Key Stats

- Current price: ~$95 (May 11, 2026)

- Q1 2026 revenue: $6,701M (+7% YoY)

- Q1 2026 adjusted EPS: $1.09 (+10% YoY)

- Q1 2026 net income: $2,275M (+12% YoY)

- FY 2026 adjusted EPS guidance: $3.92 to $4.02 (targeting high end)

- Adjusted EPS CAGR guidance: 8%+ through 2032 (off 2025 base of $3.71)

- Dividend growth: ~10%/yr through 2026, 6%/yr through 2028

- TIKR model price target: $138

- Implied upside: +46%

NextEra Energy Stock Delivers 10% EPS Growth as Backlog Hits Record 33 GW

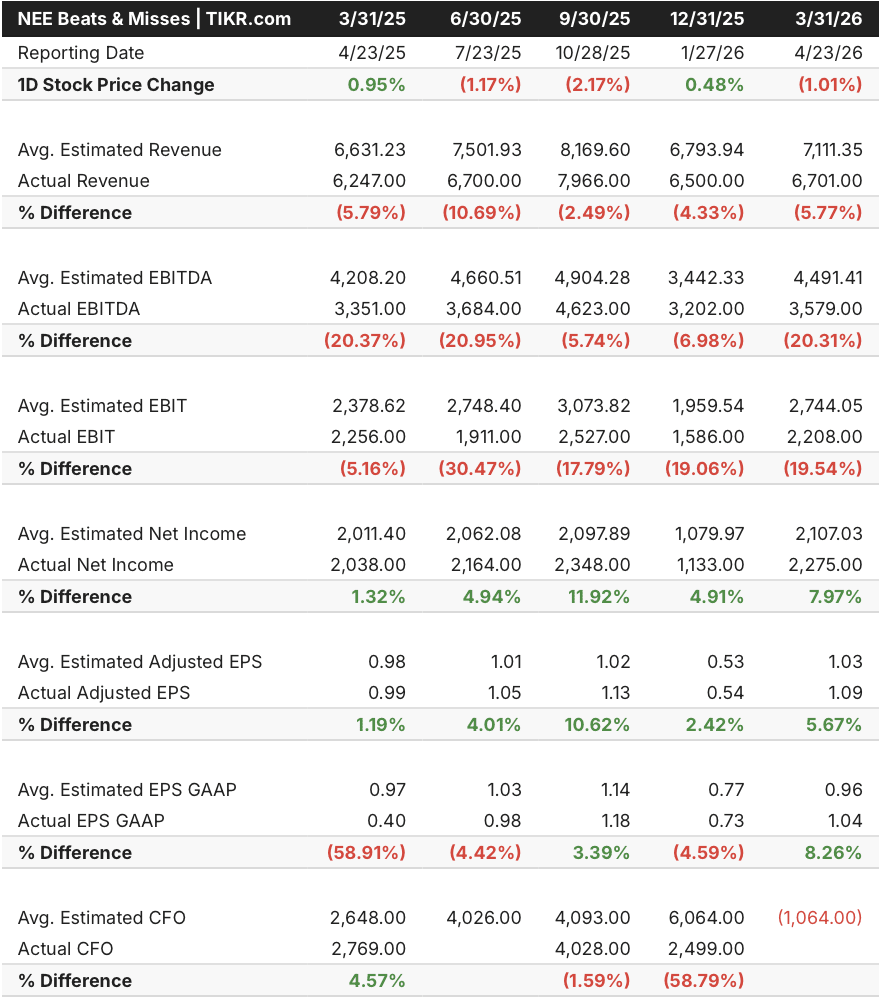

NextEra Energy stock (NEE) reported Q1 2026 adjusted EPS of $1.09, a 10% increase year-over-year and a beat against the Street’s $1.03 estimate.

Revenue came in at $6,701M, up 7% from $6,247M in Q1 2025, though it missed the $7,111M consensus estimate by nearly 6%.

The divergence between the revenue miss and the EPS beat captures the quarter’s story: bottom-line performance was strong even as top-line came in below expectations.

Energy Resources drove the headline result, reporting adjusted earnings growth of approximately 14% year-over-year, according to Executive Vice President and CFO Mike Dunne on the Q1 2026 earnings call.

The segment added 4 gigawatts of new long-term contracted renewables and storage to its backlog during the quarter, a record origination pace, bringing total backlog to approximately 33 gigawatts.

Battery storage accounted for 1.3 gigawatts of the Q1 additions, with the overall backlog split roughly 30% hyperscaler demand and 70% power utility customers, including cooperatives and municipalities.

Florida Power and Light also contributed positively, with FPL’s regulatory capital employed growing approximately 8.8% year-over-year, a primary driver of its EPS contribution, according to Dunne.

FPL’s Q1 capital expenditures were approximately $3.2B, and the company raised its full-year FPL capital investment guidance to $12B to $13B, up from the prior $10B to $11B range cited at the analyst event.

FPL added nearly 100,000 customers year-over-year during Q1, and retail sales grew approximately 3.4% on a reported basis, with weather-normalized growth of roughly 0.3%.

On the recontracting front, NextEra Energy locked in contracts for over 600 megawatts of existing projects during Q1, at an average contract length of over 18 years and at pricing approximately $20 per megawatt hour above prior realized rates, according to Dunne.

The U.S. Department of Commerce selected Energy Resources to build 9.5 gigawatts of new gas-fired generation under the U.S.-Japan trade framework, with projects in Texas and Pennsylvania designed to serve large load customers.

CEO John Ketchum characterized the structure as capital-light, with essentially zero capital outlay for NextEra Energy and fee streams tied to development, construction, and ongoing operations.

NextEra Energy Transmission received ERCOT approval for Lone Star Transmission to build portions of two new lines in North Central Texas, with NextEra’s investment share approximately $300M, representing a roughly 40% increase in Lone Star’s rate base.

NextEra Energy Transmission has now secured more than $5B in new projects since 2023, with total regulated and secured capital reaching $8B.

Energy Resources completed the acquisition of Symmetry Energy Solutions, one of the largest natural gas suppliers in the U.S., operating in 34 states, bringing NextEra’s total natural gas transport and delivery to approximately 2.9 trillion cubic feet annually.

NextEra Energy reaffirmed its 2026 adjusted EPS guidance range of $3.92 to $4.02 and stated it is targeting the high end.

The company also reaffirmed its 8%+ adjusted EPS CAGR target through 2032 and indicated it expects to target the same growth rate from 2032 through 2035, both off the 2025 base of $3.71.

Supply chain positioning was highlighted as a competitive advantage: solar panels secured through 2029, battery storage secured through 2029, wind components secured domestically through 2027, and transformer capacity sufficient through the end of the decade.

Beats & Misses

NextEra Energy stock beat on the bottom line and missed on the top, with adjusted EPS of $1.09 coming in 6% above the Street’s $1.03 estimate while revenue of $6,701M fell nearly 6% short of the $7,111M consensus.

The EBITDA miss was the sharpest gap: actual EBITDA of $3,579M came in over 20% below the $4,491M estimate, with EBITDA margins at 53% against a Street expectation of 63%.

Net income was the clear exception, beating estimates by nearly 8% at $2,275M against the $2,107M consensus, suggesting cost and tax dynamics below the operating line helped rescue the bottom-line result even as operating profitability fell short.

What Does the Valuation Model Say?

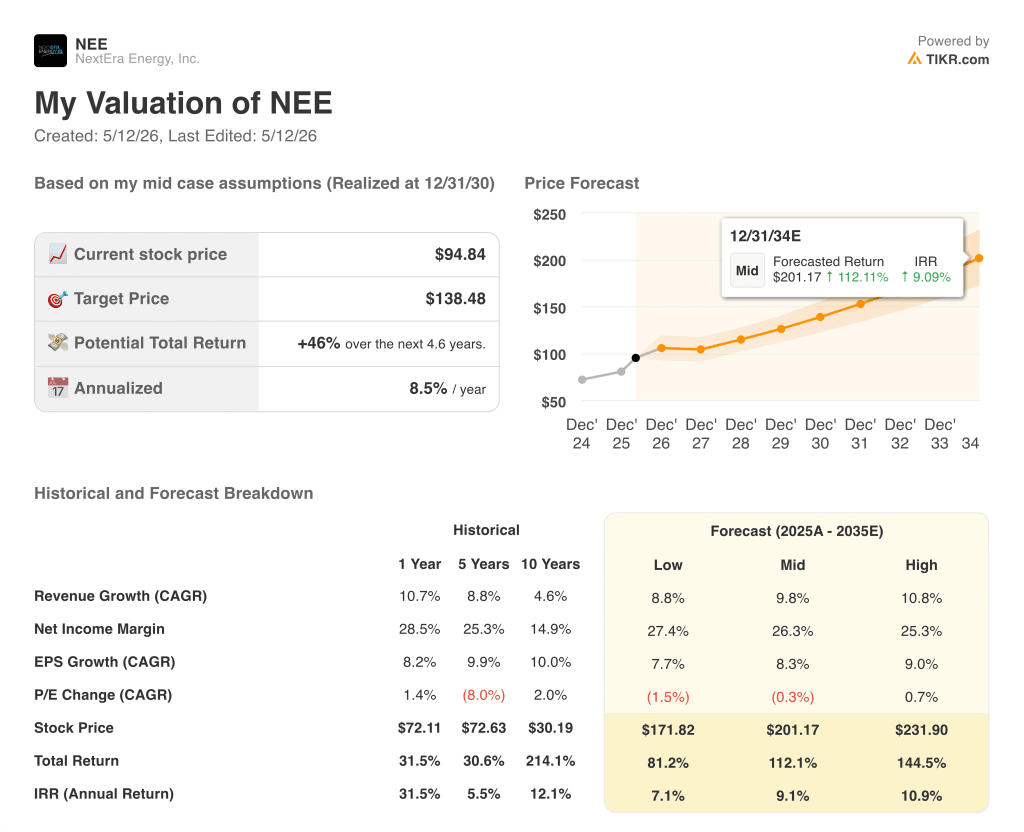

The TIKR model places a price target of $138 on NextEra Energy stock against a current price of approximately $95, implying roughly 46% total return over the next 4.6 years, or approximately 8.5% annualized.

The mid-case model assumes a revenue CAGR of approximately 10% and a net income margin of approximately 26% through 2030.

Q1 results reinforce the model’s assumptions: double-digit EPS growth, record backlog origination, and reaffirmed guidance all confirm that the core growth thesis is tracking on plan.

The investment case for NextEra Energy stock is incrementally stronger after this quarter, with execution matching guidance, supply chain secured ahead of demand, and multiple long-duration growth vectors (FPL customer growth, Energy Resources backlog, transmission, recontracting) all moving in the same direction.

Q1 showed strong execution, but the stock’s path to the $138 target depends on whether NextEra Energy can convert an unprecedented pipeline of opportunities into contracted, earning assets at scale.

What Has to Go Right

- The 33 GW backlog converts to in-service projects on schedule, sustaining the 8%+ adjusted EPS CAGR management has guided through 2032

- At least one large load customer signs under FPL’s approved tariff before year-end 2026, validating the 21 GW of FPL large load interest and roughly $2B CapEx per gigawatt

- The U.S.-Japan 9.5 GW project reaches definitive agreements within the 2-to-3-month window Ketchum described, turning fee streams into visible earnings contributors

- Recontracting at premium rates continues: the 600 MW contracted in Q1 at +$20/MWh above prior pricing is a leading indicator, with up to 6 GW of renewables and 1.5 GW of nuclear rolling off contract through 2032

What Could Still Go Wrong

- Revenue missed Street estimates by nearly 6% in Q1, and EBITDA missed by over 20%, signaling that margin conversion is not yet meeting consensus expectations

- FPL’s rate stabilization mechanism balance was drawn down by $306M in Q1, leaving approximately $1.2B remaining after-tax, a buffer that narrows with each quarter of utilization

- Gas-fired generation build timelines remain constrained by EPC labor and permitting reform, creating execution risk for the data center hub strategy and the U.S.-Japan projects

- Higher financing costs partially offset transmission gains in Q1, and with over $43B in interest rate hedging programs in place, any hedge roll-off into a higher-rate environment would pressure the bottom line

Should You Invest in NextEra Energy, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NextEra Energy stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NextEra Energy stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze X stock on TIKR for Free →