Key Stats

- Current Price: ~$296 (May 11, 2026)

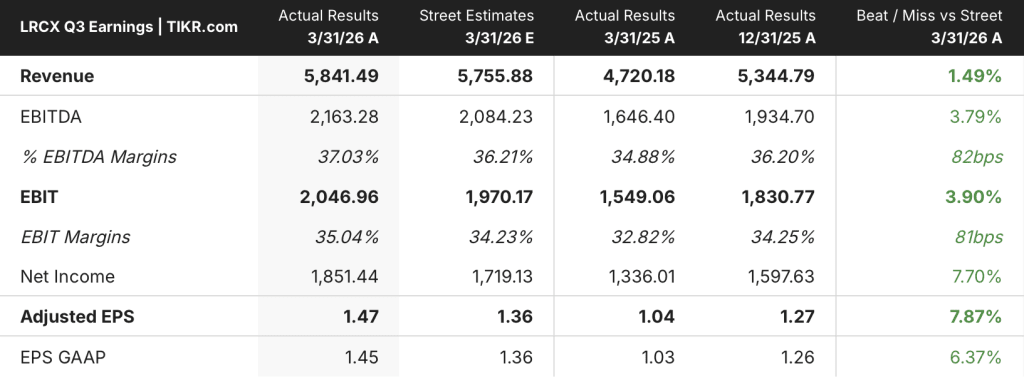

- Q3 FY2026 Revenue: $5.84B, up 24% YoY

- Q3 FY2026 Adjusted EPS: $1.47, up 41% YoY (record; above guidance high end)

- Q4 FY2026 Revenue Guidance: $6.6B (+/-$400M)

- Q4 FY2026 EPS Guidance: $1.65 (+/-$0.15) — record

- Q4 FY2026 Gross Margin Guidance: 50.5% (+/-1pp)

- Q4 FY2026 Operating Margin Guidance: 36.5% (+/-1pp)

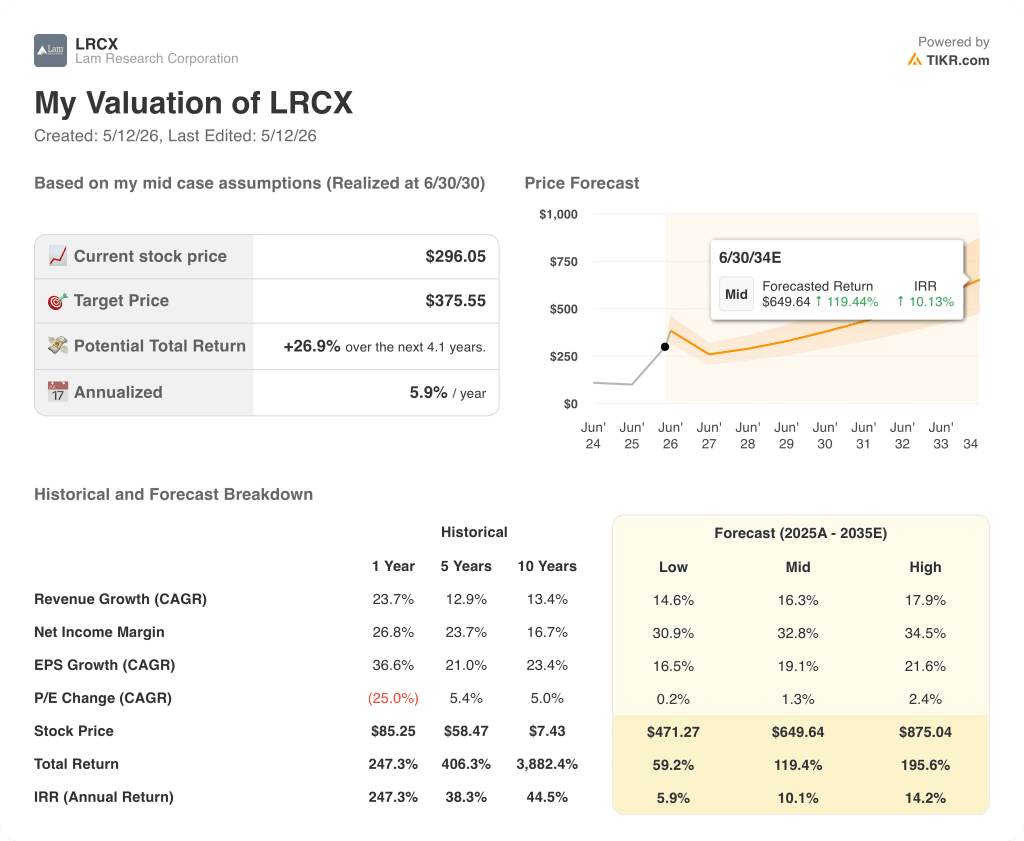

- TIKR Model Price Target: ~$376

- Implied Upside: ~27%

Lam Research Stock Posts Record Quarter as AI Drives Accelerating Equipment Demand

Lam Research stock (LRCX) delivered $5.84B in revenue for Q3 FY2026, up 24% year-over-year and representing the company’s third consecutive record revenue quarter, with adjusted EPS of $1.47 beating the top end of guided range.

The Customer Support Business Group was the headline driver, crossing $2B in quarterly revenue for the first time in company history, according to CFO Doug Bettinger on the Q3 2026 earnings call.

CSBG generated $2.11B in revenue, up 6% sequentially and 25% year-over-year, fueled by high industry utilization rates driving spares and services demand.

Foundry accounted for 54% of systems revenue, with revenue in dollar terms approximately flat sequentially but up 35% year-over-year, as leading-edge investments and mature node spending ran in parallel.

Memory recovered ground, rising to 39% of systems revenue from 34% in the prior quarter, with DRAM reaching a record 27% share on strong HBM investment and accelerating 1c node transitions.

NAND held at 12% of systems revenue, with management now projecting growth throughout the remainder of the year as the industry accelerates conversion to 256-layer and above devices.

CEO Tim Archer stated that the previously communicated $40B in NAND conversion spending will now be “pulled forward with the majority of spending occurring before the end of calendar year 2027,” a notable acceleration from prior expectations.

Gross margin for the quarter came in at 49.9% and operating margin hit 35%, both at the high end of guidance, driven by favorable customer and product mix and improved factory efficiencies.

For Q4 FY2026, Lam guided revenue of $6.6B and record EPS of $1.65, with operating margin of 36.5%, meaning the company is already operating above the high end of its prior long-term target model.

Management raised its 2026 WFE estimate from $135B to $140B with an upside bias, citing stronger customer spending projections across all device segments.

Bettinger confirmed that WFE growth is expected to continue into 2027, stating: “It feels like it’s setting up to be a pretty good year in ’27 right now based on what we can see,” citing increasing clean room availability as the primary catalyst.

Capital return activity was substantial: Lam allocated approximately $800M to share buybacks in the quarter at an average price of approximately $211 per share, retired $750M in unsecured notes, and paid $326M in dividends, returning 139% of free cash flow.

Lam also advanced key technology wins this quarter, achieving its first dielectric etch wins at a major foundry/logic manufacturer, a milestone Archer highlighted as evidence of portfolio breadth extending into new customer relationships.

Advanced packaging revenue is expected to exceed 50% growth for full calendar year 2026, supported by Lam’s copper plating and TSV etch capabilities.

The Dextro cobot program expanded to 8 tool types in the quarter, with next-generation units shipping for deposition products for the first time, adding automated maintenance precision to Lam’s installed base of more than 100,000 chambers.

Management noted that second-half calendar year revenues are expected to exceed the first half, and a long-term financial model update is planned later in 2026 given that operating margins have already exceeded prior targets.

Lam Research Stock Valuation: Strong Setup, Measured Upside

The TIKR model prices Lam Research stock at ~$376, implying approximately 27% upside from the current price of ~$296.

The mid-case model assumes a revenue CAGR of 16% and a net income margin of 33% over the forecast period, against a 1-year historical revenue growth rate of 24% and a current net income margin of 27%.

This quarter’s results reinforce both assumptions as achievable: revenue growth is running well ahead of the mid-case CAGR, and management’s own guidance points to continued margin expansion beyond the company’s prior long-term targets.

The risk/reward picture has improved meaningfully on the back of the WFE upward revision, the NAND conversion pull-forward, and the June quarter guidance that implies a sequential step-up in both revenue and operating margin.

At ~$296 with record forward guidance and a credible multi-year demand setup, Lam Research stock offers a reasonable entry for investors who accept that the mid-case return of 27% is back-weighted over 4-plus years.

Lam Research stock’s investment case now rests on whether the AI-driven equipment cycle sustains its intensity long enough for the NAND conversion pull-forward and WFE growth to flow through to earnings at the guided margin structure.

What Has to Go Right

- NAND conversion spending, concentrated before end of 2027, materializes on the accelerated timeline Archer described, driving systems revenue well above current NAND’s 12% share

- Gross margin holds at or above 50% through year-end, as Bettinger guided, despite customer mix headwinds cited for Q4

- Advanced packaging revenue exceeds 50% growth for full calendar 2026, adding a recurring growth vector that broadens Lam’s revenue base beyond traditional memory and foundry cycles

- The second Malaysia manufacturing facility ramps in the second half of 2026, allowing Lam to fulfill increasing demand without compressing margins through expedite costs or supply constraints

What Could Still Go Wrong

- Operating expense growth of approximately 5% to 7% per quarter, which management has committed to sustaining, limits downside earnings protection if revenue growth decelerates

- China revenue, at 34% of total in Q3 and expected to decline in Q4 per Bettinger’s guidance, creates a structural concentration risk if further export restrictions tighten

- Customer down payments are at their lowest level in nearly 4 years, signaling that the customers growing the fastest are not pre-committing capacity, which limits forward visibility in a demand softening scenario

- WFE growth in 2027 is currently management’s expectation but no formal guidance; a clean room build delay or memory customer spending pause could cause significant estimate revisions

Should You Invest in Lam Research Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Lam Research Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Lam Research Corporation stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze LRCX stock on TIKR for Free →