Key Stats for CrowdStrike Stock

- 52-Week Range: $189.27 to $429.44 (pre-split adjusted)

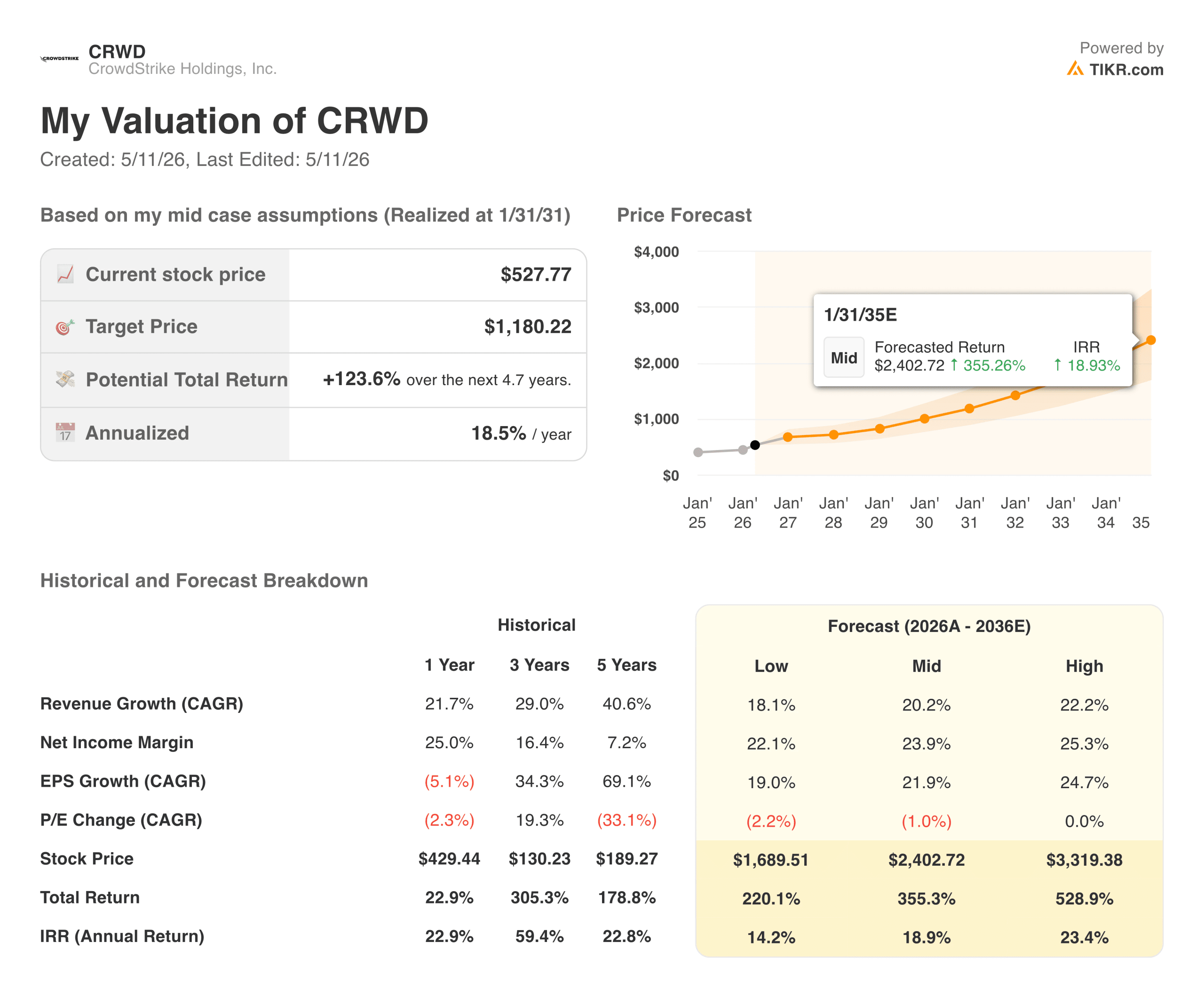

- Current Price: $527.77

- TIKR Target Price (Mid): ~$1,180

- TIKR Annualized IRR (Mid): ~18.5% per year

- FY2026 Ending ARR: $5.25 billion, up 24%

- FY2026 Net New ARR: $1.01 billion (first time exceeding $1 billion)

- Falcon Flex ARR: $1.69 billion, up over 120%

- FY2026 Non-GAAP EPS: $4.11

Value your favorite stocks like CRWD with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

A Year That Answered Every Question From the Outage

When CrowdStrike’s (CRWD) faulty software update triggered a global IT outage in July 2024, taking down millions of Windows machines and causing billions in economic damage across airlines, hospitals, and enterprises, the central question for investors was not whether the company would survive. It was whether customers would stay, and whether growth would recover before the damage became structural.

FY2026 ended January 31st and provided the answer in full. Net new ARR grew 47% year over year in Q4 alone, reaching $331 million. For the full year, net new ARR hit $1.01 billion, the first time CrowdStrike has crossed that threshold.

Ending ARR reached $5.25 billion, growing 24% and making CrowdStrike the fastest pure-play cybersecurity company to reach that milestone. Gross retention held at 97% throughout the recovery period. CEO George Kurtz called it the company’s best year yet, and the numbers support that framing.

The Falcon Flex subscription model, which lets enterprises flexibly expand their module usage rather than commit to fixed bundles, was central to the recovery. Flex ARR grew by over 120% year over year and now accounts for roughly $1.69 billion of the total base.

That model creates larger initial commitments and makes it structurally harder for customers to leave, because the more modules they adopt, the more deeply the platform is embedded in their security architecture.

See analysts’ growth forecasts and price targets for CRWD stock (It’s free!) >>>

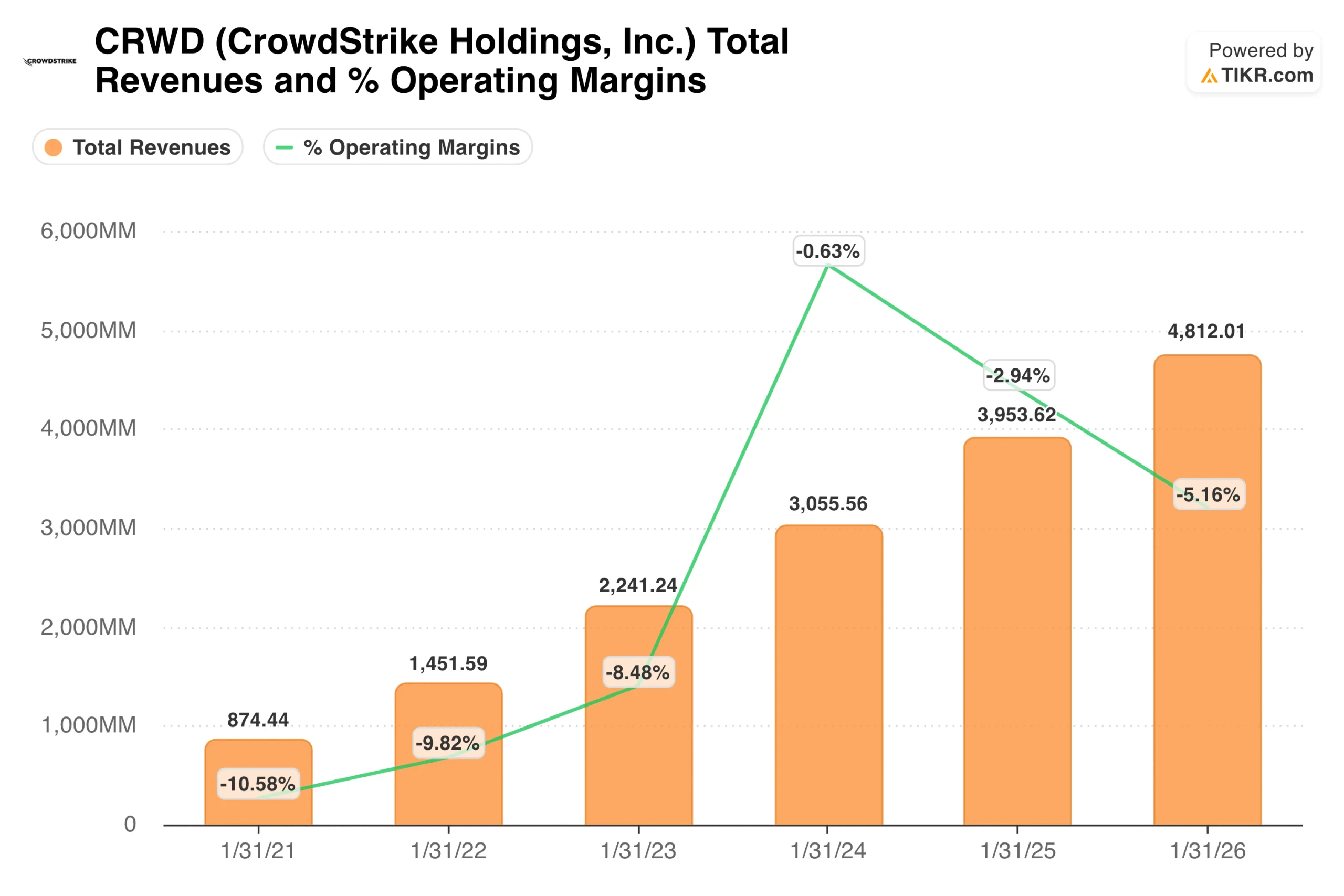

What the Revenue and Margin Chart Actually Shows

The revenue trajectory on this chart is one of the cleanest growth stories in enterprise software. CrowdStrike grew from $874 million in FY2021 to $4.8 billion in FY2026, compounding at over 40% annually for five years while maintaining subscription gross margins above 78%.

The operating margin line requires context before drawing conclusions from it. These are GAAP margins, which include significant stock-based compensation, and SBC at a fast-growing software company of this scale is not trivial. The apparent regression from -0.6% in FY2024 toward -5% in FY2026 does not reflect deteriorating unit economics.

It reflects the post-outage period, during which CrowdStrike offered customer commitment packages and invested heavily in product reliability and enterprise relationships, temporarily increasing operating expenses.

Non-GAAP operating margins, which strip out SBC and acquisition-related charges, ran around 22% for FY2026, and management has guided toward continued expansion. The GAAP picture will normalize as SBC moderates relative to revenue and the commitment packages roll off.

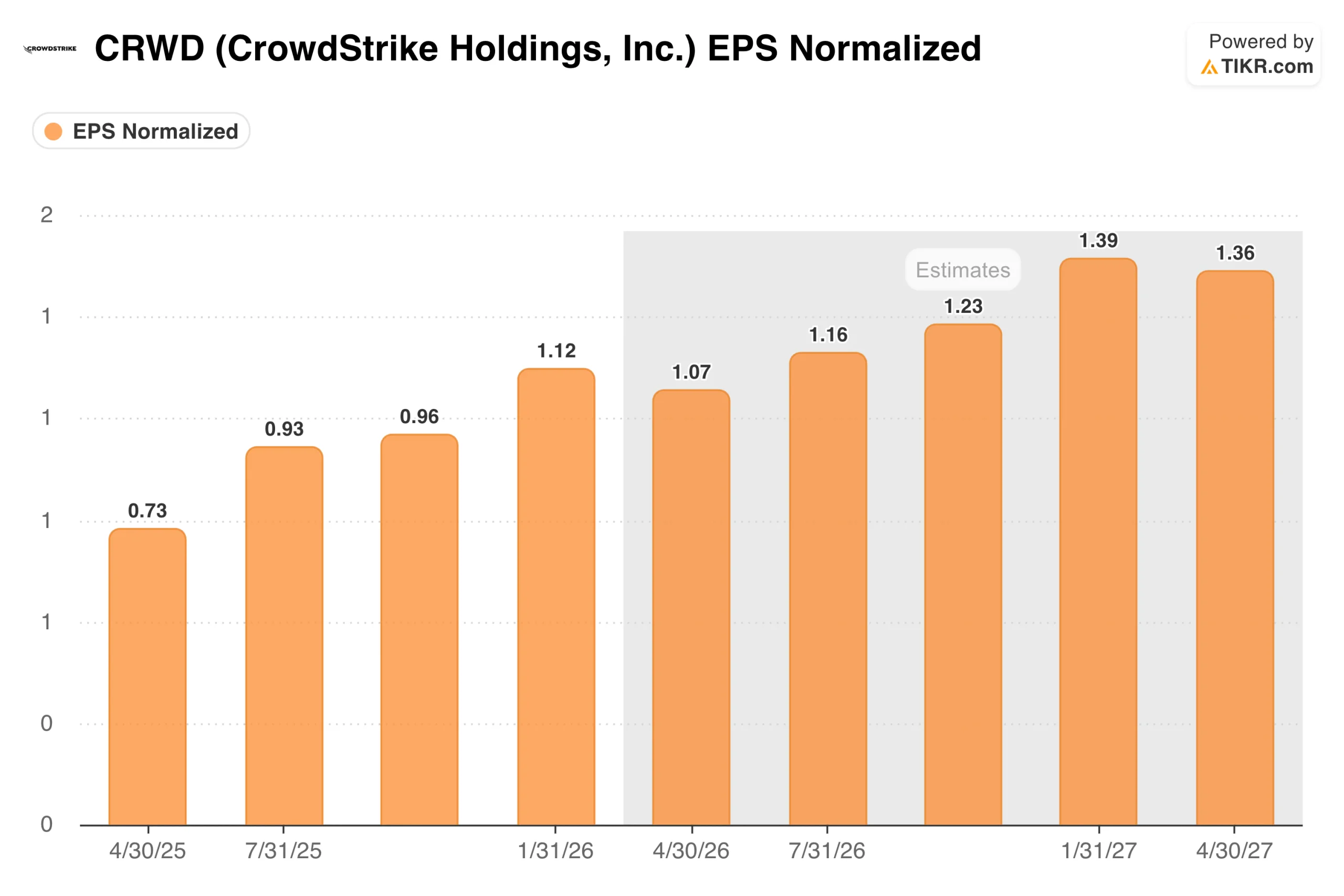

A Business Earning Real Money, Quarter After Quarter

The EPS chart shows the non-GAAP earnings trajectory that the revenue and margin chart cannot fully capture. Normalized EPS grew from $0.73 in Q1 FY2026 to $1.12 in Q4, a 53% increase over four quarters. Analysts model continued quarterly growth through FY2027, with Q4 FY2027 consensus around $1.39.

That kind of EPS compounding on a $5 billion ARR base is what makes the TIKR model’s return assumptions credible rather than optimistic. The earnings base is real, the growth rate is real, and the platform retention data suggest the revenue is sticky. CrowdStrike achieved positive GAAP net income in Q4 FY2026, marking the first time in the company’s history and removing one of the remaining objections institutional investors had about the business model.

Value CRWD instantly (Free with TIKR) >>>

124% Upside in the Mid Case on a Thesis Built Around Consolidation

TIKR’s model targets around $1,180 in the mid case, implying a total return of roughly 124% over about 4.7 years, or about 18.5% annualized. The model assumes around 20% annual revenue growth and net income margins expanding toward 24%. Both assumptions require CrowdStrike to keep doing what it has been doing, not to do something it has not yet demonstrated.

The central thesis is that enterprise security is consolidating onto fewer, broader platforms, and CrowdStrike is one of the two or three platforms large enough to absorb that consolidation at scale. The Falcon platform now covers endpoints, cloud workloads, identity, next-gen SIEM, and exposure management.

As AI creates new attack surfaces and compliance requirements, the addressable market grows alongside it. Kurtz has articulated a path toward $10 billion in ending ARR, which would roughly double the current base.

What the Bulls Are Counting On

- Platform consolidation is a multi-year structural tailwind. Enterprises are reducing the number of security vendors they work with, consolidating onto integrated platforms that can share telemetry and respond across surfaces simultaneously. CrowdStrike’s module adoption data tells this story clearly. As of Q3 FY2026, 49% of customers had adopted six or more modules, 34% had adopted seven or more, and 24% had adopted eight or more. Customers who adopt more modules are harder to displace and spend more over time.

- The outage recovery proved the platform is genuinely mission-critical. The fact that 97% gross retention held through the most embarrassing product failure in company history is more informative about customer dependency than any marketing claim could be. Enterprises did not leave because they could not afford to. That stickiness is the real moat, and it is now proven under the most adversarial conditions imaginable.

- AI creates more attack surface, which means more demand. Every AI workload, every autonomous agent, every new data pipeline is a new vector for adversaries. CrowdStrike has positioned Falcon as the security layer for AI infrastructure, specifically, with Falcon AI Detection and Response launched in Q4 FY2026. As enterprises deploy AI at scale, they need to secure it, and CrowdStrike is building the products to capture that spending before it goes elsewhere.

- Falcon Flex is changing the deal economics. Flex customers commit to larger initial ARR and expand their module usage over time, creating a compounding revenue base that grows independently of new logo acquisition. With Flex ARR up over 120% and representing a growing share of the total base, the business is shifting toward a model in which existing customers drive a larger share of growth each year.

What the Bears Are Watching

- The valuation is demanding even against strong growth. At around $528 per share, CrowdStrike trades at roughly 100 times forward non-GAAP earnings. The mid-case return of 18.5% annualized is compelling, but it requires the growth rate to hold and the model’s multiple compression to be manageable. Any material deceleration in net new ARR would compress the multiple quickly, given how much future growth is embedded in the current price.

- The GAAP operating margin picture remains negative and is getting worse. Investors who focus on GAAP metrics will see operating margins going the wrong direction even as revenue compounds at 20%. The non-GAAP story is better, but the gap between GAAP and non-GAAP at this scale is worth monitoring carefully, particularly around SBC as a percentage of revenue.

- Competition from Palo Alto Networks is intensifying. Palo Alto has been aggressively pursuing its own consolidation strategy, offering platformization deals that bundle capabilities at discounted rates to displace point solutions. The two companies are competing for the same enterprise security consolidation opportunity, and the outcome of that competition will shape both of their long-term trajectories.

Should You Invest in CrowdStrike

CrowdStrike is one of the most straightforward long-term cases in enterprise software right now: a platform business with 97% retention, expanding module adoption, growing ARR, and a newly profitable earnings base competing in a market that grows every time a new technology wave creates new attack surfaces.

The honest caveat is that the stock prices in a lot of that future. At around $528, you are paying for years of compounding ahead of time, and the model’s 18.5% annualized return in the mid-case requires execution against revenue growth targets that are ambitious even for a business with CrowdStrike’s track record.

The next key milestone to watch is FY2027 Q1 earnings, where the net new ARR trajectory will indicate whether the Falcon Flex momentum from FY2026 carries into the new fiscal year or growth begins to normalize after the elevated recovery pace.

See analysts’ growth forecasts and price targets for CRWD stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!