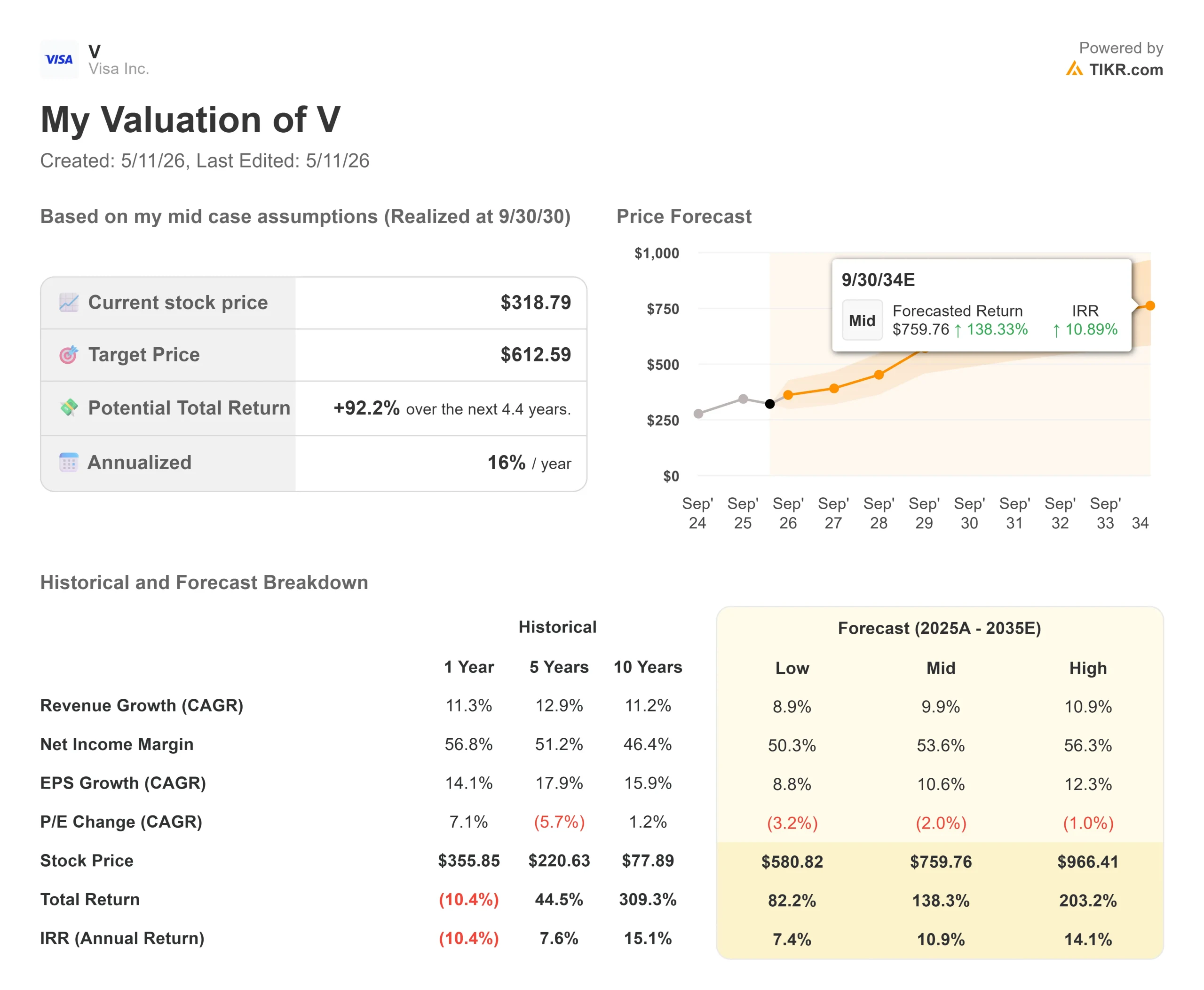

Key Stats for Visa Stock

- Current Price: $322.32

- Street Target: ~$398

- Target Price (Mid): ~$613

- Potential Total Return: ~92%

- Annualized IRR: ~16% / year

- Earnings Reaction: +8.26% (April 28, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Visa (V) stock had spent months wrestling with a stubborn question: can a payments network stay relevant when AI agents, stablecoins, and crypto-native fintechs are actively trying to route around it? The Q2 fiscal 2026 earnings report, released April 28, delivered a decisive answer.

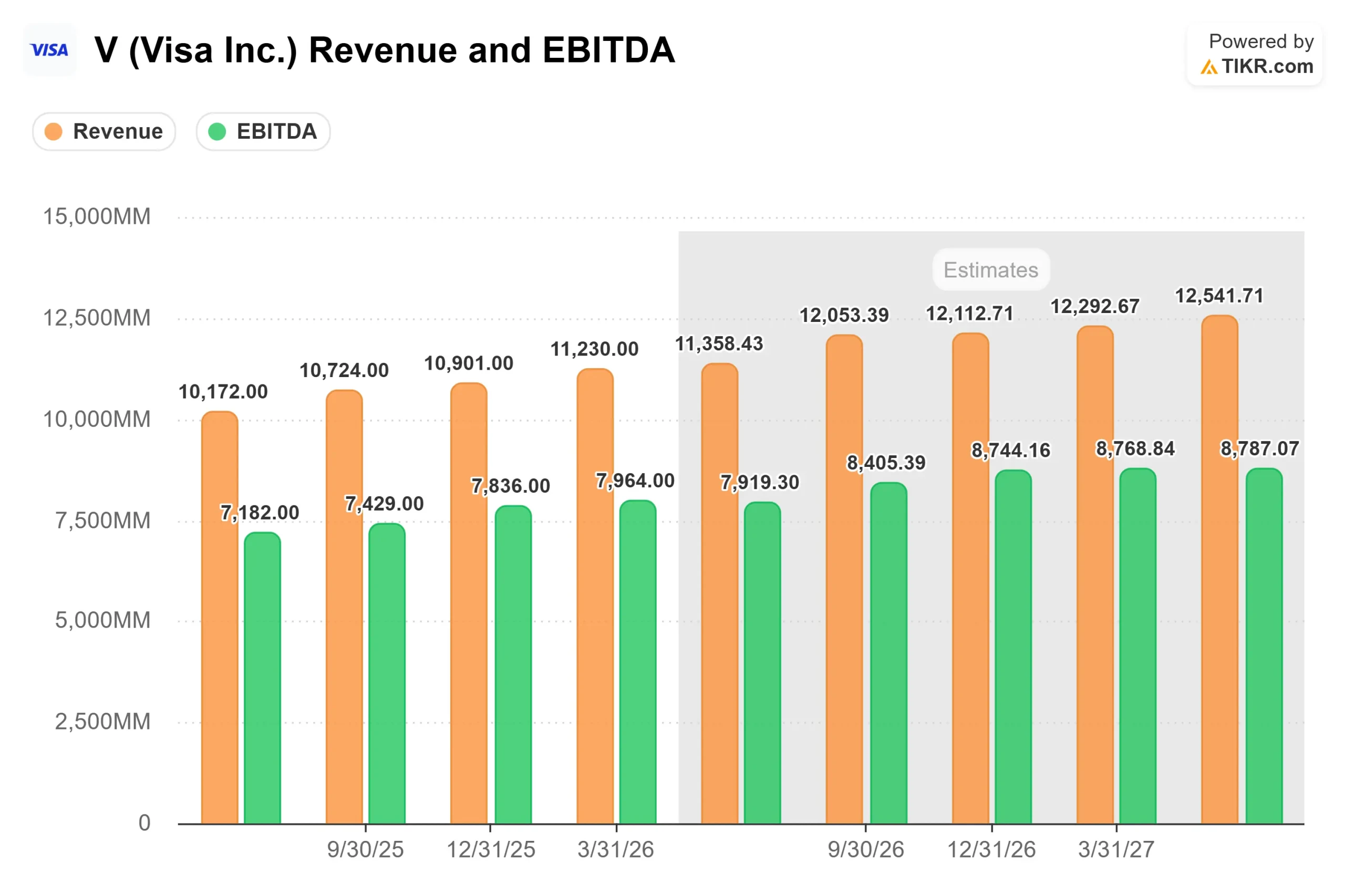

The stock jumped 8.26% on earnings day after Visa reported net revenue of $11.2 billion, up 17% year-over-year its fastest revenue growth since 2022. The result beat analyst estimates by $480 million. CEO Ryan McInerney noted that when excluding the post-pandemic recovery and the Visa Europe acquisition, it was actually the strongest growth since 2013. Adjusted EPS came in at $3.31, topping the $3.10 consensus by $0.21.

Bulls are pointing to value-added services, or VAS, growing 27% in constant dollars, commercial and money movement revenue up 24%, and a record $7.9 billion quarterly buyback. Bears are asking whether the 22.9x forward P/E already prices in the good news, and whether stablecoin challengers will eventually bypass the network entirely. The unresolved question is whether Visa’s push into AI commerce and blockchain is genuine growth or a hedge against its own disruption.

VAS: The Engine the Market Is Still Underpricing

The number that mattered most in Q2 was not payment volume. It was VAS, the suite of fraud tools, data analytics, advisory, and marketing services that now makes up 30% of total net revenue and grew 27% year-over-year in constant dollars to $3.3 billion.

This is not a one-quarter spike. McInerney told analysts on the earnings call that fraud now ranks as a top-three concern for CEOs across Visa’s issuer and merchant base, “something that just wasn’t the case several years ago.” Visa’s answer is the Visa Large Transaction Model, a proprietary AI model trained on its own transaction data that McInerney said can power “up to a 5x increase in fraud value capture.”

Marketing services are the second engine. The FIFA World Cup, with the first match less than 45 days away as of the earnings call, is already delivering. CFO Chris Suh described one Latin American client campaign that drove a 10% lift in active cards in just over three months and generated $10 million in VAS revenue for Visa. “There’s a good flywheel at work,” Suh said. “As our clients continue to grow faster, they continue to drive volumes and drive spend back to Visa.”

The structural point: as McInerney noted, the vast majority of VAS revenue is “linked to transactions, cards and accounts.” It is not a standalone business that can be disrupted away from the core network. It compounds with every AI capability layered on top.

See historical and forward estimates for Visa stock (It’s free!) >>>

Stablecoins and Agents: Threat or Tailwind?

The bear case is playing out publicly. Fortune reported this week that challengers, including MoonPay, Stripe, and Coinbase, believe that on-chain settlement, which can cost a fraction of Visa’s roughly 12 basis point network fee, will eventually make card rails obsolete. Y Combinator co-founder Paul Graham put it bluntly: why drag Visa “like a software virus” into an agentic future?

Visa’s answer, laid out in detail on the earnings call, is that it is not competing with stablecoins; it is becoming the bridge between them and the real world. The company already has over 160 stablecoin card programs globally with partners including Rain, Reap, and Bridge. Stablecoin-linked card payment volume was up nearly 200% year-over-year in Q2. Visa has added five new blockchains, Arc, Base, Canton, Polygon, and Tempo, bringing its stablecoin settlement infrastructure to nine chains, with a $7 billion annual run rate growing more than 50% quarter-over-quarter. Visa is also a validator on Tempo and a super validator on Canton, meaning it helps govern the settlement network itself.

On agentic commerce, Visa launched Intelligent Commerce Connect as an on-ramp for AI agent builders, then expanded its Agentic Ready Program to Canadian issuers on May 5, following rollouts across Asia-Pacific and Latin America. The thesis is simple: when consumers hand off spending decisions to AI agents, they default to payment methods they trust. “I think the limiting factor for agentic commerce is trust,” McInerney said.

When an analyst pushed directly on whether stablecoin and agentic transactions are accretive or dilutive, McInerney was direct: they have economics that “look just like our normal products.” What changes is volume, not the revenue model. That is the key claim the market has not yet fully priced in.

Valuation: A Discount the Market Is Not Pricing In

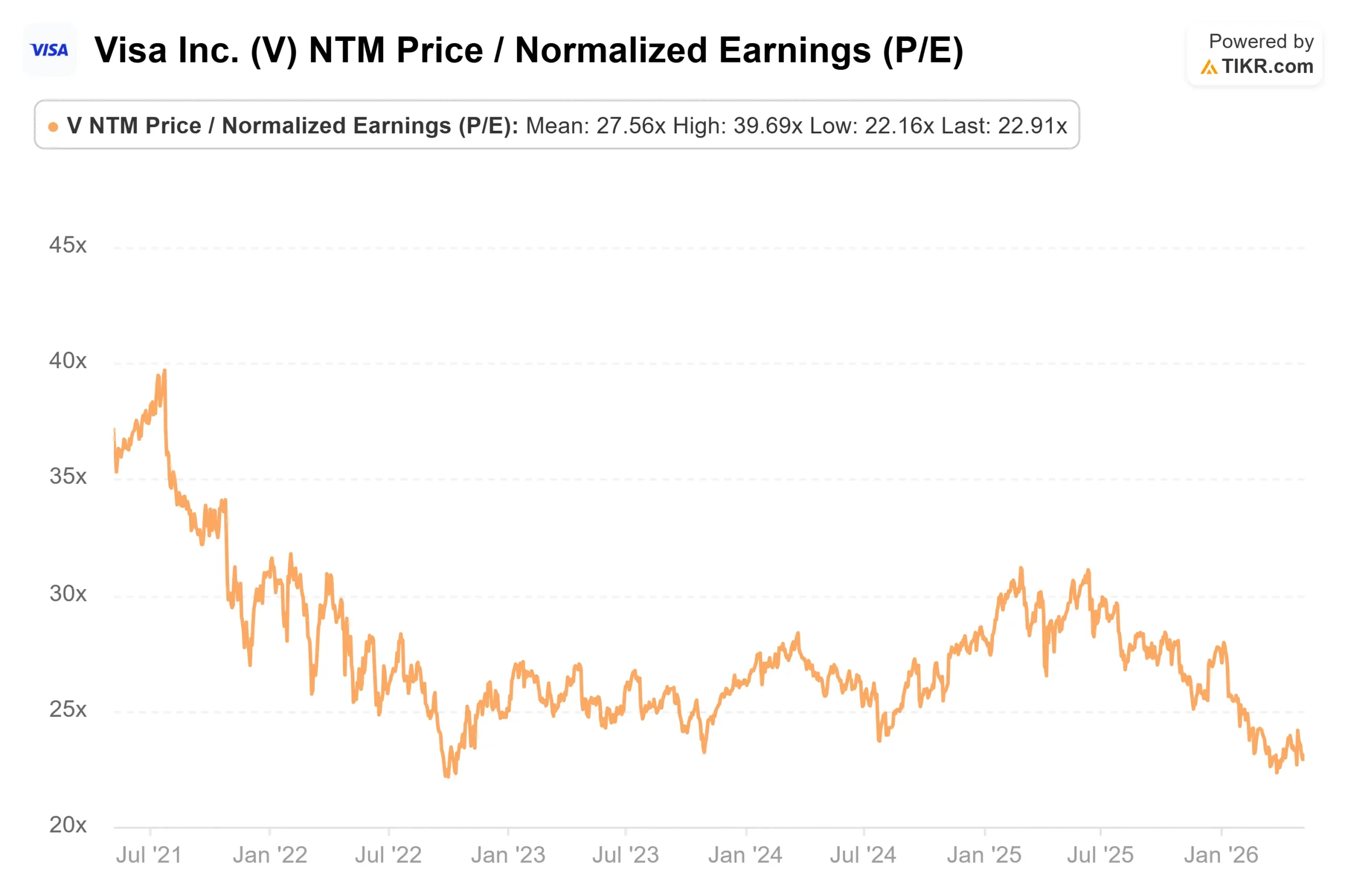

Visa trades at 22.9x NTM earnings per TIKR. Mastercard, running the same asset-light model without issuing cards or carrying credit risk, trades at roughly 25.9x forward earnings according to StockAnalysis. Neither Visa’s stablecoin strategy nor its agentic commerce build appears to be priced in at current levels. That is either a margin of safety or evidence that the market is right to wait.

Morgan Stanley raised its price target to $415 after the quarter, calling the network “near-undisruptible” and applying 27x P/E to its CY27 EPS estimate. That framing implies the current price needs no credit for stablecoins, agentic commerce, or Pismo, the cloud-native core banking platform that Visa acquired and which signed Wells Fargo as a client this quarter.

The capital return picture adds a floor. The $7.9 billion Q2 buyback was the largest in Visa’s history. The board authorized a new $20 billion program in April on top of $13 billion already remaining, putting total buyback capacity at approximately $33 billion. With LTM free cash flow at approximately $22.4 billion per TIKR, the buyback is essentially self-funded from operating cash.

The 35-analyst Street consensus sits at ~$398: 28 Buys, 7 Outperforms, 3 Holds, 2 Underperforms, 0 Sells per TIKR.

One risk deserves naming directly. Visa’s CEMEA region, roughly 6% of total payment volume, saw a 2.5-point deceleration in constant-dollar growth in Q2 due to the Middle East conflict. Suh said that, normalizing for Ramadan timing, April cross-border volumes ran in line with February. A broader escalation would weigh on cross-border for the rest of fiscal 2026.

See how Visa performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $322.32

- Target Price (Mid): ~$613

- Potential Total Return: ~92%

- Annualized IRR: ~16% / year

See analysts’ growth forecasts and price targets for Visa stock (It’s free!) >>>

The TIKR mid-case model, realized at 9/30/30, targets around $613, implying roughly 92% total return. Two factors drive the revenue CAGR of around 10%: sustained cross-border volume expansion and continued VAS compounding. The net income margin assumption is around 54%, consistent with Visa’s ability to grow services without degrading overall profitability.

The high case reaches around $966 with a revenue CAGR of around 11% and margins near 56%. The low case lands at around $581 with around 7% annualized returns, if growth moderates to around 9% and margins compress modestly.

The primary risk is structural: if stablecoin rails scale in a way that routes commerce entirely around Visa’s network, the revenue growth assumptions break. That is the Fortune bear case. Neither the TIKR model nor the Street consensus prices it in.

Conclusion

Watch VAS revenue growth in Visa’s fiscal Q3 2026 earnings, expected in late July. If it holds above 20% in constant dollars despite tougher Olympics comparables, the flywheel is structural. Management guided for Q3 net revenue growth in the low double digits, a bar that holds only if consumer spending stays stable and the Middle East situation remains contained.

Visa is the payments network that keeps finding new reasons to grow. The Q2 2026 result was the strongest argument yet that stablecoins and AI agents are more likely to run on Visa’s rails than around them.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Visa?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Visa, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Visa alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!