Key Stats for Wells Fargo Stock

- 52-Week Range: $72 to $98

- Current Price: $76

- Street Mean Target: $96

- Street High Target: $113

- Analyst Consensus: 19 Buys / 7 Holds / 0 Sells

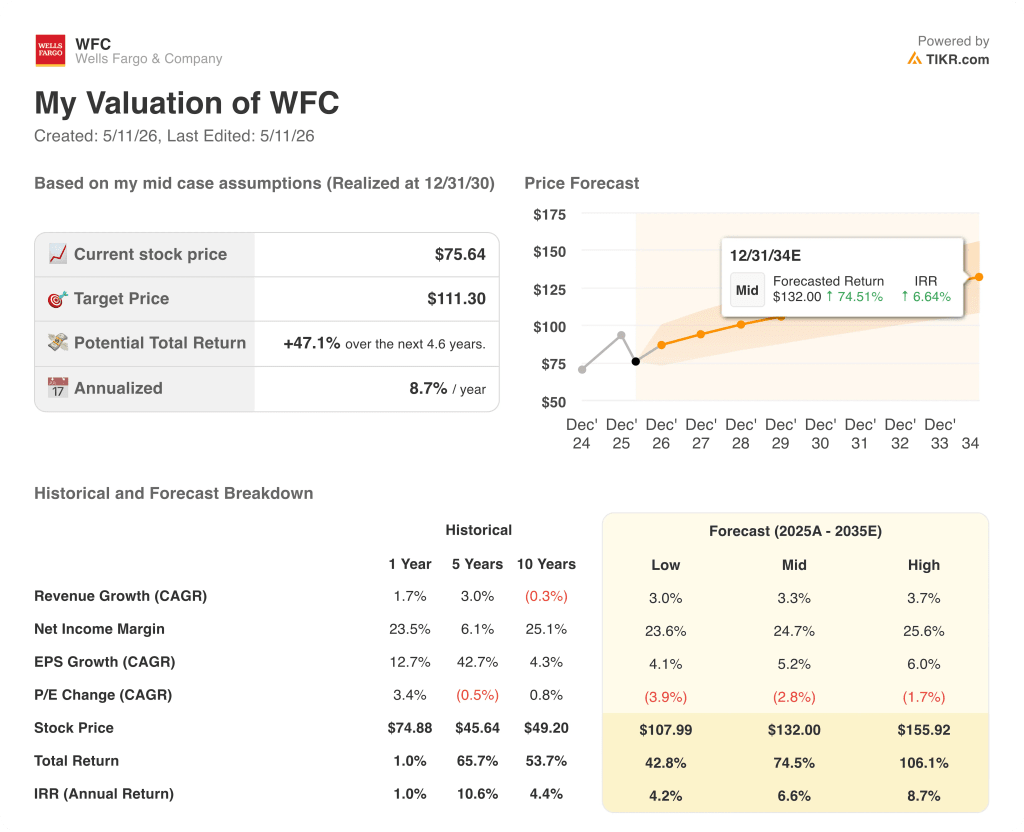

- TIKR Model Target (Dec. 2030): $111

What Happened?

Wells Fargo & Company (WFC), the fourth-largest U.S. bank by assets and one of the most consumer-exposed lenders in the country, is executing the most consequential strategic expansion in over a decade after years of regulatory constraint.

The bank’s seven-year asset cap, a penalty imposed by the Federal Reserve following a widespread fake accounts scandal that saw employees open millions of unauthorized customer accounts, was lifted in 2025, unlocking Wells Fargo’s ability to grow its balance sheet across every business line for the first time since 2018.

In March 2026, the Fed terminated its 2018 consent order, the final outstanding enforcement action from the scandal era, closing a chapter that had cost the bank billions in remediation costs and management bandwidth across 14 total consent orders terminated since 2019.

With the regulatory overhang cleared, Wells Fargo stock entered Q1 2026 as a genuine growth story for the first time in years, and the numbers confirmed the narrative: revenue rose 6% year over year to $21.45 billion, net income climbed 7% to $5.25 billion, and diluted EPS GAAP came in at $1.60, a penny above the Street’s $1.58 estimate.

The loan book crossed $1 trillion in period-end balances for the first time since Q1 2020, driven by 16.4% growth in commercial loans and 3.7% growth in consumer loans, as the post-cap balance sheet expansion moved from aspiration to realized momentum.

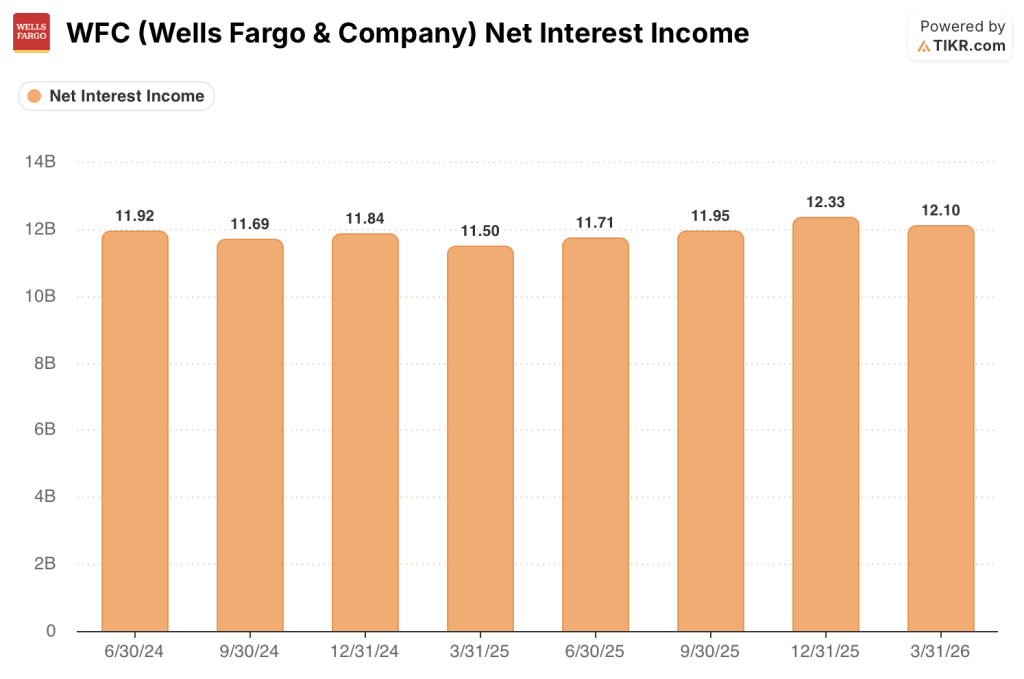

Net interest income came in at $12.1 billion against the Street’s $12.3 billion estimate, a miss that sent WFC stock down roughly 5% on earnings day and dominated the post-print narrative.

Markets revenue surged 19% year over year in Q1, driven by higher activity across most asset classes, as Wells Fargo continued building out the Corporate and Investment Bank that CEO Charlie Scharf has identified as a core long-term return driver.

Investment banking revenue grew 13% year over year, with the bank continuing to hire senior talent across M&A advisory, equity capital markets, and debt capital markets, with management entering Q2 describing the pipeline as strong and driven by M&A and equity issuance activity.

Wealth and Investment Management revenue rose 14% year over year to reach client assets of $2.2 trillion, with company-wide net asset flows reaching their highest level in over 10 years in Q1, as the bank’s Wells Fargo Premier offering gained traction across its branch network.

Auto originations more than doubled year over year, benefiting from the bank’s preferred financing partnership with Volkswagen and Audi vehicles in the United States, while new credit card account growth jumped nearly 60% year over year as earlier card product relaunches compounded into the origination pipeline.

CFO Mike Santomassimo stated on the Q1 2026 earnings call that “if demand remains strong, average loan growth could be higher than mid-single digits,” framing the bank’s official guidance as conservative relative to the momentum already visible across commercial and consumer portfolios.

The Fed’s proposed Basel III capital rule revisions, unveiled in March, would reduce Wells Fargo’s risk-weighted assets by approximately 7% under the current proposal, with the GSIB surcharge expected to remain around 1.5%, creating a pathway to release excess capital for buybacks and further balance sheet deployment.

Headcount fell for the 23rd consecutive quarter, reaching 200,999 employees at the end of March, as Scharf continued to drive efficiency across operations while simultaneously reinvesting savings into technology, advertising, and frontline growth hires across commercial banking and the investment bank.

Wall Street’s Take on WFC Stock

The Q1 miss on net interest income obscures the real story: Wells Fargo stock is in the early innings of a multi-year earnings ramp, and the bank’s idiosyncratic growth drivers are only beginning to show up in the P&L.

WFC’s EPS GAAP hit $1.60 in Q1, up 15% year over year, while consensus estimates project further step-ups through 2026 as the credit card book matures, the auto lending expansion compounds, and the investment bank continues to gain wallet share from competitors who have known the Wells franchise for decades.

Nineteen of the 26 analysts covering Wells Fargo stock have it rated Buy, with a mean price target of $100 representing roughly 32% upside from current levels; what the consensus is waiting on is evidence that the NII trajectory inflects in the second half of the year as loan growth compounds beyond mid-single digits.

The NII miss creates a real short-term friction: Q1 net interest income came in at $12.1 billion against estimates of $12.3 billion, and if higher-for-longer rates keep deposit mix tilted toward interest-bearing accounts, that gap could persist into Q2, leaving WFC stock vulnerable to continued underperformance relative to peers.

With the asset cap lifted, the last consent order terminated, and loan balances crossing $1 trillion, Wells Fargo stock appears undervalued given the compounding EPS ramp and the 15% ROTCE already achieved before the bank has fully monetized its investment banking and markets investments.

Elevated energy prices and their lagged effect on consumer spending are the single development that, if it worsens materially, squeezes the consumer banking segment that generates over 40% of WFC’s revenue.

Q2 2026 earnings, expected in July, will be the first data point where investors can assess whether NII ex-markets has inflected as management guided, with the $50 billion full-year NII target the specific number to watch.

What Does the Valuation Model Say?

The TIKR valuation model captures what the income statement alone cannot: a bank repricing from regulatory discount to growth compounder, with the earnings ramp only now becoming visible in the reported numbers.

The TIKR model places WFC’s mid-case intrinsic value at $111 per share, based on a 3.3% revenue CAGR, a 24.7% net income margin, and a 5.2% EPS CAGR through 2030, assumptions that do not require the bank to reach its 17% to 18% ROTCE target to generate meaningful upside.

Trading at 10.56x NTM normalized earnings against a 5-year historical mean of 11.43x, Wells Fargo stock is priced below its own average despite carrying a cleaner balance sheet, a cleared regulatory record, and a loan book that just crossed $1 trillion for the first time since 2020.

WFC appears undervalued at a multiple that has only been this compressed during the deepest phases of the asset cap era, before the bank had any path to the earnings ramp now visibly underway.

The investment case hinges on whether loan growth and NII recovery arrive in the sequence management described, or whether energy-driven consumer pressure delays the timeline.

What Has to Go Right

- NII ex-markets inflects higher in H2 2026 as loan balances compound beyond mid-single-digit growth, validating the $50 billion full-year guidance

- Credit card vintages from 2022 and 2023 mature into profitability as delinquencies remain below model in both card and auto

- Investment banking and markets revenue continue gaining wallet share, with markets revenue already up 19% year over year in Q1 2026 and the pipeline described as “very active”

- Basel III capital rule implementation reduces WFC’s risk-weighted assets by approximately 7%, freeing excess capital for buybacks or further balance sheet deployment

What Could Go Wrong

- Consumer spending softens in H2 2026 as the lagged effect of elevated oil prices reduces spending across non-essential categories, compressing the consumer banking segment that drives over 40% of revenue

- Noninterest-bearing deposit growth remains slow, keeping deposit mix tilted toward higher-cost interest-bearing accounts and capping NII upside even as loan volumes rise

- Private credit exposure of $36.2 billion in corporate debt finance, while well-structured, attracts incremental regulatory scrutiny that increases remediation costs at exactly the moment the bank is trying to retire compliance overhead

- The GSIB surcharge, currently at 1.5%, moves to 2% as balance sheet growth accelerates, tightening the CET1 buffer and slowing buyback capacity

Should You Invest in Wells Fargo & Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Wells Fargo & Company stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Wells Fargo & Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze WFC stock on TIKR for Free →