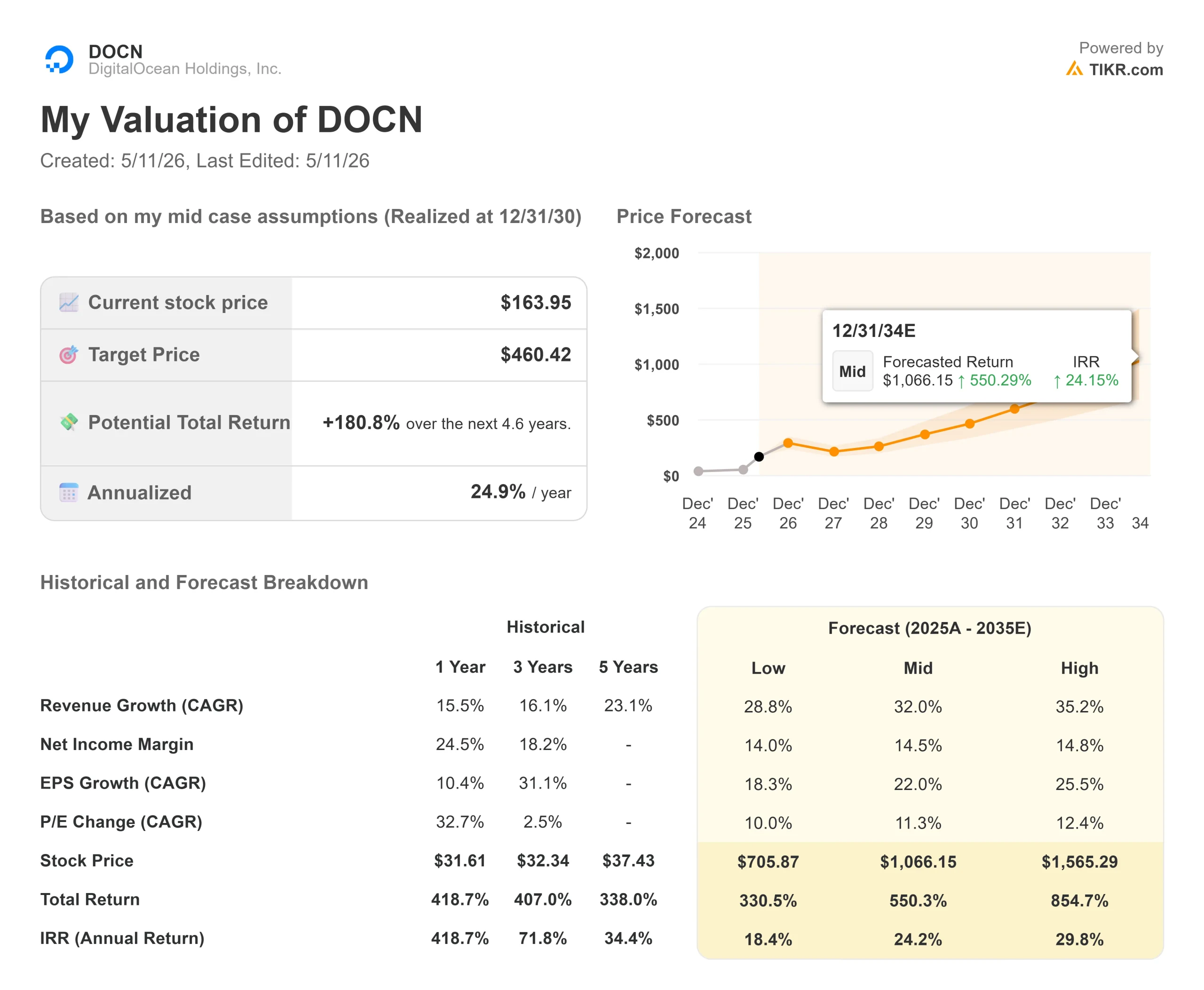

Key Stats for DigitalOcean Stock

- Current Price: $163.95

- Target Price (Mid): ~$460

- Street Target: ~$136

- Potential Total Return (Mid): ~181%

- Annualized IRR: ~25% / year

- Earnings Reaction: +5.38% (May 5, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

DigitalOcean (DOCN) has been one of the sharpest-moving AI infrastructure names of 2026. The stock rose more than 5% on May 5 following a blowout Q1 earnings report, capping a broader rally that had already pushed the stock significantly higher heading into the print. Three catalysts drove the move: the April 28 launch of the DigitalOcean AI-Native Cloud at the company’s Deploy 2026 conference, DigitalOcean’s promotion from the S&P SmallCap 600 to the S&P MidCap 400 effective April 9, and a wave of analyst upgrades from Canaccord, Oppenheimer, BofA, and Barclays.

Bulls argue DigitalOcean has repositioned itself at exactly the right moment, as inference and agentic workloads expand rapidly and neither hyperscalers nor bare-metal GPU providers fully meet the needs of AI-native builders. Bears are watching the valuation, the dilution from the $888 million equity raise, and whether 50% revenue growth in 2027 is locked in or depends on capacity ramp timing and pricing discipline.

What Q1 2026 Said About the Business

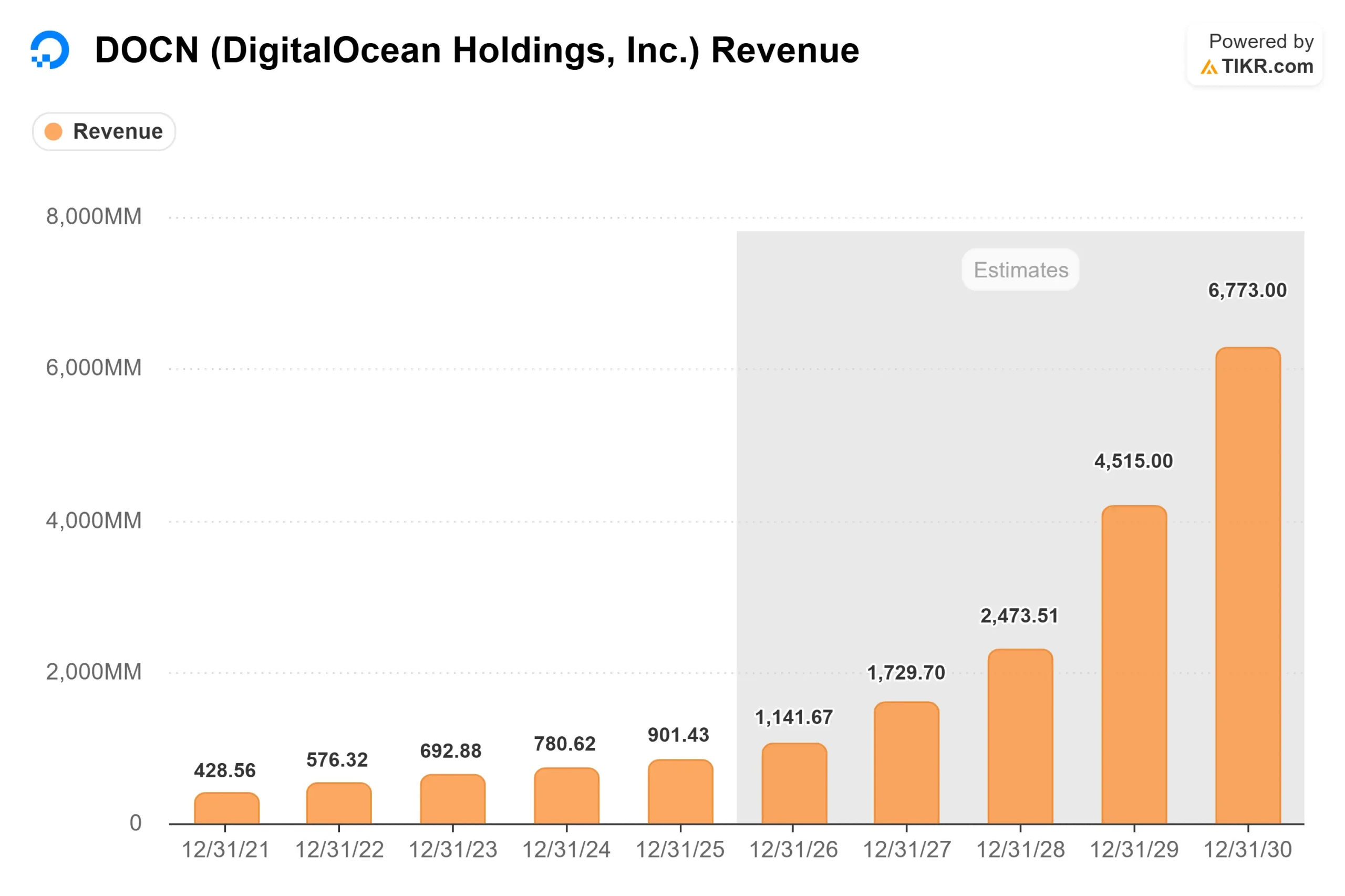

The beat was broad-based. Revenue came in at $257.91 million, up 22% year-over-year, ahead of the $249.76 million consensus. Adjusted EPS of $0.44 beat the $0.26 estimate by approximately 68%, per TIKR data. Adjusted EBITDA was approximately $105 million at a 41% margin.

Critically, none of this came from new capacity. As CFO Matt Steinfort confirmed on the Q1 2026 earnings call: “The Richmond data center, which began ramping revenue in March, contributed less than $500,000 of revenue and less than 20 basis points of year-over-year growth in Q1.” The beat came entirely from the existing business.

The customer data is where the story sharpens. AI customer ARR (annual recurring revenue from customers primarily using AI workloads) hit $170 million, up 221% year-over-year. Customers spending over $1 million annually reached $183 million in ARR, up 179%. The company delivered a record $62 million in incremental organic ARR.

The most striking number was the remaining performance obligations. RPO, meaning contracted future revenue not yet recognized, reached $243 million in Q1 versus $14 million a year ago. That 1,700% increase signals customers are not just spending more with DigitalOcean, they are committing to it on a forward basis.

One detail that matters most for the margin story: inference and core cloud services grew to more than 80% of total AI customer ARR in Q1, up from 70% in Q4, while bare-metal GPU rentals declined in absolute ARR dollars. CEO Paddy Srinivasan said it plainly: “We are not a GPU rental business. We are a full stack cloud platform that AI native companies depend on to build, run and scale their production AI software.” That mix shift toward higher-margin managed services is where the long-term margin story lives.

See historical and forward estimates for DigitalOcean stock (It’s free!) >>>

The AI-Native Cloud Launch: Why It Matters

One week before earnings, DigitalOcean unveiled its AI-Native Cloud at Deploy 2026 in San Francisco. The platform spans five integrated layers: infrastructure, core cloud, inference, data, and managed agents, purpose-built for AI workloads that require both inference (the “thinking”) and autonomous task execution (the “doing”).

The centerpiece is a new Inference Engine with serverless and dedicated endpoints, a catalog of over 70 models with day-zero access, and an intelligent model router from the April acquisition of Katanemo Labs. The router automatically selects the best model for each task based on cost, latency, and availability in real time. A managed agents platform sits at the top of the stack, handling secure sandboxes, state management, and orchestration without locking customers into a single AI provider.

Independent benchmarking firm Artificial Analysis reported that DigitalOcean delivers the number one output speed for leading open-source models, including DeepSeek v3.2 and Qwen v3.5, across all cloud providers. Srinivasan cited 230 output tokens per second on DeepSeek v3.2, described as 3.9 times faster than one leading hyperscaler.

The customer wins validated the strategy in production. Cursor, one of the fastest-growing AI coding tools ever built, is onboarded for production inference, model fine-tuning, and core cloud services. Ideogram migrated production inference from a hyperscaler. Higgsfield AI, serving over 20 million creators, runs its full multi-model video generation workflow on the platform. On Cursor, Steinfort noted: “This is not a bare metal contract. They’re using our inference services. They’ve made commitments around the NFS and some of the core cloud capabilities.” That is platform depth, not just a logo win.

The Capacity Math and the 2027 Case

DigitalOcean now guides to full-year 2026 revenue of $1.13 billion to $1.145 billion, representing 25% to 27% growth, with an exit rate approaching 30% in Q4. For 2027, management projects revenue exceeding $1.7 billion, 50% or more growth, with around 40% adjusted EBITDA margins and high-teens free cash flow margins.

In Q1, DigitalOcean secured approximately 60 megawatts of incremental capacity across four new locations, an 80% increase in its total committed footprint, bringing the total to around 135 megawatts. None of this contributes to 2026 guidance. The 2026 raise is entirely driven by the previously committed 31 megawatts, with the Richmond facility now ramping. The 60 new megawatts begin generating revenue throughout 2027.

To fund this, DigitalOcean raised $888 million through an 11.9 million share follow-on offering. Proceeds first went to repaying the full $500 million Term Loan A, saving roughly $50 million per year in cash interest. The balance sheet now carries no material debt maturities until 2030, with a 2026 exit leverage target of around 3x net debt to EBITDA.

The 2026 free cash flow margin guidance of 9% to 12% includes approximately $100 million in one-time startup costs for the new capacity build-out. Excluding those costs, FCF margins would be 18% to 21% for the year above prior guidance. The cash compression is a deliberate investment decision, not structural margin erosion.

The pricing environment also works in DigitalOcean’s favor. Unlike competitors in multiyear bare-metal contracts, DigitalOcean’s customer agreements typically run three to twelve months. As Srinivasan said on the call: “We can just raise the price on that customer to whatever the current market prevailing prices.” With H100 and H200 GPU pricing still rising, that flexibility is a direct revenue upside lever.

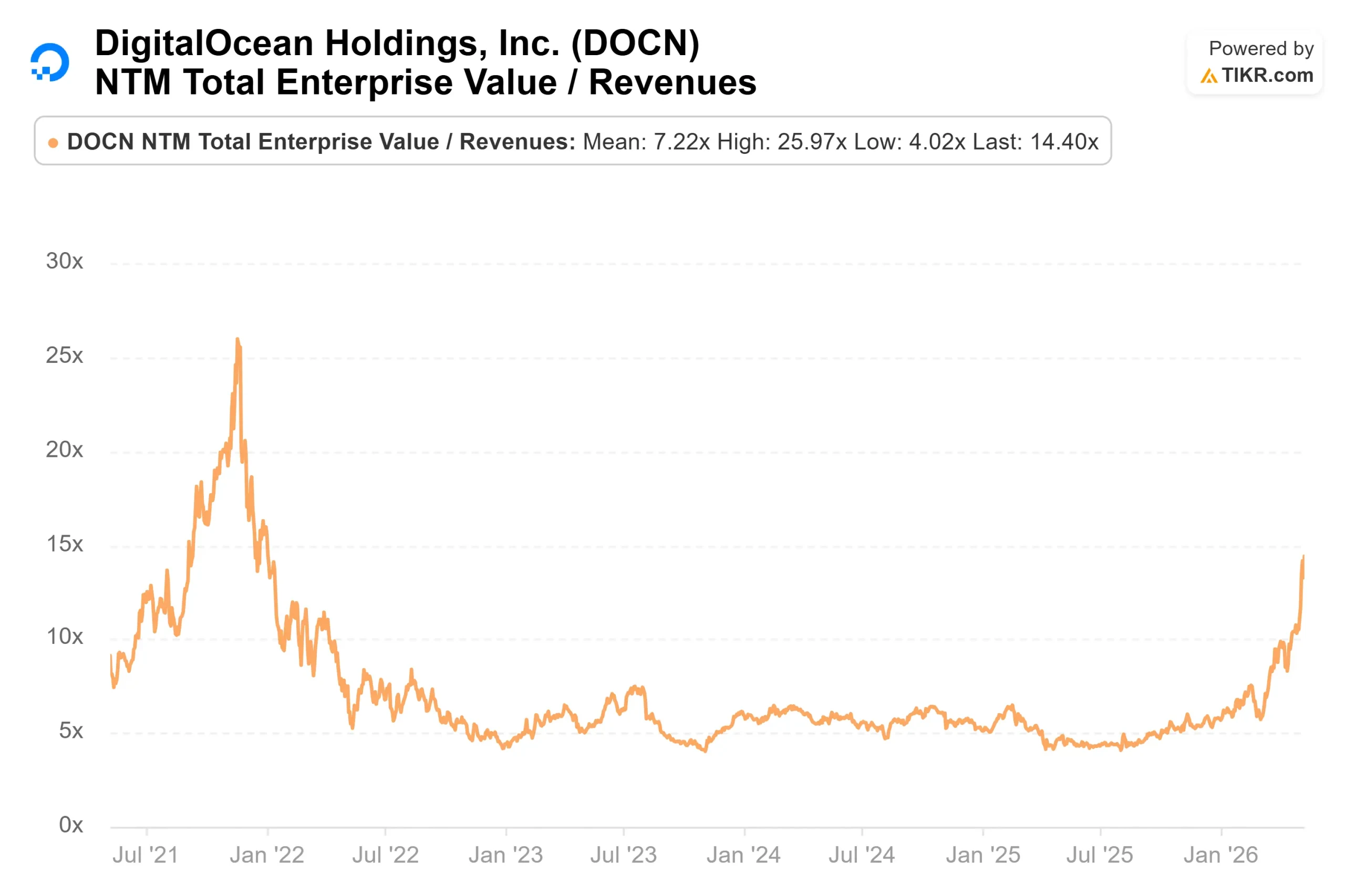

On valuation, DigitalOcean trades at 14.40x NTM EV/Revenue and 37.42x NTM EV/EBITDA, per TIKR data. CoreWeave (CRWV), which focuses primarily on GPU infrastructure for large training clusters, trades at 6.11x NTM EV/Revenue and 10.33x NTM EV/EBITDA. The premium DigitalOcean commands reflect its managed, software-layered platform, though whether it is sustainable depends on whether ARR per megawatt continues to expand as the platform scales.

See how DigitalOcean performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $163.95

- Target Price (Mid): ~$460

- Potential Total Return (Mid): ~181%

- Annualized IRR: ~25% / year

See analysts’ growth forecasts and price targets for DigitalOcean stock (It’s free!) >>>

The TIKR mid-case model assumes a 32% revenue CAGR through 12/31/30, with a net income margin of around 14.5%. Two drivers power that compound annual growth rate: AI customer ARR expanding as inference and agentic workloads compound across the 135-megawatt committed infrastructure pipeline, and ARR-per-megawatt expansion as higher-margin managed services replace lower-margin bare-metal contracts. Both trends are already visible in Q1.

The upside scenario puts the stock at approximately $1,565 at the model’s full 2034 horizon, assuming a 35% revenue CAGR. The downside scenario projects approximately $706 at that same horizon, still above today’s price, but dependent on execution. The primary near-term risk: CapEx per megawatt for the new 60-megawatt tranche is running higher than the prior build, driven by rising component costs and more capable hardware. Management expects equal or better return on invested capital, but that depends on continued pricing strength in AI infrastructure.

One tension worth naming: the Street consensus target of approximately $136 sits below the current price of $163.95. Most analyst targets were set before Q1 earnings. The market is running ahead of sell-side models, pricing in a 2027 that has not yet been delivered.

Conclusion

Watch the AI customer ARR at the Q2 2026 report, expected around early August. The threshold that would confirm Q1 momentum is not decelerating: AI customer ARR above $200 million, with inference and core cloud pull-through holding above 80%. If those hold while Richmond begins contributing more meaningfully, the 2027 guidance shifts from aspirational to structurally credible. DigitalOcean built the full-stack AI-native cloud the inference era demands, and Q1 was the first concrete evidence that AI-native builders are choosing it at scale.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in DigitalOcean?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DigitalOcean, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DigitalOcean alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze DigitalOcean on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!