Key Stats for Walmart Stock

- Current Price: $130.43

- Street Mean Target: ~$137

- Earnings Reaction (Feb. 19, 2026): -1.51%

- TIKR Mid-Case Price: ~$181 | ~38% total return | ~4% IRR/yr

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

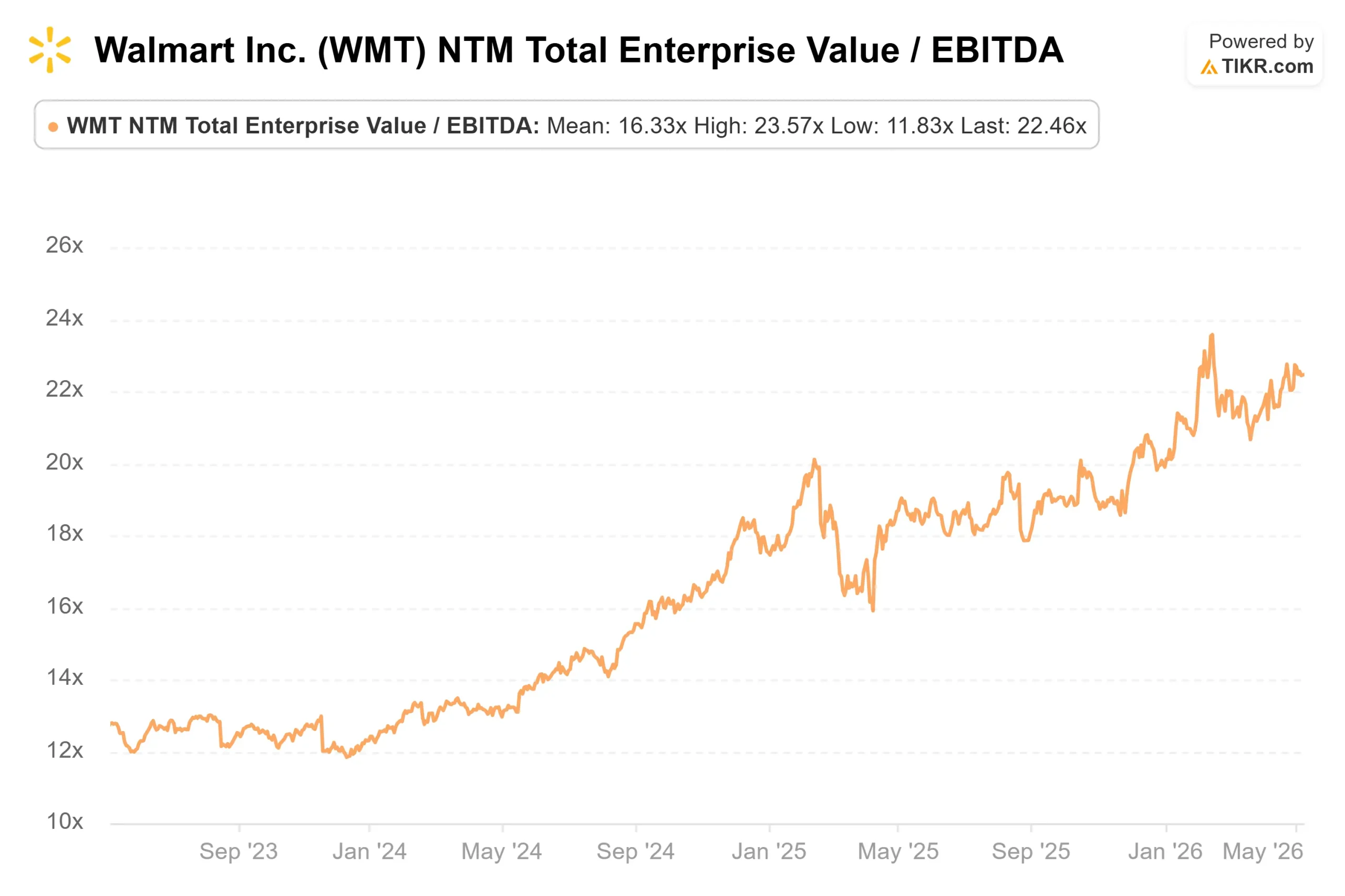

Walmart (WMT) has delivered a 34.8% return over the past year, and the question the market is asking right now is whether a roughly 45x forward earnings multiple is sustainable as the business changes underneath it. Bulls say Walmart is mid-innings in a platform transformation that will push operating margins back toward historical highs. Bears say those gains are already priced in at $130. On April 8, CFO John David Rainey walked into JPMorgan’s 12th Annual Retail Roundup and spent an hour laying out exactly what that transformation looks like, milestone by milestone, in one of the most specific public accounting management has offered.

With Q1 FY2027 earnings arriving May 21, the clock is ticking on whether the numbers confirm the narrative.

See historical and forward estimates for Walmart stock (It’s free!) >>>

What Rainey Said at J.P. Morgan

Three things Rainey described at the conference are already in motion, not aspirational.

The first is e-commerce profitability. An e-commerce transaction at Walmart today is still less profitable than an in-store one. Rainey said so directly and then named the inflection point: “Within our planning horizon, we expect that we will get to a point where an e-commerce transaction fully loaded with the other benefits will become more profitable than an in-store transaction. That’s a monumental point in time for us.” He tied it to automation, lowering marginal fulfillment costs and advertising layering on top. He also confirmed Walmart is already seeing double-digit incremental margins in e-commerce today, ahead of that crossover.

The second is advertising. Rainey described the ad business as “early to mid-innings” relative to best-in-class penetration, which he said is roughly twice Walmart’s current advertising dollars as a share of GMV. Walmart’s global advertising reached $6.4 billion in fiscal year 2026, with Walmart Connect in the U.S. growing 41% in Q4. The VIZIO acquisition adds something new: non-endemic advertising, meaning inventory for products Walmart does not carry. Rainey called that “in the first inning” high-margin revenue with no meaningful incremental capex.

The third is agentic commerce. Roughly half of Walmart’s app users are already engaging with Sparky, its AI shopping assistant. Customers who buy through Sparky carry a basket 35% larger than those who don’t, Rainey said at the conference. In March 2026, Walmart embedded Sparky directly into ChatGPT and Google Gemini after its OpenAI Instant Checkout pilot produced conversion rates three times lower than Walmart’s own site figures, which Walmart disclosed publicly via CNBC and WIRED. The move was deliberate: Walmart uses AI platforms as customer acquisition channels while retaining the checkout, the data, and the post-purchase relationship.

That data retention is directly tied to ad yields. Rainey made the point explicitly at J.P. Morgan: knowing a customer searched for camping gear before arriving at Walmart allows for more targeted advertising, which could increase return on ad spend even if some ad dollars shift to AI platforms.

What the Consumer Looks Like Heading Into May 21

Rainey pushed back on the pessimistic consumer narrative at J.P. Morgan: “I am probably more constructive on the consumer than what one would glean from reading the headlines.” He said tax refunds provided a bigger tailwind than expected when Q1 guidance was set in February, and that the quarter is tracking in line with that guidance.

The risk he flagged seriously was oil. At above $100 per barrel, fuel costs flow through to food via fertilizer and transport, and Walmart has already absorbed over $100 million in fuel-related headwinds this quarter. How long prices stay elevated is the watch item.

Walmart guided Q1 FY2027 for constant-currency net sales growth of 3.5% to 4.5% and operating income growth of 4% to 6%, with adjusted EPS of $0.63 to $0.65. On May 7, TD Cowen analyst Oliver Chen raised his price target from $145 to $150, citing durable grocery traffic and easier general merchandise comparisons. BTIG also raised its target from $140 to $145 the same week.

One pattern worth noting from the TIKR Beats & Misses data: WMT has fallen on earnings day in four of its last five reports, including a -1.51% reaction on February 19 despite beating adjusted EPS estimates of $0.73 with an actual $0.74. The market reacts to guidance, not the beat itself. On May 21, the number that matters is operating income growth, specifically whether it confirms the margin trajectory is intact.

See how Walmart performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

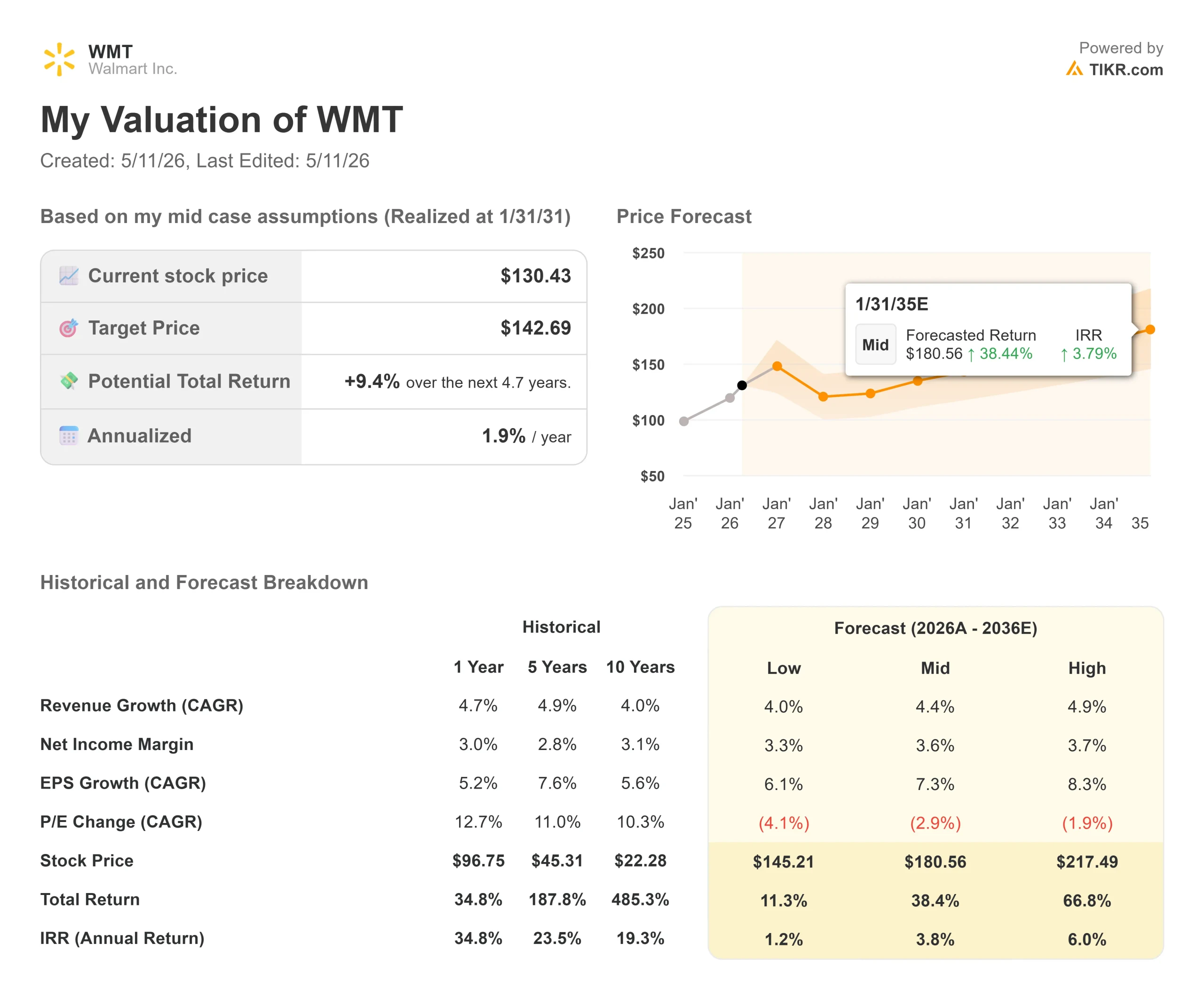

- Current Price: $130.43

- TIKR Mid-Case Price: ~$181 | ~38% total return | ~4% IRR/yr

See analysts’ growth forecasts and price targets for Walmart stock (It’s free!) >>>

The mid case assumes around 4% revenue CAGR, driven by continued e-commerce share gains in the U.S. and margin improvement at Flipkart and the Mexico business as they replicate the advertising and fulfillment flywheel. Net income margins expand into the mid-3% range as the business mix shifts toward higher-margin digital revenue. The primary margin driver is advertising, which Rainey said has room to roughly double its penetration as a share of GMV.

The honest near-term picture: a ~9% total return to January 2031 at around 2% annualized is not a compelling return for most equity investors. At roughly 45x forward earnings, most of the near-term upside is priced in. The longer-dated case is more interesting, around 38% total return to 2035 in the mid scenario and around 67% in the high case, if Sparky monetization and VIZIO’s non-endemic advertising scale. The primary risk is a prolonged energy shock that bleeds into food inflation faster than Walmart’s pricing and mix management can absorb, compressing free cash flow precisely as capex peaks in FY2027. The upside: if the e-commerce profitability crossover Rainey described arrives by FY2029, operating margins recover toward the 6–7% range he referenced at J.P. Morgan, and the re-rating on that earnings power justifies today’s multiple.

Conclusion

The single number to watch on May 21 is operating income growth against the 4%–6% guided range. A result at or above the midpoint confirms the margin story is on track. Walmart’s transformation into a platform business with advertising, membership, and AI commerce layered on top is one of the more durable structural stories in consumer staples, but at roughly 45x forward earnings, it does not come cheap, and near-term returns will be modest unless May 21 resets operating income expectations upward.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Walmart?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Walmart, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Walmart alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Walmart on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!