Key Stats for IBM Stock

- 52-Week Range: $161.13 to $253.69

- Current Price: $229.76

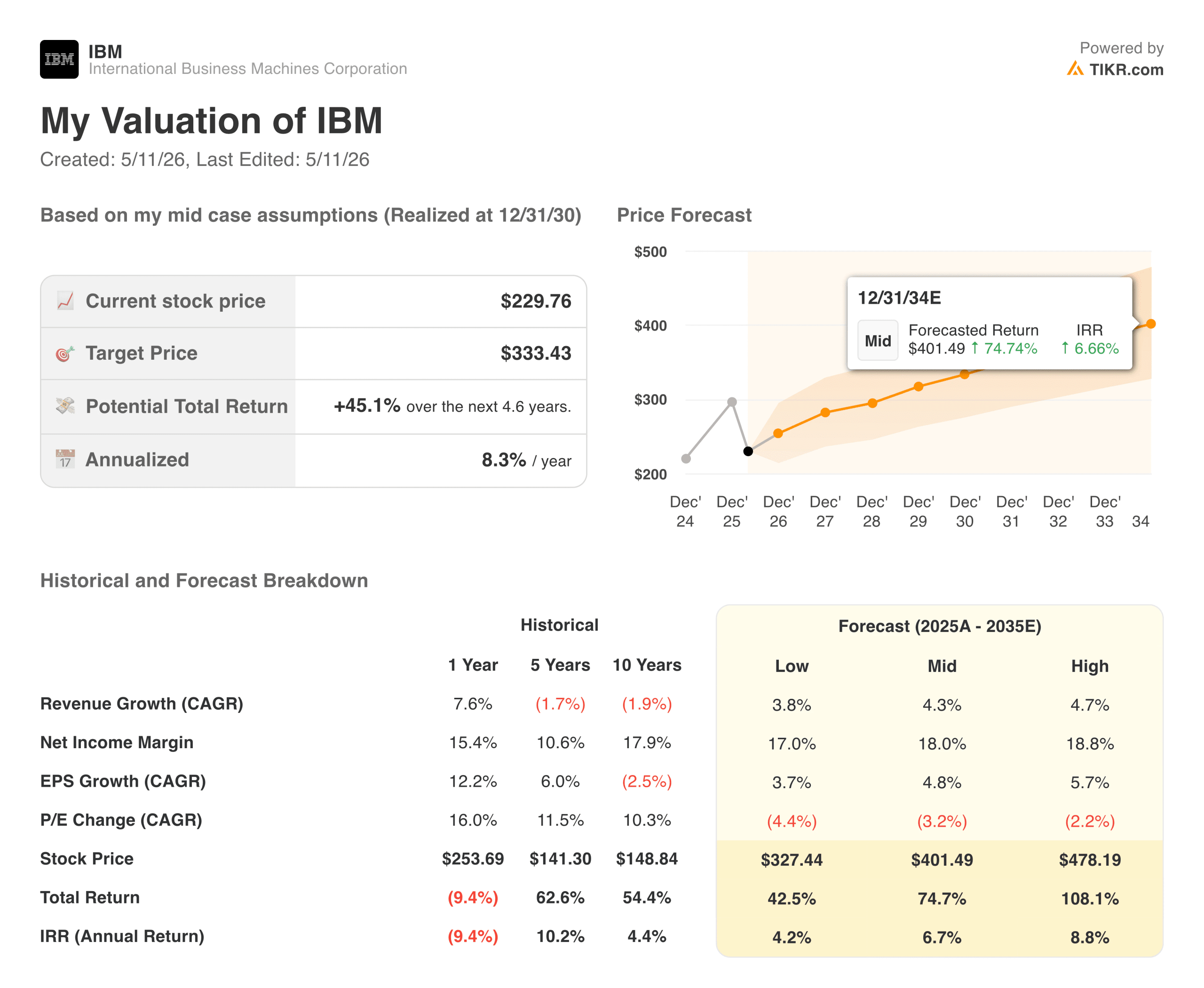

- TIKR Target Price (Mid): ~$333

- TIKR Annualized IRR (Mid): ~8% per year

- Q1 2026 Revenue: $15.9 billion, up 9%

- Q1 2026 Operating EPS: $1.91, up 19% year over year

- Gen AI Book of Business: $12.5 billion+

Value your favorite stocks like IBM with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

Why a Strong Quarter Sent the Stock Lower

IBM (IBM) reported Q1 2026 results on April 22nd and beat on nearly every metric that matters. Revenue came in at $15.9 billion, above the consensus of around $15.6 billion. Operating EPS of $1.91 beat the $1.81 estimate by around 6%. Free cash flow hit its highest level in a decade. Software grew 11%, Red Hat grew 13%, and the z17 mainframe cycle produced a 51% jump in IBM Z revenue.

The stock fell 6% in after-hours trading anyway.

The reason is straightforward. IBM maintained its full-year 2026 guidance for more than 5% constant currency revenue growth and a $1 billion increase in free cash flow, rather than raising it, and a market that had priced in an upgrade walked away disappointed. That reaction created something worth paying attention to: a business delivering genuine results at a price that does not reflect them.

See what analysts think about IBM stock right now (Free with TIKR) >>>

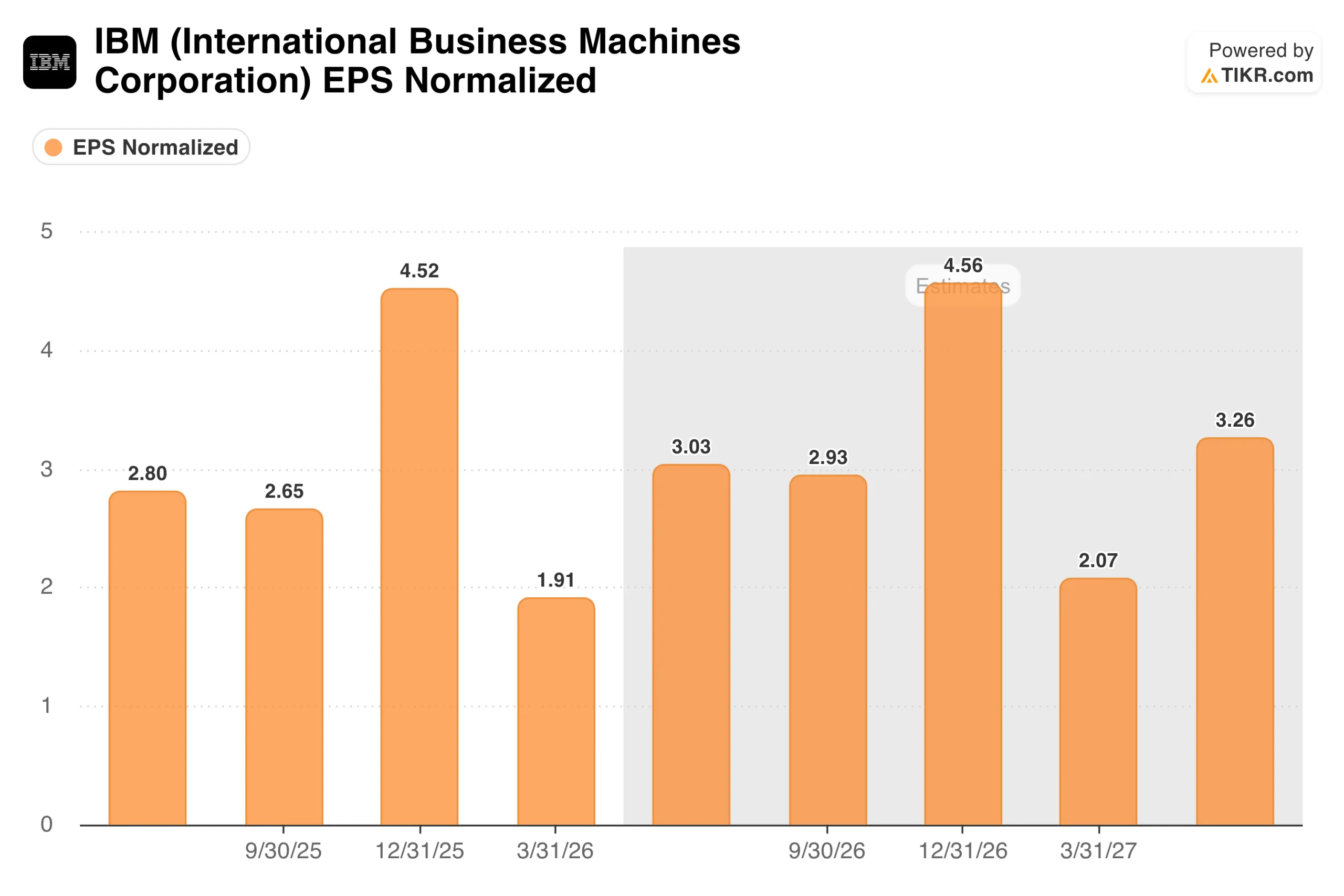

What the EPS Chart Is Actually Showing

The EPS chart requires some context before drawing conclusions from it. IBM’s earnings are heavily seasonal, with Q4 consistently producing the largest quarter of the year and Q1 the smallest. The $4.52 in Q4 2025, followed by $1.91 in Q1 2026, is not a sign of deterioration. It is the normal rhythm of a business, with enterprise software renewals, hardware deployments, and consulting project completions clustering toward year-end.

What the chart clearly shows is that Q1 2026 EPS of $1.91 represents around 19% growth over Q1 2025, which is the comparison that matters. Analysts are modeling Q2 2026 at around $3.03 and Q4 2026 at around $4.56, representing modest growth over the prior-year equivalents. The Confluent acquisition is expected to create around $600 million in EPS dilution in 2026, indicating the underlying business is growing faster than the headline numbers suggest.

Value IBM instantly (Free with TIKR) >>>

45% Upside in the Mid Case, With a Business Hiding in Plain Sight

TIKR’s model targets around $333 in the mid-case, implying a total return of about 45% over roughly 4.6 years, or about 8% annualized. The model assumes revenue growth of around 4% annually and net income margins expanding toward 18%. That margin assumption is already within reach, given the current trajectory.

IBM is one of those businesses that gets chronically underestimated because the brand carries two decades of legacy connotations. The company today generates $7 billion per quarter in software revenue, runs the largest enterprise AI consulting practice in the world with a book of business exceeding $12.5 billion, and is in the middle of a mainframe upgrade cycle that will drive infrastructure revenue over the next several years.

What the Bulls Are Counting On

- Software is compounding at double digits, and the mix is improving. Software is now IBM’s largest revenue segment and its highest-margin business. Red Hat grew 13% in Q1, the Data segment grew 19%, and Automation grew 10%. As software becomes a larger share of total revenue, the overall margin profile improves structurally. IBM now expects software to grow above 10% for the full year, which is the growth rate that justifies a re-rating of the multiple.

- The AI book of business is a real number, not a marketing figure. Over $12.5 billion in gen AI commitments across software and consulting is the largest such figure among enterprise technology companies that are not hyperscalers. That backlog converts into recurring software revenue and multi-year consulting engagements, both of which carry above-average margins and high renewal rates.

- The z17 mainframe cycle adds a durable earnings layer. The mainframe business is one that most investors forget IBM still has, and it is currently in the strongest upgrade cycle in years. IBM Z revenue grew 51% in Q1 2026, and management expects this to be the strongest z cycle given the AI innovation being delivered on the platform. That is a multi-quarter tailwind that does not depend on enterprise software growth or consulting demand to materialize.

- Free cash flow is at its highest level in a decade. IBM guided for a $1 billion increase in FCF for 2026, which is not a trivial number for a business of this size. That cash funds the dividend, which IBM has paid and grown for decades, and supports the ongoing share buyback program.

What the Bears Are Watching

- Consulting growth is stubbornly slow. At 4% reported and just 1% at constant currency in Q1, consulting is not delivering the acceleration the long-term model requires. Consulting carries lower margins than software and is more exposed to client budget cycles and macroeconomic softness. If consulting growth remains in the low single digits, the overall revenue growth story remains modest.

- Confluent dilution is a real near-term headwind. The Confluent acquisition is expected to dilute operating EPS by around $600 million in 2026. That is a meaningful drag in a year when the underlying business is otherwise delivering double-digit earnings growth, making the headline EPS numbers look softer than the actual business performance would suggest.

- The model’s 8% annualized return is modest for the risk. At around $230, IBM is not pricing in growth, but it is not pricing in a disaster either. The mid-case return of 8% per year is reasonable for a business of this quality and stability, but investors looking for a more compelling risk-reward can find higher implied returns elsewhere in the market right now.

Should You Invest in IBM

IBM is the kind of stock that rewards patience and punishes impatience. The transformation Arvind Krishna has been running since 2020 is producing real results in the numbers, but the market keeps expecting a faster pace of change than a company of IBM’s scale can deliver in any single quarter.

The gap between a beat on every major metric and a 6% stock decline on the day of earnings is the clearest signal of what this stock is pricing in. At around $230 against a TIKR mid-case target of around $333, the implied return over roughly four and a half years is around 45%.

The next meaningful data point is Q2 2026 earnings, scheduled for July 23rd, where the key question is whether consulting revenue growth begins to accelerate toward the low- to mid-single-digit range that management has been guiding toward all year.

See analysts’ growth forecasts and price targets for IBM stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!