Key Stats

- Current Price: CA$75 (May 11, 2026)

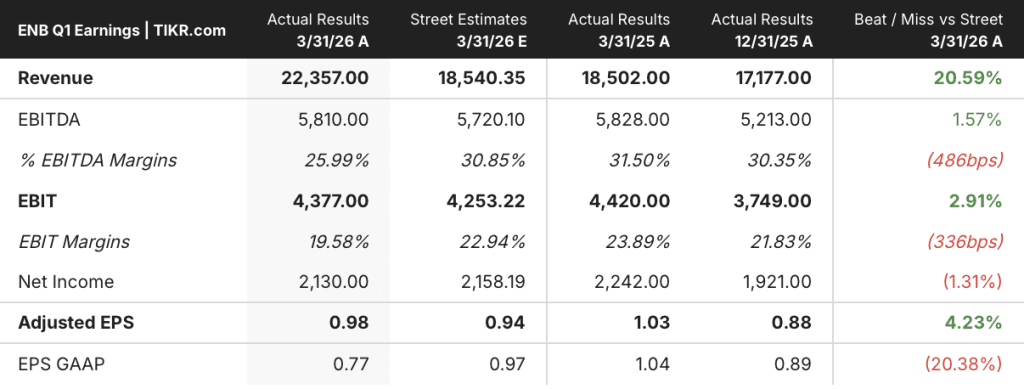

- Q1 2026 Revenue: CA$22,357M (up 20.6% YoY)

- Q1 2026 Adjusted EPS: $0.98 (up from $0.88 QoQ; down from $1.03 YoY)

- Q1 2026 EBITDA: CA$5,810M (up 11.5% QoQ; down 0.3% YoY)

- 2026 EBITDA Guidance: Reaffirmed (midpoint)

- 2026 DCF/Share Guidance: Reaffirmed (midpoint)

- Post-2026 Growth Outlook: 5% average annual EBITDA, DCF/share, and EPS through end of decade

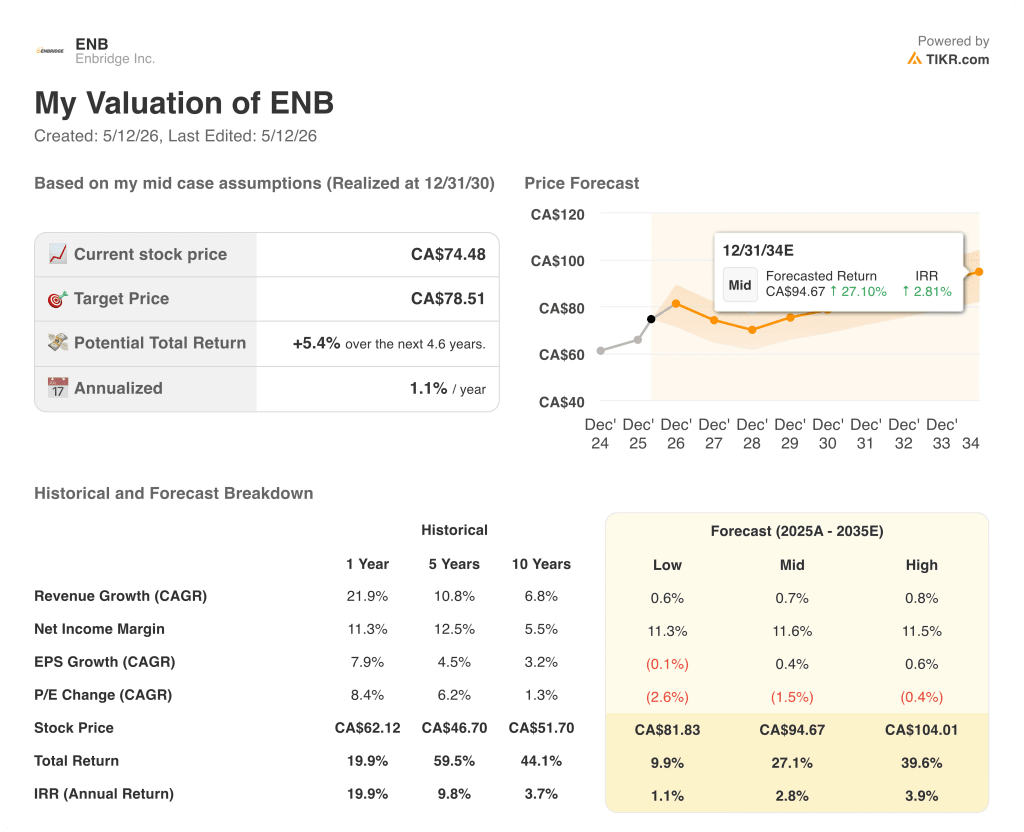

- TIKR Model Price Target: CA$79

- Implied Upside: ~5% total return over ~5 years

Enbridge Q1 2026 Earnings Breakdown

Enbridge stock (ENB) posted Q1 2026 adjusted EPS of $0.98, beating Street estimates of $0.94, while revenue of CA$22,357M came in well above the CA$18,540M consensus.

Record Q1 mainline volumes of 3.2 million barrels per day drove Liquids Pipelines performance, though the segment reported lower contributions year over year due to the absence of a litigation settlement recognized in Q1 2025 and lower Line 9 tolls.

Gas Transmission outperformed on favorable contract settlements and strong storage results, with CFO Pat Murray citing the East Tennessee pipeline reaching a rate case settlement in principle as a specific tailwind, with a FERC filing expected in Q2.

Gas Distribution and Storage grew year over year after new rates took effect in Utah and North Carolina, plus rate escalators in Ontario.

Renewables results came in below Q1 2025 levels due to the absence of investment tax credits tied to the Fox Squirrel solar project, partially offset by strong international wind resources in the quarter.

A CA$0.07 decline in the average CAD/USD exchange rate weighed on all four business units, reducing reported EBITDA, though Enbridge’s realized hedge rate partially offset the FX impact in eliminations.

Management reaffirmed 2026 guidance at the EBITDA and DCF/share midpoints and maintained the post-2026 growth outlook of 5% average annual growth through the end of the decade across EBITDA, DCF/share, and EPS.

CEO Greg Ebel characterized the current period as the best growth environment in energy infrastructure he has seen in 10 to 15 years, pointing specifically to rising natural gas demand, LNG export buildout, and data center power requirements as compounding demand drivers.

Enbridge sanctioned two new projects in Gas Transmission during the quarter: a CA$400M Tres Palacios natural gas storage expansion adding 25 Bcf of Gulf Coast capacity (in-service 2028 to 2030), and a Vector pipeline expansion of just over CA$100M adding 400 million cubic feet per day of westbound capacity (targeted in-service 2028).

In Gas Distribution, the company sanctioned approximately 8 Bcf of unregulated natural gas storage expansion at the Dawn Hub in Ontario, with a 2029 in-service date.

On renewables, Enbridge sanctioned the Cone onshore wind project in Texas with an expected USD $700M investment and a 2027 in-service target, expanding its Meta partnership to over 1 gigawatt of total generation capacity.

The company completed its seventh Ingleside storage expansion in April, bringing total site capacity to approximately 20 million barrels, and brought the Gray Oak pipeline expansion into service at over 1 million barrels per day of operating capacity.

Enbridge disclosed that Gulf Coast crude export interest strengthened materially in April and May, with operating leverage available at Ingleside given existing dock permits and the recently completed storage expansion.

Capital return guidance remained unchanged: Enbridge expects to return CA$40 billion to CA$45 billion to shareholders over the next five years, following CA$38 billion returned over the prior five years.

Management confirmed that the Line 5 Wisconsin relocation project cost is now approaching USD $900M, with approximately USD $600M remaining to be spent, and flagged the project for addition to the secured project listing in Q2 2026.

The $40 billion secured capital backlog extends through 2033, and management disclosed that $17 billion has been added to the sanctioned backlog in the 14 months since the March 2025 Investor Day, with a $50 billion unsanctioned opportunity set that continues to refill.

What Does the Valuation Model Say?

The TIKR model prices Enbridge stock at CA$78.51 against the current CA$74.48, implying total return of approximately 5.4% over 4.6 years, or 1.1% annualized.

The mid-case assumes revenue CAGR of just 0.7% and a net income margin of 11.6% through 2035, with EPS growth CAGR of 0.4% and a P/E contraction of 1.5% annually over the forecast period.

The Q1 results did not materially shift the risk/reward picture: execution was solid, guidance was reaffirmed, and the project pipeline continued to build, but the model’s margin assumptions already embed a fairly muted expansion thesis.

Given the limited implied upside and sub-2% annualized return in the mid case, Enbridge stock presents as a yield and capital-return story more than a price-appreciation opportunity at current levels, with the investment case resting on dividend continuity and backlog conversion rather than multiple expansion.

Enbridge delivered a clean Q1 and reaffirmed guidance, but the stock’s 1.1% annualized model return means the long-term payoff depends almost entirely on whether the $40 billion backlog converts into EBITDA growth that the model has yet to fully price.

What Has to Go Right

- The $40B secured backlog, anchored by projects such as Tres Palacios (CA$400M, in-service 2028 to 2030), Sunrise ($4B, construction beginning summer 2026), and Cone wind (USD $700M, in-service 2027), must execute on schedule to deliver the guided 5% annual EBITDA growth through 2030

- Gulf Coast export demand acceleration following the Strait of Hormuz conflict must sustain into 2027 and pull through incremental Ingleside and Gray Oak utilization

- The Vector open season, which saw customer interest exceed offered capacity for 300 to 500 Mcf per day of additional westbound capacity, must convert to signed contracts and support further expansion FIDs

- Near 50 Bcf of Gulf Coast storage expansion under construction must reach in-service on schedule and capture the rising storage rates management cited on the call

What Could Still Go Wrong

- The TIKR model embeds a P/E contraction of 1.5% annually through 2035, meaning the stock does not rerate even as EBITDA grows, capping price appreciation regardless of operational execution

- The Line 5 Wisconsin relocation, now approaching USD $900M in total cost, remains in active construction through fall 2026 with the Michigan tunnel project still awaiting state and federal permits and no refreshed cost estimate

- FX headwinds reduced reported EBITDA across all four business units in Q1; the CA$0.07 YoY decline in the average CAD/USD rate is a structural drag that partially erodes the value of CAD-denominated backlog for USD-based investors

- Gas Distribution growth in Ontario is slowing by management’s own admission, with the segment redirecting capital to U.S. utilities, where execution and regulatory approval timelines add incremental uncertainty

Should You Invest in Enbridge Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Enbridge Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Enbridge Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ENB stock on TIKR for Free →