Key Stats for Roku Stock

- 52-Week Range: $53.73 to $142.00

- Current Price: $129.53

- TIKR Target Price (Mid): ~$268

- TIKR Annualized IRR (Mid): ~17% per year

- Q1 2026 Revenue: $1.25 billion, up 22%

- Q1 2026 EPS: $0.57 (versus -$0.19 a year ago)

- Q1 2026 Adjusted EBITDA: $148 million, up 165%

- Streaming Households: 100 million+

Value your favorite stocks like Roku with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

A Milestone Quarter That Changes the Narrative

Roku’s (ROKU) business model has always been straightforward to understand and difficult to trust. Sell the hardware at or below cost, build the installed base, then monetize through advertising and platform subscriptions. The first two parts of that equation worked from day one. The third part took years longer than investors wanted to wait, and the stock spent much of 2022 through 2024 reflecting that impatience.

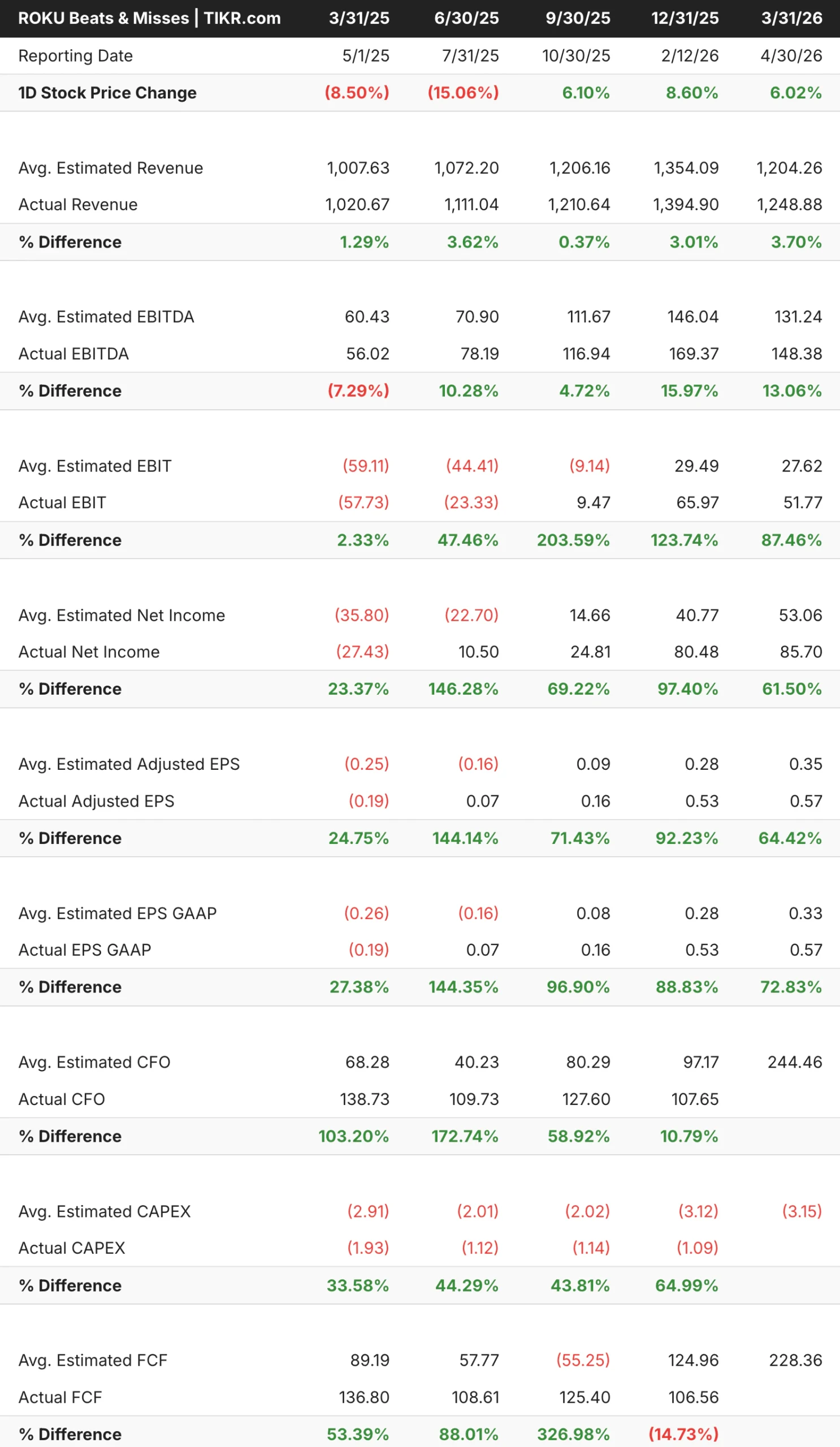

The Q1 2026 results are the clearest evidence yet that the monetization is arriving at scale. Revenue grew 22% to $1.25 billion, beating consensus by around $45 million. EPS of $0.57 obliterated the $0.35 estimate. Adjusted EBITDA surged 165% year over year to $148 million, above its own guidance of $130 million. And the company turned a $27 million net loss a year ago into $86 million in net income. Roku now reaches over 100 million streaming households globally, a scale that makes the advertising business structurally defensible.

The beats and misses table shows something important about where this business is in its development. Revenue has beaten modestly and consistently, by 1%-4%, for five consecutive quarters. The profitability beats are where the story is. Net income has beaten by 24%, 146%, 69%, 97%, and 61% in those same five quarters, in that order. That acceleration is not noise. It reflects a business whose operating leverage is compounding quarter after quarter as platform revenue grows faster than costs.

See analysts’ growth forecasts and price targets for ROKU (It’s free) >>>

The Gross Margin Chart Needs Context

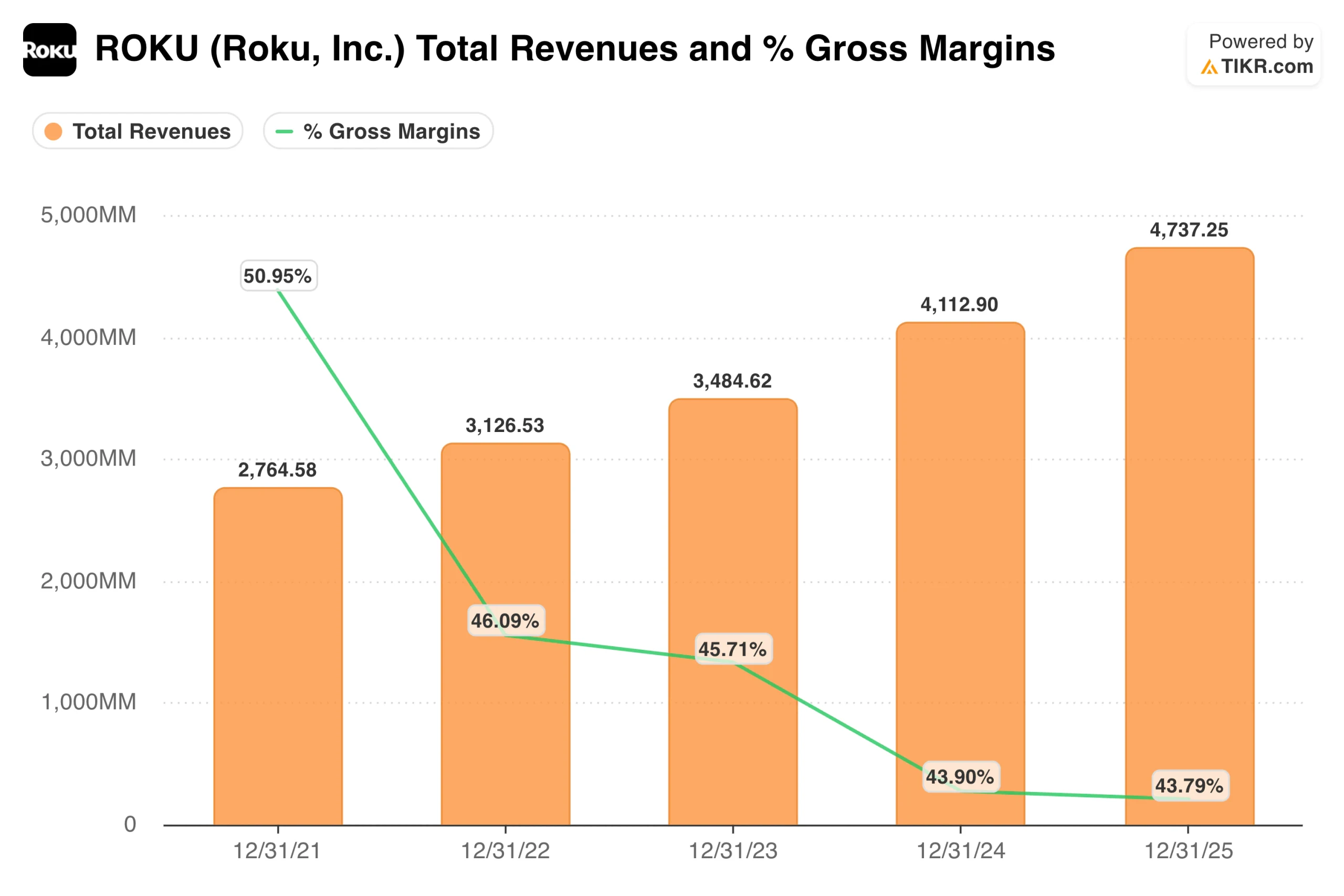

At first glance, the revenue and gross margin chart looks like a business with deteriorating economics. Gross margins declined from about 51% in 2021 to around 44% in 2024 and 2025, even as revenue grew from $2.8 billion to $4.7 billion. That looks like the kind of margin compression that warrants concern.

The context that changes the interpretation is the device segment. Roku sells hardware at or near cost, sometimes below it, as a deliberate strategy to grow the installed base. Devices carry negative or near-zero gross margins, and as Roku scaled its hardware business in 2022 and 2023, those low-margin sales pulled the blended gross margin down even as platform economics improved. Platform gross margins run around 52%.

In Q1 2026, device revenue fell 16% year over year while platform revenue grew 28%. That mix shift is exactly what the thesis requires, and it is why total gross profit grew 27% even as the headline gross margin percentage looks flat. The full-year picture will start to show this improvement more clearly as the platform becomes a larger share of a larger revenue base. Roku guided full-year platform revenue to $5 billion, up 21%, against devices revenue of roughly $535 million.

Value Roku instantly (Free with TIKR) >>>

107% Upside in the Mid Case, Built on a Platform Still in Early Innings

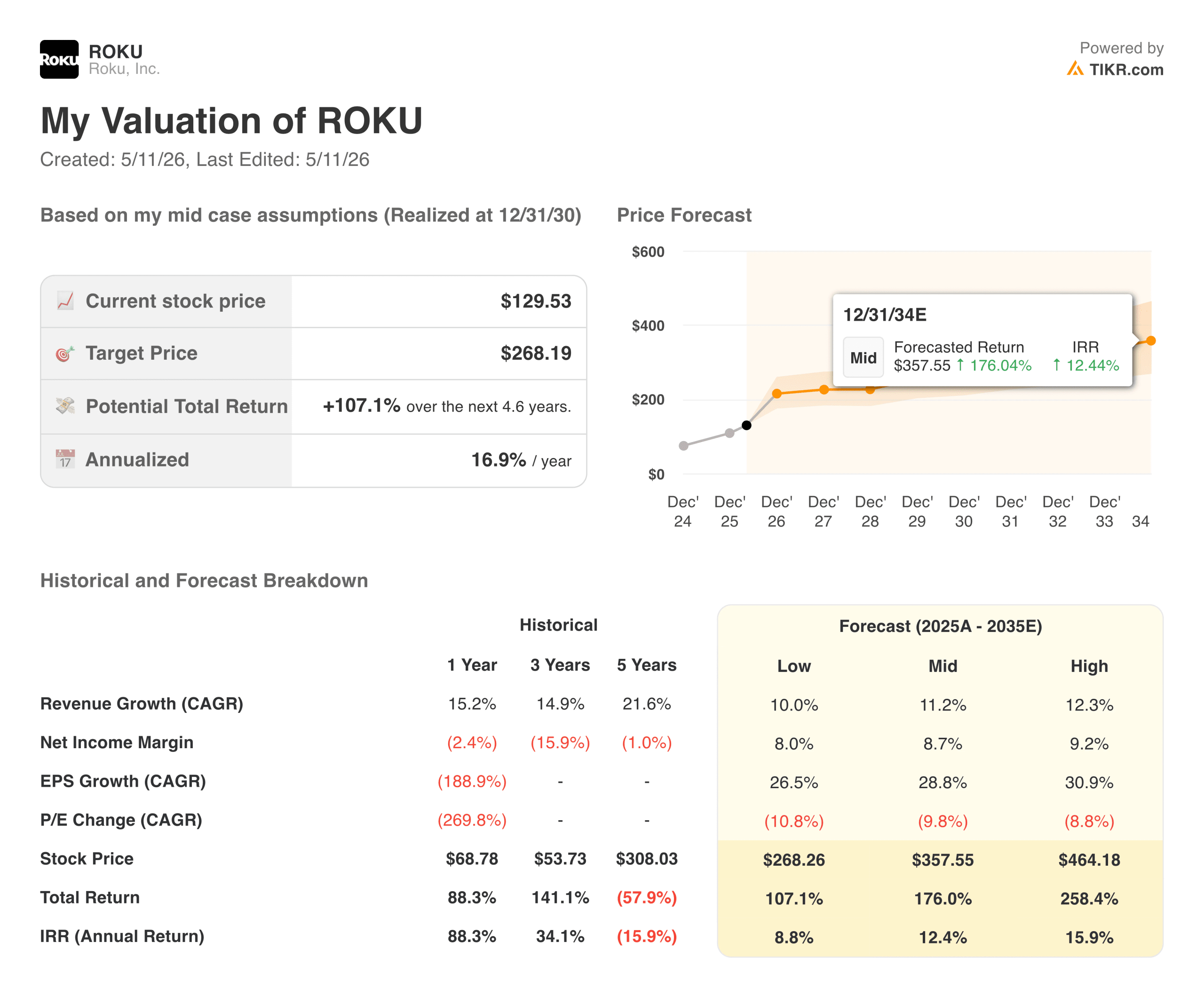

TIKR’s model targets around $268 in the mid-case, implying a total return of roughly 107% over about 4.6 years, or about 17% annualized. The model assumes revenue growth of around 11% annually and net income margins expanding toward 9%. Given that margins were deeply negative as recently as 2024, those forward assumptions require real execution, but the trajectory over the past four quarters suggests the business is ahead of schedule.

CEO Anthony Wood has said Roku expects to reach $1 billion in annual free cash flow by 2028, and potentially sooner. FCF for the trailing twelve months already stands at $539 million.

What the Bulls Are Counting On

- The CTV advertising market is structurally growing, and Roku is taking share. Connected TV ad spend through third-party programmatic partners grew more than 40% year over year in Q1, driven by deeper integrations with Google DV360, Amazon DSP, The Trade Desk, Yahoo, and FreeWheel. Non-media and entertainment brands reached nearly 30% of Roku Experience ad revenue, an all-time high, reflecting genuine diversification beyond the entertainment advertisers who were the early adopters. Roku is the number one TV streaming platform by hours streamed in the US, Canada, and Mexico, which gives it a scale advantage that compounds with each new household added.

- The subscription business is a durable and growing revenue layer. Subscriptions grew 30% to $519 million in Q1, driven by price increases from streaming partners and record new premium subscription sign-ups. Unlike advertising revenue, subscription revenue does not fluctuate with the ad market cycle, giving the platform a more stable earnings base than a pure advertising business would have.

- Operating leverage is just beginning to show up. EBITDA margins in 2021 were deeply negative. They are now in double digits and accelerating. As platform revenue compounds and device losses shrink, the incremental revenue is flowing to the bottom line at an unusually high rate. The EBITDA CAGR over the next two years is expected to be around 40%, well above revenue growth, reflecting operating leverage as the business crosses its fixed cost base.

- 100 million households is a network effect, not just a scale metric. Every new household added to the Roku ecosystem creates more advertising inventory, more first-party data for targeting, and more leverage in content distribution negotiations. That flywheel gets stronger as the installed base grows, and at 100 million households, Roku is reaching a scale where meaningful advertiser budget commitments become rational.

What the Bears Are Watching

- The valuation requires sustained execution over multiple years. At around $130 per share, Roku is priced at a significant multiple of current earnings and requires the platform’s growth trajectory to hold through 2026 and beyond. Any quarter in which advertising growth slows meaningfully, whether due to a macro downturn or share loss to competitors, will quickly reset expectations, given how much forward growth is embedded in the price.

- The gross margin story is not straightforward. The blended margin has been declining for four years and the recovery depends on devices shrinking as a proportion of revenue. If Roku decides to reinvest in hardware to grow households faster, it could delay the margin improvement that the model is counting on.

- Stock-based compensation is a real dilution risk. Roku has historically been an aggressive issuer of stock-based compensation, which does not show up in adjusted EBITDA but absolutely affects shareholders. Any investor evaluating the EBITDA story should look at the GAAP earnings alongside it to understand the true cost of the platform’s growth.

Should You Invest in Roku

The investment case for Roku has shifted meaningfully over the past twelve months. A year ago, it was a show-me story requiring proof of profitability. Today, that proof has arrived in four consecutive quarters of accelerating beats, a clear path to $1 billion in free cash flow, and a platform reaching the scale where advertising economics become genuinely compelling.

The gross margin chart is the one piece of the story that requires patience and context rather than straightforward optimism. The underlying platform economics are strong, but they are obscured by the device business in the annual numbers. Watching the quarterly gross margin trend over the next two to three quarters will tell you whether the mix shift is accelerating on schedule. If it is, the TIKR mid-case target of around $268 against a current price of around $130 will look conservative rather than ambitious.

See analysts’ growth forecasts and price targets for Roku stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!