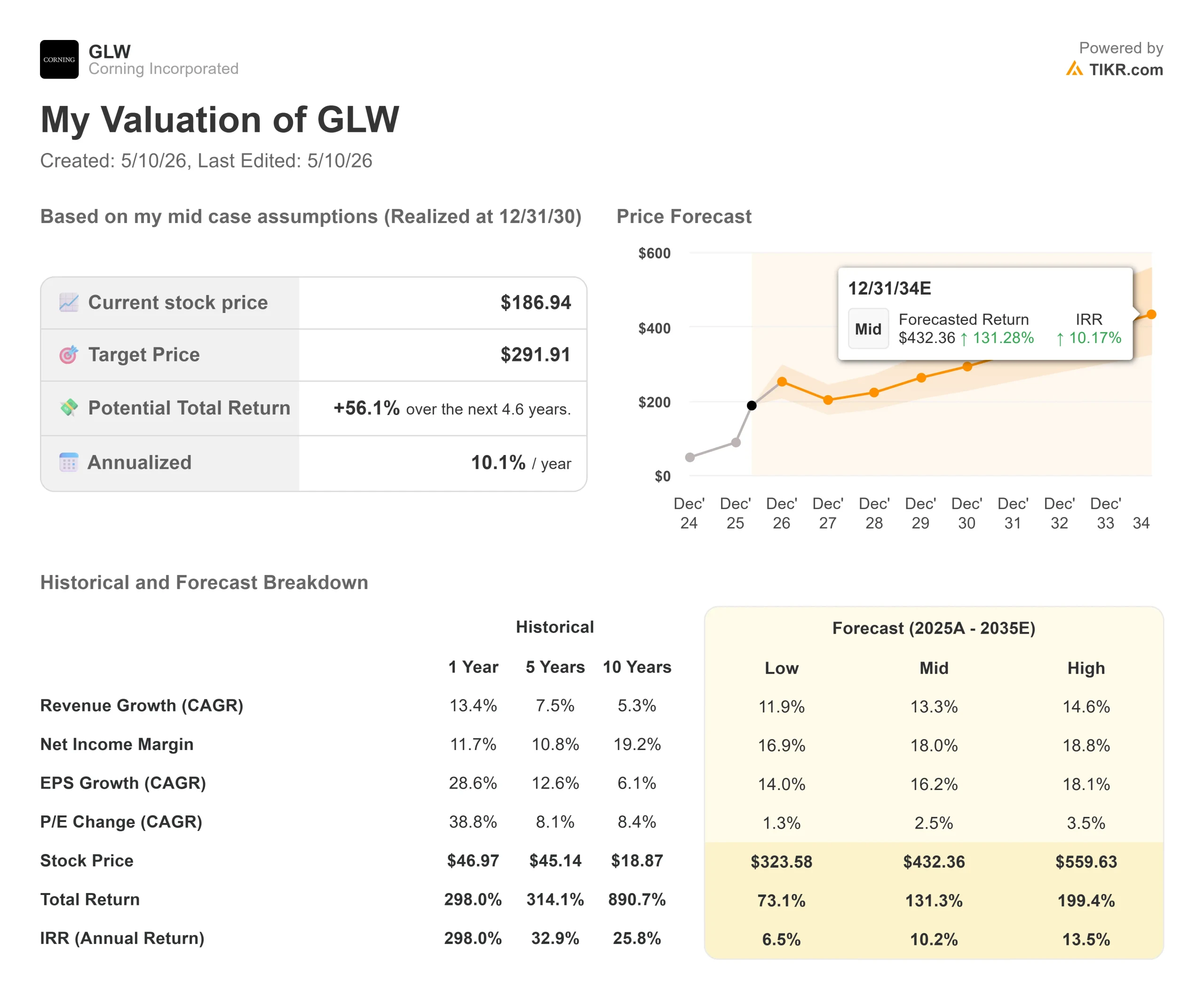

Key Stats for Corning Stock

- Current Price: $186.94

- Target Price (Mid): ~$292

- Street Target (Mean): ~$173 (15 analysts)

- Potential Total Return: ~56%

- Annualized IRR: ~10% / year

- Earnings Reaction: -0.75% (April 28, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Corning (GLW) is up more than 300% in 12 months, and the market is now asking a harder question than usual: not whether Corning is a good business, but whether it is already priced for perfection. On May 6, the stock surged roughly 12% after NVIDIA named Corning its optical connectivity partner for next-generation AI infrastructure and put $500 million behind it. Bulls say this validates everything Corning has been building toward. Bears point to a 55x forward P/E and a stock near its 52-week high of $198.25, asking whether the AI thesis is already priced in. The unresolved question: can Corning hit $40 billion in revenue by 2030, and does it matter at today’s price if it does?

The context matters. In Q4 2023, Corning launched its Springboard plan, committing to grow from a $13 billion annualized sales run rate to $18 billion by the end of 2026, with operating margin expanding from 16% to 20%. By this week’s investor event at the New York Stock Exchange, the company had hit that margin target a full year early, grown EPS 85%, expanded return on invested capital by 540 basis points to 14.2%, and nearly doubled free cash flow to $1.72 billion in 2025 from $880 million in 2023. CEO Wendell Weeks said at the event: “We’ve outperformed our plan, and we have transformed the financial profile of the company.” That track record is the foundation on which the new, far more ambitious plan rests.

The NVIDIA Deal Is Not a Marketing Announcement

The partnership goes well beyond a typical supply agreement. Per Corning’s investor relations materials, NVIDIA purchased pre-funded warrants to acquire 3 million Corning shares for $500 million upfront. NVIDIA also received warrants to buy up to 15 million additional shares at $180 per share. If fully exercised, the total investment could reach approximately $3.2 billion.

In exchange, Corning will build three new manufacturing facilities in North Carolina and Texas, increase U.S. optical connectivity capacity by 10 times, and expand U.S. fiber production capacity by more than 50%, while creating more than 3,000 jobs. Weeks explained the logic at the event: “This partnership creates a significant opportunity for growth, for new innovations and for new advanced manufacturing platforms, including many right here in the U.S.” The deal underpins Corning’s new Photonics Market-Access Platform (MAP), a business unit targeting the opportunity to bring optics inside the AI switch box, an area where Corning currently has no revenue.

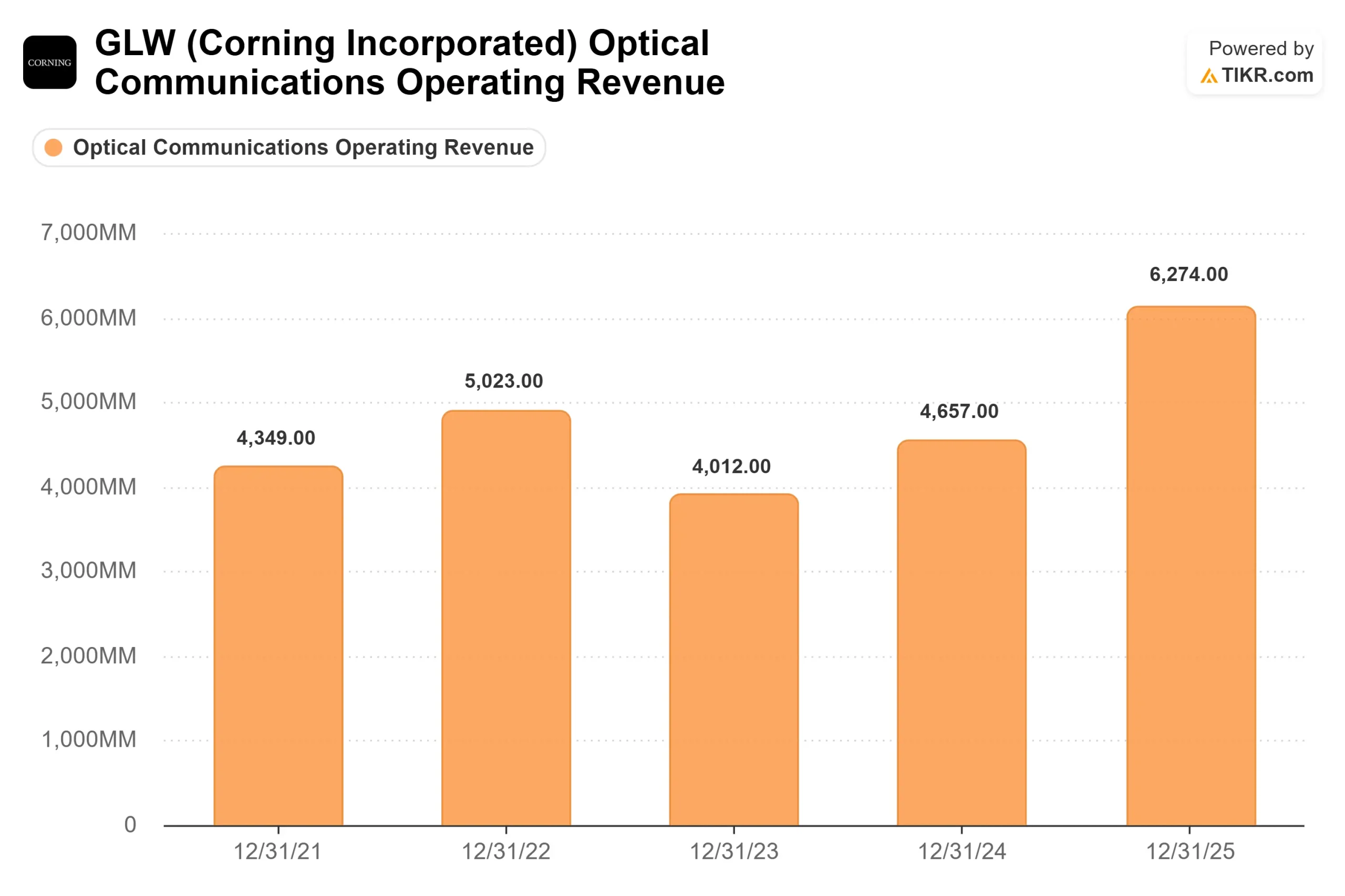

The NVIDIA deal landed on a strong foundation. In Q1 2026, Corning reported core sales of $4.35 billion, up 18% year over year, with core EPS of $0.70, up 30%. Optical Communications grew 36%, and Solar grew 80%. Management also disclosed that two additional hyperscale customers had signed long-term agreements comparable in size to the previously announced up-to-$6 billion Meta deal. When Q1 earnings landed on April 28, the stock fell 0.75% because Q2 guidance of approximately $4.6 billion came in slightly below analyst expectations, partly due to a planned $30 million solar maintenance shutdown. That dip looks different in hindsight.

See historical and forward estimates for Corning stock (It’s free!) >>>

Why the Physics of AI Favor Corning

The most differentiated part of the investor event had nothing to do with guidance. It was a technical explanation of why optical fiber demand inside AI data centers is set to grow faster than the GPU count itself.

Senior VP and General Manager of Optical Communications Mike O’Day walked through the mechanics. Today’s AI data centers run GPU clusters on scale-out networks with two optical switching layers, which can support up to 130,000 GPUs. Once clusters exceed that threshold, a third layer must be added. As O’Day put it: “When this third layer is needed, it means more Corning, increasing our content by 50% as we go from 2 layers to 3.” Hyperscaler clusters are rapidly approaching that threshold.

The second driver is scale-up, the high-bandwidth, low-latency network connecting GPUs within a single computing node. Today, that network is entirely copper. But copper hits physical limits as node sizes grow. CEO Weeks described the transition as inevitable beyond the “electrical to optical divide,” adding an entirely new optical network where Corning currently earns nothing.

Combined, Corning expects optical content demand per GPU in its Enterprise MAP to grow 1.3 to 1.5 times faster than GPU unit growth through 2028. Most AI infrastructure suppliers can only gesture at AI tailwinds. Corning can quantify theirs.

The third driver is co-packaged optics (CPO), the basis for the Photonics MAP. In a traditional switch, optical transceivers sit outside the box, connecting to Corning’s fiber today. In CPO architectures, that functionality moves inside onto a silicon photonic engine, opening an entirely new addressable market for passive photonic components where Corning currently has zero content. O’Day said directly: “Everything you see in yellow is potential Corning content where none existed inside the box before.” Management estimates this Photonics MAP could represent a $10 billion revenue stream by 2030.

The Springboard Numbers and What Has to Go Right

The upgraded plan runs on two tracks. Corning’s internal plan targets a $30 billion annualized run rate by the end of 2028 and $40 billion by the end of 2030. The high-confidence plan, designed as an investable thesis for outside investors, targets $27 billion by 2028 and $35 billion by 2030. The implied compound annual growth rate from the end of 2026 through 2030 is 19% under the internal plan, a 400 basis point acceleration from the 15% CAGR delivered in Springboard’s first two years.

CFO Ed Schlesinger explained what separates the two tracks: “One of the most significant areas we’re adjusting for is the timing on scale-up of the network. This impacts both enterprise and photonics. The timing of when scale-up happens could have a significant impact to our numbers.” The difference between $35 billion and $40 billion is a timing question about optical scale-up adoption, not whether it happens.

What gives Corning unusual protection is its customer structure. The large, long-term agreements with Meta, NVIDIA, and two additional hyperscalers include upfront capital contributions or revenue guarantees. Schlesinger compared the model to Corning’s Gen 10.5 display glass agreements and Apple’s $2.5 billion commitment to manufacture iPhone and Apple Watch cover glass at Corning’s Kentucky facility. These structures let Corning invest ahead of revenue without bearing the full demand risk.

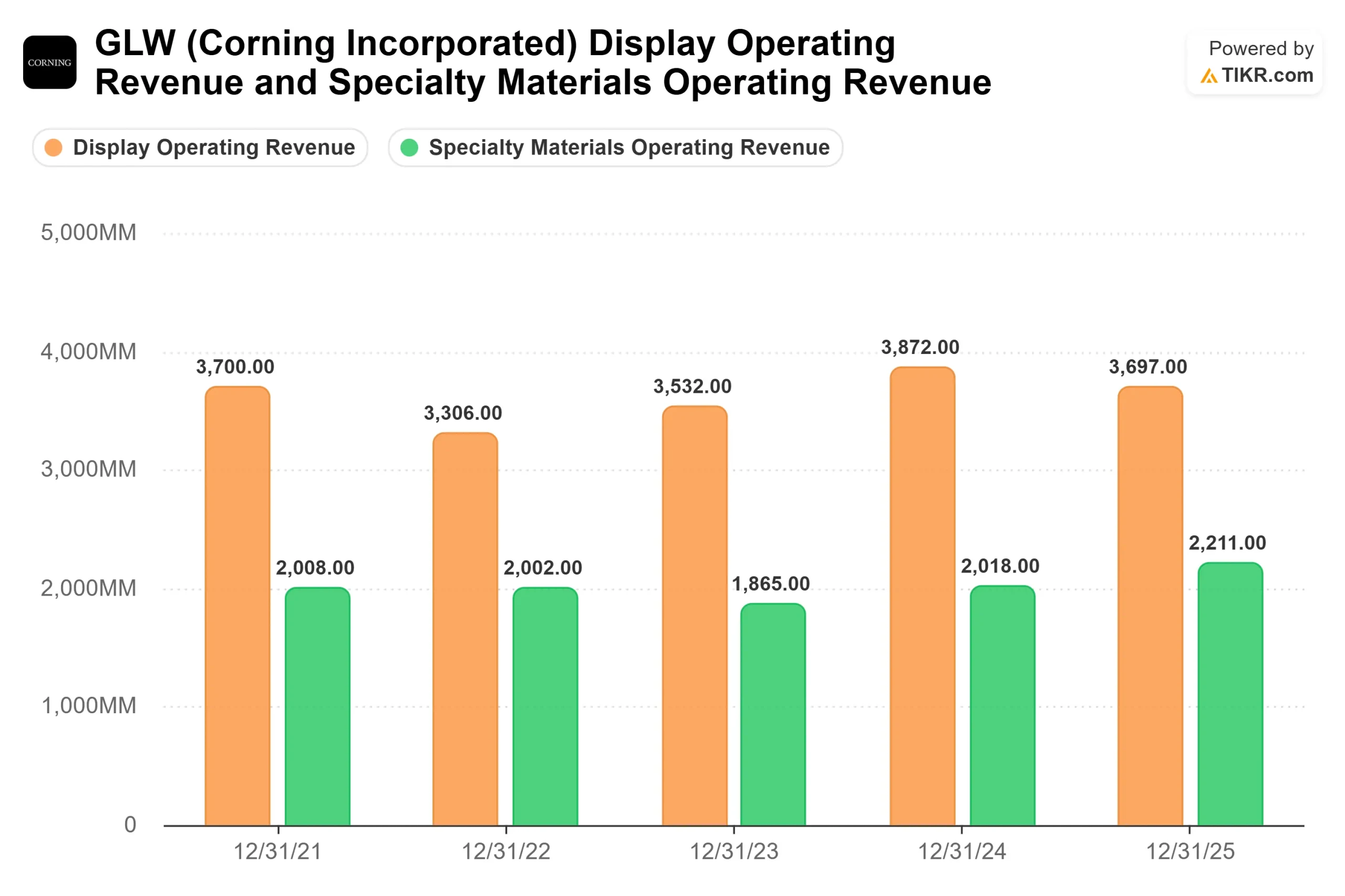

Execution risk remains real. Solar posted $370 million in Q1 revenue, up 80%, but segment net income fell to just $7 million as wafer ramp costs hit margins. Management expects recovery as production scales, with polysilicon already running above the 20% operating margin target. But until wafer profitability improves, Solar will keep dragging on consolidated margins.

On valuation multiples, Corning trades at roughly 30x NTM EV/EBITDA, about 55% above the peer median of around 19x on the TIKR Competitors page. The closest optical communications comparable is Coherent Corp. (COHR), which trades at roughly 30x NTM EV/EBITDA, in line with Corning. But Coherent trades at about 7.6x NTM revenue versus Corning’s 8.6x, a premium that reflects Corning’s vertical integration across fiber, cable, and connectivity, plus the strategic weight of the NVIDIA relationship. Whether that premium holds depends on whether the Photonics MAP generates real revenue and whether optical scale-up adoption runs on management’s timeline.

See how Corning performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $186.94

- Target Price (Mid): ~$292

- Potential Total Return: ~56%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Corning stock (It’s free!) >>>

The TIKR mid-case model uses a revenue CAGR of around 13% with net income margins expanding toward around 18% by 12/31/30. The primary revenue drivers are Optical Communications, which grew 36% year over year in Q1 2026 with segment net income up 93%, and Solar, where near-term ramp costs weigh on margins but underlying demand is strengthening. The margin driver is operating leverage: Corning’s capacity investments were largely in place before the AI revenue wave, so incremental Optical revenue flows through at high profit margins. The primary risk is timing: if optical scale-up networks remain copper through 2028, the Photonics MAP stays an option rather than a revenue stream.

The TIKR model’s high case assumes faster scale-up adoption and earlier Photonics MAP contribution. The low case assumes Solar execution friction, a delayed scale-up ramp, and some multiple compression after the stock’s 300%-plus run. At around $187, investors are paying for the high-confidence plan and getting the $40 billion internal plan as optionality. That is not cheap. But for a company that has beaten every prior version of its own plan and just secured a $500 million equity commitment from the most important chip company in AI, the premium is not without logic.

Conclusion

The metric to watch at Q2 2026 earnings, expected in late July, is Optical Communications revenue growth. If the segment sustains 30%-plus year-over-year growth despite the stock’s sharp re-rating, it confirms that demand is outpacing even the elevated expectations now embedded in the price. Corning has transformed from a cyclical glass maker into a structural pillar of AI optical infrastructure. The NVIDIA partnership makes that thesis harder to dismiss.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Corning?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Corning, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Corning alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Corning on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!