Key Stats for KLA Corporation Stock

- 52-Week Range: $740 to $1,939

- Current Price: $1,819

- Street Mean Target: $1,836

- Street High Target: $2,100

- Analyst Consensus: 14 Buys / 5 Outperforms / 10 Holds / 1 Underperform

- TIKR Model Target (Dec. 2030): $

What Happened?

KLA Corporation (KLAC) builds the process control systems that semiconductor manufacturers use to find microscopic defects and optimize yields during chipmaking, and KLAC stock has become one of the defining beneficiaries of the AI infrastructure buildout.

Fiscal third-quarter revenue landed at $3.415 billion, beating the Street’s $3.378 billion estimate and up 11.5% year over year.

Adjusted EPS came in at $9.40, topping the $9.17 consensus estimate and marking the fifth consecutive quarter of beats.

The result was driven by rising investment in leading-edge foundry and logic capacity and a step-change in demand for high-bandwidth memory, the specialized chip used to feed AI processors data at scale.

KLA’s advanced packaging revenue is on track to reach approximately $1 billion in 2026, up from approximately $635 million in 2025, a figure CEO Rick Wallace called “well above our prior estimates” on the April 29 earnings call.

Process control intensity, which measures how much of the total semiconductor equipment market goes to inspection and metrology tools, has climbed from around 5.3% of wafer equipment spending in 2019 to 7.4% today, with KLA’s internal model targeting 9% by 2030.

The company announced a 10-for-1 stock split in May, with shares set to trade on a split-adjusted basis at market open June 12 for holders of record as of June 4.

At the March Investor Day, management raised its long-term revenue CAGR target to 13% to 17% through 2030 and set a $26 billion revenue goal, projecting $84 in EPS and authorizing an incremental $7 billion in share repurchases alongside a 21% dividend increase to $2.30 per quarter.

The post-earnings reaction was muted, with KLAC stock falling as much as 9% in after-hours trade before recovering, as analysts noted that fiscal Q4 guidance for revenue of $3.575 billion came in only marginally above consensus, a disappointment for a stock priced for outperformance.

UBS analyst Timothy Arcuri wrote that the Q4 guide reflected KLA “struggling to keep up mostly because so much of the growth this year and next is coming from memory where its exposure, while improving, is structurally much lower than peers.”

Still, at least 12 brokerages raised their price targets after the report, with the median moving to $1,825 from $1,700.

The Commerce Department’s “is-informed” letter ordering KLA and peers to halt certain tool shipments to Hua Hong, China’s second-largest chipmaker, added headline risk in late April, though CFO Bren Higgins said on the Q3 2026 earnings call that the impact was “fairly immaterial and contemplated in the guidance we provided.”

Wall Street’s Take on KLAC Stock

KLA stock’s Q3 beat came against the backdrop of rising process control intensity across every semiconductor segment, and the forward EPS trajectory now tells a story the post-earnings selloff may have obscured.

KLAC’s normalized EPS came in at $9.40 for the March quarter, up 11.8% year over year, and consensus estimates have the company accelerating sharply from here: around $10 for June, around $11 for September, and around $13 for the December quarter, reflecting a roughly 43% year-over-year gain in the back half of 2026 as new fab capacity comes online.

Of 30 analysts covering KLA Corporation stock, 14 carry Buys, 5 carry Outperforms, 10 hold a neutral rating, and 1 rates it Underperform, with the mean price target at $1,836 and the high target at $2,100; the Street is waiting for the second-half EPS ramp to confirm that supply chain constraints ease and customer urgency translates into incremental revenue recognition.

The target spread from $1,400 to $2,100 maps directly to the debate over how quickly KLA can scale shipments to match the greenfield construction wave its customers have already committed to, and whether memory’s growing contribution to process control intensity structurally closes the gap that Arcuri flagged.

The most credible bear case rests on gross margin: DRAM chip cost inflation, which Higgins quantified as a roughly 100-basis-point headwind to gross margins through at least calendar 2026, limits the earnings leverage on revenue upside, and any tariff escalation beyond the current modeled range adds further pressure.

The next confirmation point is fiscal Q4 earnings, due in late July, where the Street will be watching whether revenue lands above the $3.575 billion midpoint, whether EBIT margins recover from 42.6%, and whether management formally raises full-year 2026 guidance above the current high-teens framing.

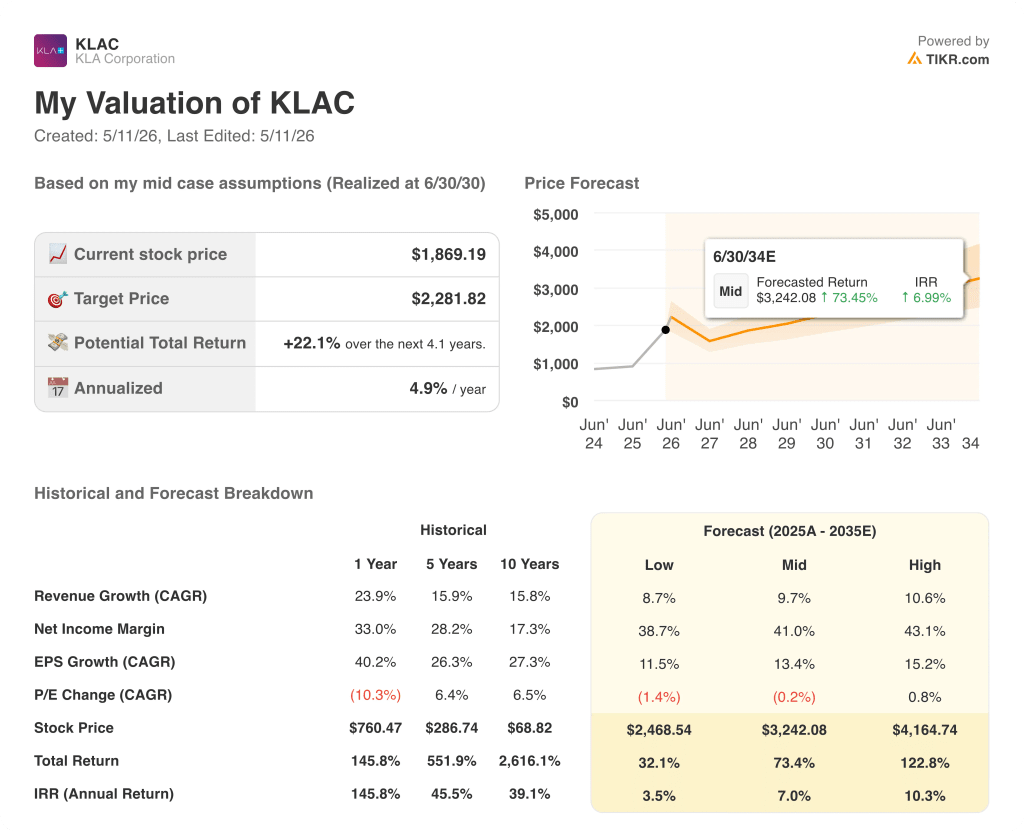

What Does the Valuation Model Say?

The TIKR model sets a mid-case target of $2,282 for KLA Corporation stock, built on a revenue CAGR of around 10% from 2025 through 2035 and a net income margin expanding toward 41%, both assumptions that sit comfortably inside the guidance management provided at the March Investor Day for a business it has a demonstrated history of delivering against.

With $26 billion in revenue and $84 in EPS as the company’s own 2030 targets, the TIKR mid-case implies a roughly 22% total return over the next four years: fairly valued at current prices for investors willing to hold through the capex supercycle, but not the compressed entry point the 52-week low represented.

The central tension in the KLA Corporation investment case is whether the second half of 2026 delivers the sequential revenue acceleration management has telegraphed, or whether supply chain constraints and a flattish China spending environment cap the near-term upside.

Bull Case (toward $2,100 to $4,165 TIKR high)

- Advanced packaging revenue reaches $1 billion in 2026, on track from $635 million in 2025, driven by CoWoS and emerging hybrid bonding demand at top hyperscaler customers

- Process control intensity reaches 9% of wafer equipment by 2030, up from 7.4% today, adding $3.1 billion in outperformance above baseline WFE growth

- Systems business grows above 20% in 2026 as greenfield fab construction commitments convert to tool deliveries in H2; Bren Higgins confirmed on the April 29 call that the second half revenue ramp is “well above 15%”

- Service revenue of approximately $3 billion in 2025 grows at the raised 13% to 15% CAGR target, nearly doubling to around $6 billion by 2030 with contract penetration above 80%

- Stock split on June 12 broadens retail participation and improves index inclusion dynamics

Bear Case (toward $1,400 TIKR low)

- Memory exposure “structurally much lower than peers” (Arcuri, UBS) limits KLA’s ability to participate proportionally if DRAM and HBM capex outpaces logic in 2027, a scenario Higgins himself acknowledged at the Investor Day

- Gross margin headwind from elevated DRAM chip costs persists at 100 basis points through end of 2026, limiting EPS leverage even if revenue accelerates

- Commerce Department “is-informed” letters targeting Hua Hong create a template for broader China restrictions; KLA’s China revenue, while “more or less flat” in absolute terms per management, represents a meaningful cushion that could shrink

- At 39x NTM earnings, any guidance miss in July carries a disproportionate de-rating risk given how much future growth the current multiple already prices

Should You Invest in KLA Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up KLA Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track KLA Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze KLAC stock on TIKR for Free →