Key Stats

- Current Price: $75 (May 12, 2026)

- Q1 2026 Revenue: $346M, up 5% YoY

- Q1 2026 Adjusted EPS: $0.59 per diluted share

- Q1 2026 Adjusted EBITDA: $190M, up 7% YoY (new company record)

- FY2026 Adjusted EBITDA Guidance: $820M to $860M

- FY2026 Discretionary Cash Flow Guidance: $520M to $570M

- Power Infrastructure Revenue Guidance (FY2026): $95M to $125M

- TIKR Model Price Target: $101

- Implied Upside: ~34% from current price

Kodiak Gas Services Q1 2026 Earnings Breakdown

Kodiak Gas Services stock delivered $346M in Q1 2026 revenue, up 5% year over year, while adjusted EBITDA hit $190M, a 7% increase and a new company record, according to CFO John Griggs on the Q1 2026 earnings call.

Contract services led the quarter, with revenues rising 6% year over year and 2% sequentially as revenue-generating horsepower expanded by approximately 35,000 units.

Contract services adjusted gross margin reached 70.6%, a 286-basis-point improvement year over year and a seventh consecutive quarterly increase, according to Griggs on the Q1 2026 earnings call.

“Adjusted EBITDA for the quarter was up 7% versus the prior year quarter, landing at a new company record of $190 million,” said Griggs, crediting investments in telemetry technology and workforce training for the margin gains.

Adjusted net income was $52M, with diluted EPS of $0.59 for the quarter, according to the Q1 2026 earnings call.

Other Services segment revenues rose 25% sequentially as station construction activity picked up, with margins improving to approximately 16% on a richer mix of higher-margin activity, according to Griggs on the Q1 2026 earnings call.

On the strategic front, Kodiak closed the acquisition of DPS on April 1 and formally launched the distributed power business as Kodiak Power Solutions, creating a new Power Infrastructure reporting segment.

Kodiak entered a 10-year compression services contract extension with a top customer during Q1 and is finalizing a second 10-year extension with another customer, according to CEO Mickey McKee on the Q1 2026 earnings call.

The company also completed a purchase-leaseback transaction in the Permian, acquiring a package of large horsepower compression units from a producer and signing a 7-year contract to provide compression services, according to McKee on the Q1 2026 earnings call.

Kodiak has sourced more than 260 megawatts of power generation capacity and is in advanced discussions to acquire an additional 1.3 gigawatts, targeting a distributed power fleet of approximately 2 gigawatts by year-end 2030, according to McKee on the Q1 2026 earnings call.

Power growth CapEx guidance for 2026 was set at $400M to $500M, with approximately $90M tied to equipment to be delivered this year and the remainder for 2027-and-beyond deliveries, according to Griggs on the Q1 2026 earnings call.

Updated FY2026 guidance lifted the adjusted EBITDA range to $820M to $860M and discretionary cash flow to $520M to $570M, reflecting the DPS acquisition contribution across three quarters.

The Board declared a dividend of $0.49 per share, covered 2.9x by Q1 discretionary cash flow of $126.5M, according to Griggs on the Q1 2026 earnings call.

Kodiak Gas Services Stock: What the Financials Show

The income statement shows Kodiak Gas Services stock underpinned by steady operating leverage, with gross margin and operating income both expanding in Q1 2026 even as revenue growth slowed from the prior-year pace.

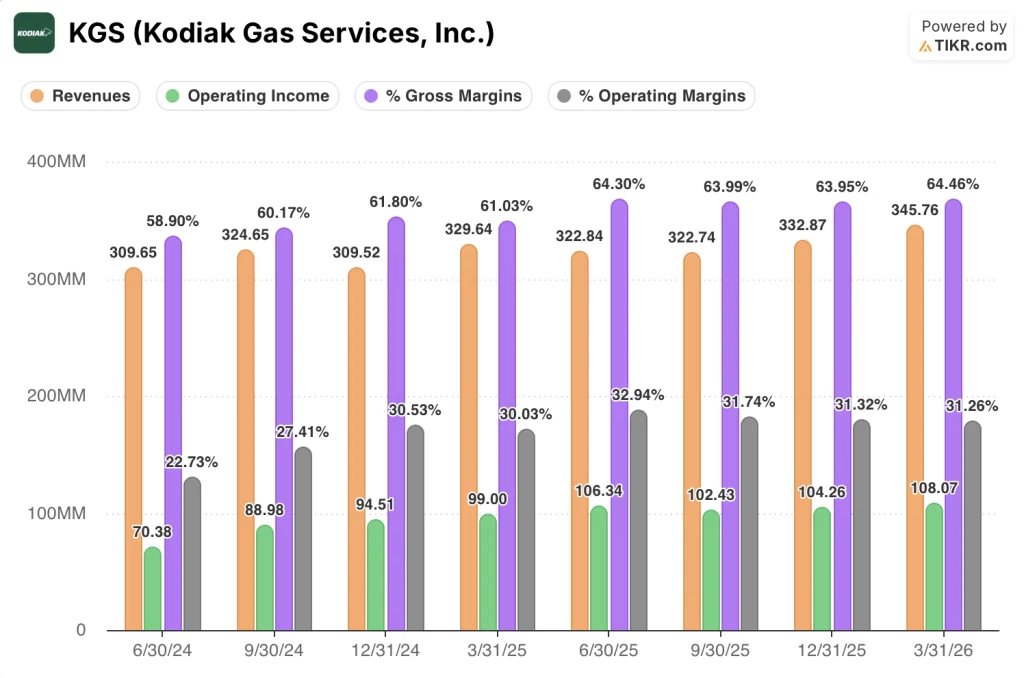

Revenue has held a narrow sequential band across the last four quarters: $323M in Q1 2025, $323M in Q2 2025, $323M in Q3 2025, $333M in Q4 2025, and $346M in Q1 2026.

Gross margin has moved consistently higher over that stretch: 61% in Q1 2025, 64% in Q2 2025, 64% in Q3 2025, 64% in Q4 2025, and 65% in Q1 2026.

Operating income followed the same direction, rising from $99M in Q1 2025 to $106M in Q2 2025, then $102M in Q3 2025, $104M in Q4 2025, and $108M in Q1 2026.

Operating margin held in a tight range through the back half of 2025 at 31% to 33%, with Q1 2026 at 31%.

The margin durability management described on the call is visible in the data: the 70.6% contract services adjusted gross margin Griggs cited on the Q1 2026 earnings call is consistent with what the income statement shows at the gross profit line, where costs declined sequentially despite higher revenue.

What Does the Valuation Model Say?

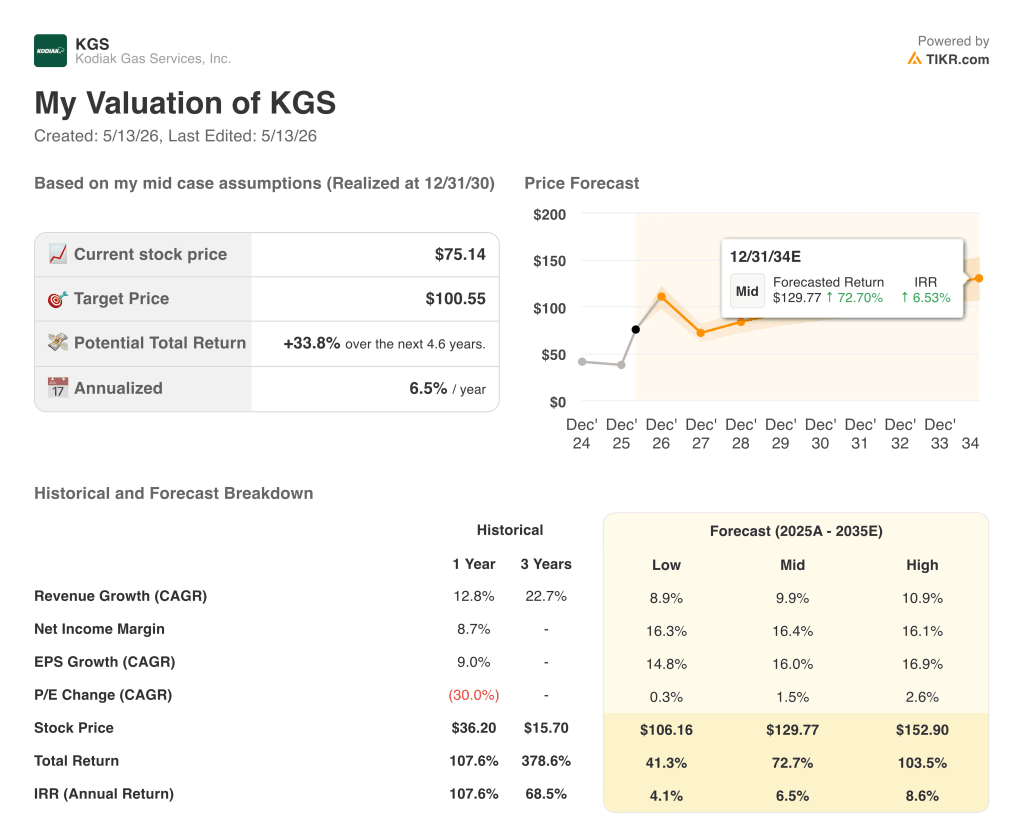

The TIKR model prices Kodiak Gas Services stock at $100.55, implying approximately 34% upside from the current price of $75.14 over the next 4.6 years, with an annualized return of 6.5%.

The mid-case assumes a revenue CAGR of 9.9% through 2035 and a net income margin of 16.4%, both materially above recent trailing figures, with P/E multiple expansion of 1.5% annually embedded in the target.

The Q1 record EBITDA, seventh consecutive contract margin high, and 10-year contract extensions reinforce the revenue growth assumption, but the mid-case return of 6.5% annualized is modest given where those assumptions sit.

Kodiak Gas Services stock is trading at a meaningful discount to model fair value, but the real upside optionality hinges on whether the Power Infrastructure buildout converts pipeline discussions into contracted revenue at scale, not on the compression base alone.

Kodiak Gas Services stock is priced on compression infrastructure durability; the variable now is whether $400M to $500M in uncontracted power CapEx generates 15%-plus unlevered returns within a timeline the model can credit.

What Has to Go Right

- Contract services adjusted gross margin reached 70.6% in Q1, a seventh consecutive quarterly record, and must hold in the 68.5% to 70% full-year guidance range as lube oil and fuel costs rise in the second half

- Kodiak has 2027 and 2028 large horsepower compression deliveries fully secured against lead times now exceeding 180 weeks for 3,600-horsepower inline engines, insulating revenue-generating horsepower growth toward the 5.2 million horsepower target

- The DPS data center contract, operating in its third year with 99.9% reliability, provides a proof point that Kodiak Power Solutions can win and execute long-term primary power contracts with hyperscalers

- Advanced discussions on an additional 1.3 gigawatts of capacity, if contracted over the next several months, would translate the power CapEx from speculative deployment to a defined earnings ramp toward the 2 gigawatt 2030 target

What Could Still Go Wrong

- Power Infrastructure guidance of $95M to $125M in revenue covers only three quarters of DPS contribution, with the 61 megawatts of additional equipment ordered in 2026 generating no material revenue until early 2027, meaning the CapEx burden arrives before the earnings benefit

- The $400M to $500M in power growth CapEx is being deployed ahead of binding contracts, and management acknowledged on the Q1 2026 earnings call that the pipeline is at the discussion stage with frameworks not yet finalized

- Net debt stood at $2.7B at quarter end with a credit agreement leverage ratio of 3.6x; management signaled leverage will drift above the 4x long-term target as the power investment cycle accelerates, compressing financial flexibility if contracts are delayed

- The compression business, while resilient, faces a guide range that bakes in margin pressure from higher oil prices in the second half, and any demand softening from Permian operators would reduce the cash flow cushion funding the power buildout

Should You Invest in Kodiak Gas Services, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Kodiak Gas Services stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Kodiak Gas Services stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze KGS stock on TIKR for Free →