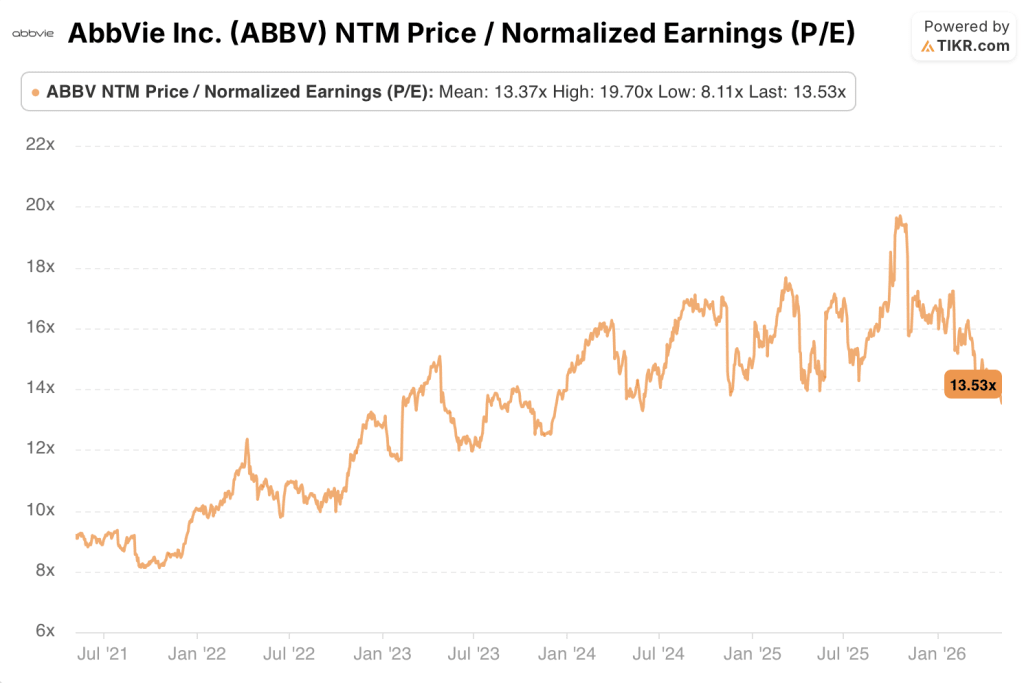

At 13.53x NTM normalized earnings, right in line with its five-year historical mean of 13.37x, AbbVie stock appears fairly valued on a multiple basis, though the NTM P/E reached as high as 19.70x during the period, and any re-rating toward that range as pipeline assets mature would represent substantial upside from today’s price.

The risk is competitive erosion in psoriasis from Icotyde faster than management expects, specifically in the oral-preferring patient segment that Skyrizi’s quarterly injectable dosing does not naturally capture.

The next catalyst is the Q2 2026 earnings report, where investors will watch whether Skyrizi maintains its greater than 30% year-over-year growth trajectory and whether the Rinvoq alopecia areata FDA filing in the U.S. advances toward a decision timeline.

What Does the Valuation Model Say?

TIKR’s valuation model prices AbbVie stock at $311 under mid-case assumptions, using a revenue CAGR of around 4% through 2035 and net income margins expanding to around 42%, implying roughly 54% total return potential over the next 4.6 years at an annualized rate of around 10%.

At 13.53x NTM normalized earnings against a five-year historical mean of 13.37x, AbbVie stock appears fairly valuedon a pure multiple basis, though the pipeline optionality in neuroscience and oncology that the sell-side has not fully priced in creates meaningful asymmetric upside from here.

The central tension: whether Skyrizi can hold dominant share in immunology as oral IL-23 competition enters psoriasis, or whether the class expands enough to absorb new entrants without cannibalization.

Bull Case

- Skyrizi Q1 sales of $4.48 billion grew 30.9% despite J&J’s Icotyde launch; management raised full-year Skyrizi guidance to $21.6 billion, reflecting confidence the IL-23 market expands rather than fragments

- Rinvoq FDA filings for alopecia areata and the Skyrizi subcutaneous Crohn’s application, if approved in 2026 and early 2027 respectively, add two new prescription drivers to the combined $31 billion Skyrizi/Rinvoq 2027 target

- Neuroscience revenues of $2.88 billion grew 26% in Q1 with Botox Therapeutic crossing $1 billion for the first time; the Parkinson’s franchise with Vyalev and tavapadon (approval expected Q3 2026) is tracking above $5 billion peak

- TIKR model mid-case target of $311 implies around 54% total return; at the high-case revenue and margin assumptions, the price target reaches $449

Bear Case

- Icotyde’s once-daily oral convenience could appeal to a meaningful subset of psoriasis patients who resist injectables; J&J estimates $5 billion-plus in Icotyde peak sales, with IBD indications in development

- Humira revenues of $688 million in Q1 declined 38.6%; the long tail of Humira erosion continues and immunology execution must remain flawless to offset it every quarter

- The FDA issued a Complete Response Letter for trenibotE on manufacturing concerns, delaying the aesthetics revenue catalyst into 2027 and removing near-term upside in a portfolio segment that posted negative filler growth in Q1

- The TIKR model low-case revenue CAGR of 3.8% and a P/E contraction of 3.4% annually produces a stock price of around $308 by 2030, still above current levels but with meaningfully compressed IRR

Should You Invest in AbbVie Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AbbVie Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AbbVie Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ABBV stock on TIKR for Free →