Key Stats for Amphenol Stock

- 52-Week Range: $83 to $167

- Current Price: $128

- Street Mean Target: $182

- Street High Target: $215

- Analyst Consensus: 11 Buys, 4 Outperforms, 3 Holds, 1 Underperform

- TIKR Model Target (Dec. 2030): $206

What Happened?

Amphenol Corporation (APH) is one of the world’s largest manufacturers of electrical, electronic, and fiber optic connectors, with components threaded into AI data centers, defense systems, commercial aircraft, and industrial equipment across more than 40 countries.

Amphenol stock surged roughly 9.5% in premarket trading on April 29 after the company reported record first-quarter 2026 results that exceeded the high end of its own guidance on both revenue and adjusted earnings per share.

Revenue came in at $7.62 billion, up 58% from the same period a year ago and ahead of the $7.09 billion Wall Street had expected, marking the highest single-quarter revenue figure in the company’s history.

Adjusted diluted EPS reached $1.06, a 68% increase from $0.63 in Q1 2025 and well ahead of the $0.94 consensus estimate.

The IT datacom segment was the engine, representing 41% of total Q1 revenue and growing 99% in U.S. dollars, with 81% organic growth driven by accelerating demand for high-speed and power interconnect products used in AI infrastructure.

Orders hit a quarterly record of $9.435 billion, up 78% from the year-ago period and up 12% sequentially, producing a book-to-bill ratio of 1.24:1, a figure that signals strong near-term demand momentum well above a neutral 1.0 reading.

The January close of Amphenol’s $10.5 billion acquisition of CommScope’s Connectivity and Cable Solutions business added fiber optic and data-center rack-to-rack connectivity to the portfolio, a capability the company had previously participated in only at the margins.

CEO R. Adam Norwitt described the strategic logic directly on the Q1 2026 earnings call: “Now with CommScope, we have the industry’s broadest range of high-speed copper, power and fiber optics interconnect products, all of which are critical components in these next-generation systems and in the next-generation architectures of our customers.”

For Q2 2026, management guided revenue of $8.1 billion to $8.2 billion and adjusted diluted EPS of $1.14 to $1.16, representing year-over-year growth of 43% to 45% and 41% to 43%, respectively, both well above Street expectations at the time of the report.

Defense, industrial, and commercial aerospace each showed broad organic growth, reinforcing that the AI tailwind is running alongside a separate structural upcycle in defense procurement and industrial electrification.

Wall Street’s Take on APH Stock

Amphenol stock’s record quarter doesn’t just validate Q1; it resets the earnings trajectory for the full year in a way that consensus had not yet priced before the print.

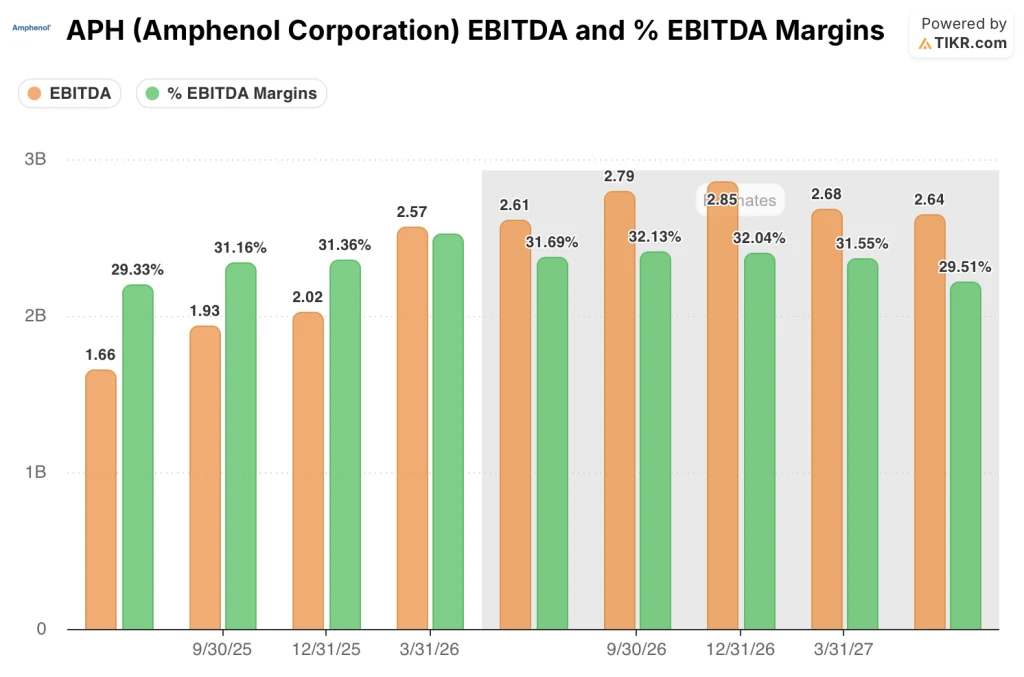

With a $10.5 billion acquisition closing in January and 81% organic growth running simultaneously in its largest segment, EBITDA is the metric that matters here.

APH posted $2.567 billion in Q1 EBITDA, up 87.9% from the year-ago quarter, with EBITDA margins expanding to 33.7% against a consensus expectation of 29.7%.

Looking ahead, Street consensus puts Q2 EBITDA at around $2.61 billion and full-year 2026 EBITDA approaching around $11 billion, implying continued mid-to-high double-digit year-over-year growth as CommScope scales within the Amphenol operating model.

Fifteen analysts cover Amphenol with active price targets. Eleven rate it a buy, four rate it outperform, three hold, and one underperforms. The mean price target sits at $181.72, implying roughly 42% upside from the current price of $128.03, with the high target reaching $215 and the low at $135. Wall Street is waiting for CommScope margin trajectory to prove out and for Q2 order momentum to confirm that the 1.24:1 book-to-bill wasn’t a pull-forward event.

The bull-to-bear spread from $135 to $215 hinges on a single question: whether AI infrastructure capex remains durable through 2026 and 2027, or whether hyperscaler spending normalizes faster than the current order book implies.

The signal worth noting: Norwitt’s disclosure that customers are “opening up order apertures” as part of capacity investment partnerships is not standard contract language for the connector industry, and it suggests demand visibility that doesn’t show up cleanly in book-to-bill alone.

The risk is the CommScope integration absorbing more management bandwidth than expected, particularly as the team attempts to migrate a decades-old corporate culture onto Amphenol’s decentralized operating model while also meeting record organic demand.

The catalyst to watch is the Q2 report: whether organic growth in IT datacom sustains into the low-teen sequential growth guided by management, and whether EBITDA margins hold above 31% inclusive of CommScope dilution.

What Does the Valuation Model Say?

The TIKR model prices APH at a mid-case target of $206 by December 2030, built on a revenue CAGR of around 11% from 2025 through 2035 and a net income margin assumption of around 20%, both of which find direct support in the Q1 result: Amphenol already posted 18% net income margins in Q1 2026 with CommScope still in its first full quarter of integration.

At $128, Amphenol stock is priced at a discount to a business that just doubled its quarterly revenue run rate in two years, is absorbing a transformative acquisition without margin deterioration, and carries a record order book into Q2.

The TIKR model’s mid-case implies a total return of around 103% through 2034, with an annualized IRR of around 8.5%, making APH undervalued for investors with a multi-year horizon who are willing to hold through near-term integration noise.

The argument hinges on one question: can Amphenol translate CommScope’s fiber optic capabilities into the same margin profile it runs across its core connector business?

If CommScope performs:

- CommScope revenue is already tracking well ahead of the mid-teens growth assumed at deal announcement, with Q1 performance roughly in line with Amphenol’s own 33% organic growth rate

- EBITDA margins expanded to 33.7% in Q1 2026 despite CommScope dilution, 394 basis points above Street estimates

- Management expects CommScope to contribute approximately $4.1 billion in 2026 revenue and $0.15 of EPS accretion, ahead of initial deal assumptions

- Defense organic growth of 25% in 2025 and 44% year-over-year in Q1 2026 provides a durable second revenue engine independent of AI

If CommScope underperforms:

- The $10.5 billion deal was funded in part through euro-denominated debt, and Amphenol priced EUR 1.1 billion in additional senior notes in May 2026 to manage near-term maturities, a sign that the balance sheet carries real leverage at net debt of $14.2 billion and a 1.6x net leverage ratio

- The adjusted tax rate rose to 27% in Q1 2026 from 24.5% a year ago, partly driven by a China tax matter totaling $230 million in charges, a cost that compresses after-tax returns and is not yet fully resolved

- If AI hyperscaler spending decelerates in 2027, IT datacom at 41% of revenue creates meaningful concentration risk, and CommScope’s fiber revenue would be doubly exposed

Should You Invest in Amphenol Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Amphenol Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Amphenol Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze APH stock on TIKR for Free →