Key Stats for Carnival Stock

- Current Price: $26.38

- Target Price (Mid): ~$50

- Street Target: ~$34 (mean of 21 price target estimates)

- Potential Total Return: ~90%

- Annualized IRR: ~15% / year

- Earnings Reaction: (0.95%) on March 27, 2026

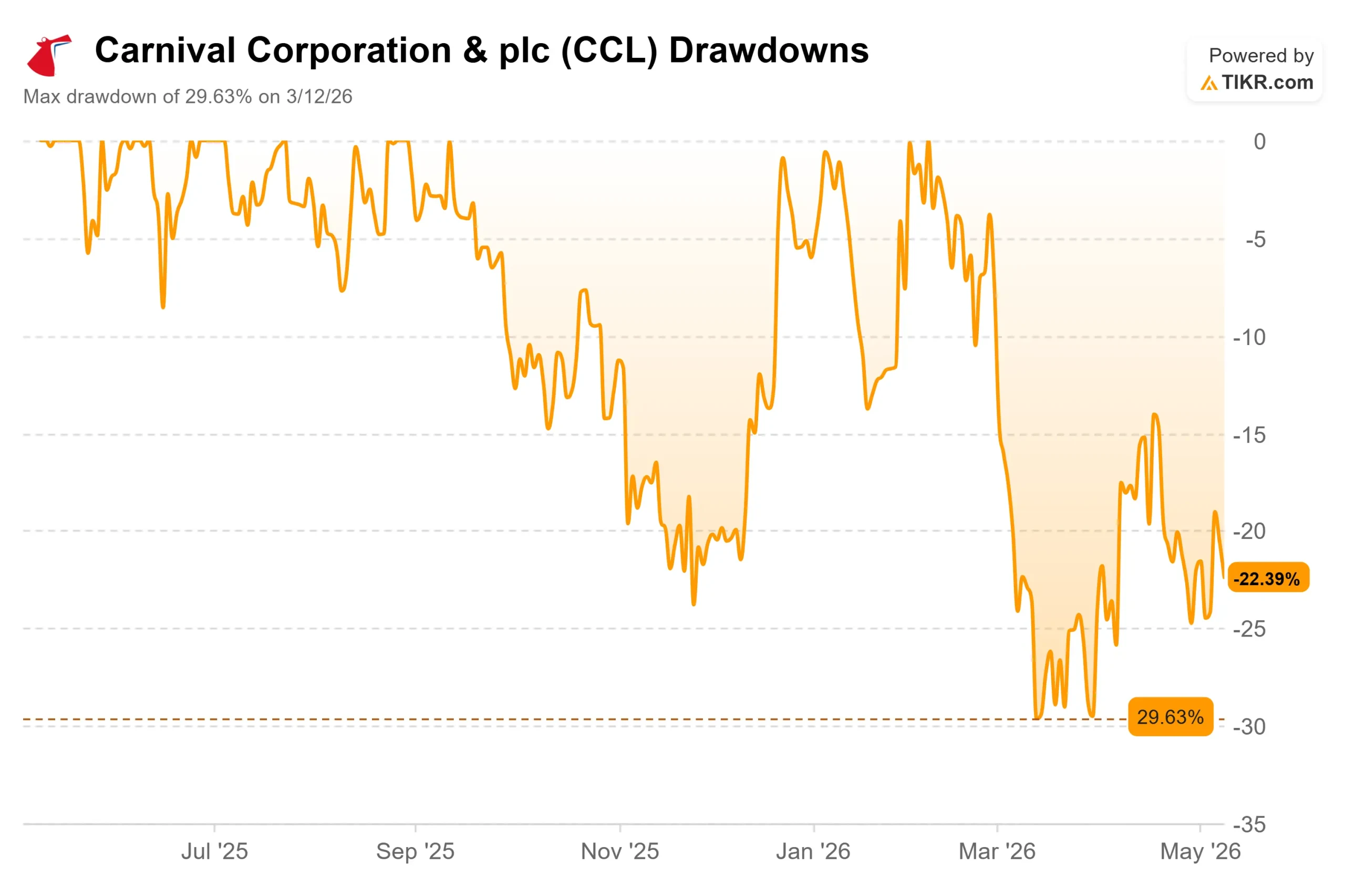

- Max Drawdown: 29.63% on March 12, 2026

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Cruise stocks are under pressure again. Carnival Corporation (CCL) has fallen roughly 22% from its 52-week high of $34.03, weighed down by a fuel cost spike tied to Middle East geopolitical tensions and broad weakness in consumer cyclicals. Bears point to a $500 million fuel headwind eating into 2026 earnings. Bulls argue the demand picture has never been stronger. The question the market is actively debating: does the selloff reflect real fundamental damage, or has it created an entry point into a business executing at a record level?

That tension sharpened this week. On May 7, Carnival completed the unification of its dual-listed company structure, consolidating Carnival Corporation and Carnival plc under a single Bermuda-incorporated entity now trading solely on the NYSE under CCL. The London Stock Exchange listing, which had existed since 2003, was canceled. On May 8, Carnival declared a $0.15 per share dividend. Both actions came on top of a record Q1 earnings report and the launch of a new multi-year growth plan that the current share price does not appear to reflect.

See historical and forward estimates for Carnival stock (It’s free!) >>>

Record Results Behind the Noise

Q1 2026 was operationally strong across every headline metric. Revenue came in at $6.2 billion, a record for the fiscal first quarter. Net income of $275 million was more than 55% above the prior year, beating guidance by $40 million. Adjusted EPS of $0.20 rose 50% year over year. Customer deposits reached nearly $8 billion, up almost 10% from the prior year’s record. With nearly 85% of 2026 already booked at historically high prices and bookings extending well into 2028, the demand engine is intact despite the macro uncertainty.

At the March 27 earnings call, CEO Josh Weinstein introduced PROPEL, which stands for Powering Growth and Returns, Responsibly. The plan targets return on invested capital above 16% and earnings per share growth of more than 50% versus 2025, both by 2029, with more than $14 billion returned to shareholders over the period. Weinstein framed the engine behind it plainly: “At its core, PROPEL is about converting strong and growing demand into higher returns, earnings, and cash flow while maintaining disciplined capacity growth and a strong balance sheet.”

The $2.5 billion buyback announced alongside PROPEL is explicitly described as a starting point. CFO David Bernstein confirmed: “Clearly, over this period with $14 billion of expected shareholder returns, there’ll be additional stock buybacks.” With only three new ships entering service across Carnival’s 96-ship fleet during the PROPEL period, the company is prioritizing returns on existing assets over volume growth. That capital discipline is new relative to the pre-COVID playbook, and the market has not fully priced it.

The Fuel Bear Case and What It Misses

The bear argument is straightforward. Carnival guided fiscal 2026 EPS at $2.21, absorbing a $0.38 per share fuel headwind. Norwegian Cruise Line Holdings cut its own annual profit forecast on May 4, citing the same elevated energy costs, dragging sentiment across the cruise sector. Multiple analysts flagged fuel-driven downgrade risk for CCL specifically. The stock’s 29.63% maximum drawdown from its peak reflects that anxiety directly.

But the fuel narrative alone is incomplete. That $500 million headwind lands against a full-year EBITDA target of approximately $7 billion. And Carnival’s consumption efficiency gains have already saved approximately $650 million in fuel costs this year versus 2019 levels, more than offsetting the current spike in dollar terms. The company is not standing still either: Brent crude is already assumed to moderate to $80 per barrel by Q4 in guidance. CFO Bernstein noted that a 10% change in fuel cost per metric ton for the remainder of fiscal 2026 moves the bottom line by approximately $160 million or $0.11 per share, giving investors a clean sensitivity framework to model scenarios themselves.

The completed DLC unification adds a structural angle that the fuel narrative ignores. Per Carnival’s own press release, the consolidation creates a single global share price, streamlines governance and reporting, and is expected to reduce administrative costs. Separately, on valuation, CCL trades at 8.61x NTM EV/EBITDA against Royal Caribbean’s 12.34x and Norwegian Cruise Line’s 9.33x, per TIKR’s Competitors page. Carnival’s discount partly reflects its higher leverage, but the $14 billion return commitment and measured capacity strategy make the gap harder to justify on fundamentals alone.

See how Carnival performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $26.38

- Target Price (Mid): ~$50

- Potential Total Return: ~90%

- Annualized IRR: ~15% / year

See analysts’ growth forecasts and price targets for Carnival stock (It’s free!) >>>

The mid-case assumes a revenue CAGR of around 3% and a net income margin of around 13%, consistent with PROPEL’s expectation that yield growth runs ahead of low-single-digit cost growth. Two revenue drivers underpin the CAGR: continued commercial improvement across marketing, revenue management, and personalization technology; and onboard spending growth, where guests are pre-purchasing packages and excursions before boarding, a trend Weinstein called out explicitly in Q1 as a meaningful contributor to yield expansion.

The upside case (around 15% IRR, ~$85 stock price by 2034) assumes yield growth accelerates as Carnival’s private destination portfolio matures and the ship revitalization program drives premium pricing. The downside case (around 10% IRR, ~$58 stock price by 2034) assumes sustained fuel pressure and softer yields, but still prices in significant appreciation from today. On free cash flow, TIKR estimates FCF growing from around $4 billion in fiscal 2026 to approximately $5.4 billion by fiscal 2030.

At 8.61x NTM EV/EBITDA and 12.23x NTM P/E, with 15 Buys, 5 Outperforms, and 5 Holds from 25 analysts and a Street mean target of around $34, consensus already sees meaningful upside from here. The TIKR mid-case to 2030 suggests the long-term setup is considerably more compelling than the near-term Street target implies, if PROPEL executes as outlined.

Conclusion

Watch net yield growth at the Q2 2026 earnings call on June 22. Guidance calls for around 2% constant currency yield growth. If actual yields clear that threshold while onboard spending holds, it confirms fuel costs are not eroding demand, and PROPEL stays on track. The one-sentence thesis: Carnival is executing at a record level, has structured itself for the next decade of returns, and the current share price does not yet reflect either of those facts.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Carnival?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Carnival, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Carnival alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Carnival on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!