Key Stats

- Current Price: €6 (May 11, 2026)

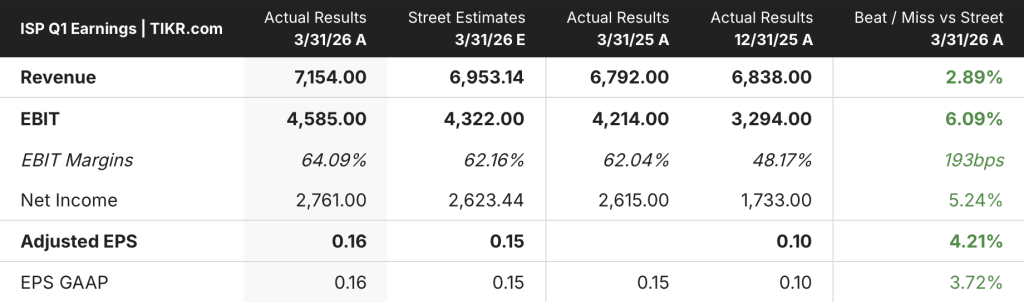

- Q1 2026 Revenue: €7.2B, up 5% YoY

- Q1 2026 Net Income: €2.8B (best ever quarterly result)

- Q1 2026 Adjusted EPS: €0.16, up from €0.10 in Q4 2025

- Q1 2026 EBIT: €4.6B, EBIT margin 64%

- 2026 Net Income Guidance: €10B

- 2026 Total Capital Return: ~€9.4B (including €2.3B buyback)

- TIKR Model Price Target: €8

- Implied Upside: +30% over 5 and a half years

Intesa Sanpaolo Q1 2026 Earnings Breakdown

Intesa Sanpaolo stock (ISP) posted its best-ever quarterly net income of €2.8B in Q1 2026, with annualized return on equity of 21% and EPS up 8% year-on-year.

Q1 revenue reached €7.2B, up from €6.8B in the same quarter a year ago, driven by record commissions and best-ever insurance income according to CEO Carlo Messina on the Q1 2026 earnings call.

Commission income grew 3% year-on-year, led by a 4% increase in Wealth Management and Protection, with €421M in dealing and placement fees representing the highest figure in that series, according to CFO Luca Bocca.

Insurance income hit a record quarterly high, with non-motor Property and Casualty as the primary growth driver; management guided for mid-single-digit insurance income growth for the full year.

The cost/income ratio came in below 36%, a best-ever level, supported by operating costs declining 1% year-on-year and a headcount reduction of more than 1,900 people over the prior 12 months.

Net interest income held year-on-year despite more than 60 basis points of Euribor decline, with the hedging book contributing a projected €500M positive impact to NII in both 2026 and 2027, according to Bocca.

Loans to customers grew 3% year-on-year and 1% quarter-on-quarter, led by Corporate and Investment Banking activity in infrastructure, energy transition, and international clients; management guided for full-year loan growth of 3% to 4%.

The annualized cost of risk was 16 basis points, well below the full-year guidance range of 25 to 30 basis points, with net NPL stock at €3.9B and €900M in overlays maintained in full with no release planned for 2026 or 2027.

Management confirmed its 2026 full-year net income guidance of €10B, with Messina noting that raising guidance in the first quarter is not the organization’s practice regardless of the strength of early results.

Intesa Sanpaolo stock will return approximately €9.4B to shareholders in 2026, comprising the May dividend, a November interim dividend, and a €2.3B buyback scheduled to launch in July.

The final 2025 dividend, payable in two weeks at the time of the call, was confirmed at 11% higher than the prior year.

Customer financial assets grew €64B year-on-year to more than €1.4T, with the quarterly decline attributed to negative market performance that had already been recovered in April.

The global adviser network stands at 19,000 people, with approximately 900 added in the past 12 months and a target of reaching 22,500 by 2028.

Messina explicitly ruled out any acquisition of Generali, citing antitrust constraints from Intesa Sanpaolo’s existing market share in Italian banking and insurance.

The group’s CET1 ratio was above 13% after accruing €2.6B for distribution in Q1, with a 15 basis point valuation reserve impact from March market volatility reported as fully recovered by the time of the call.

=

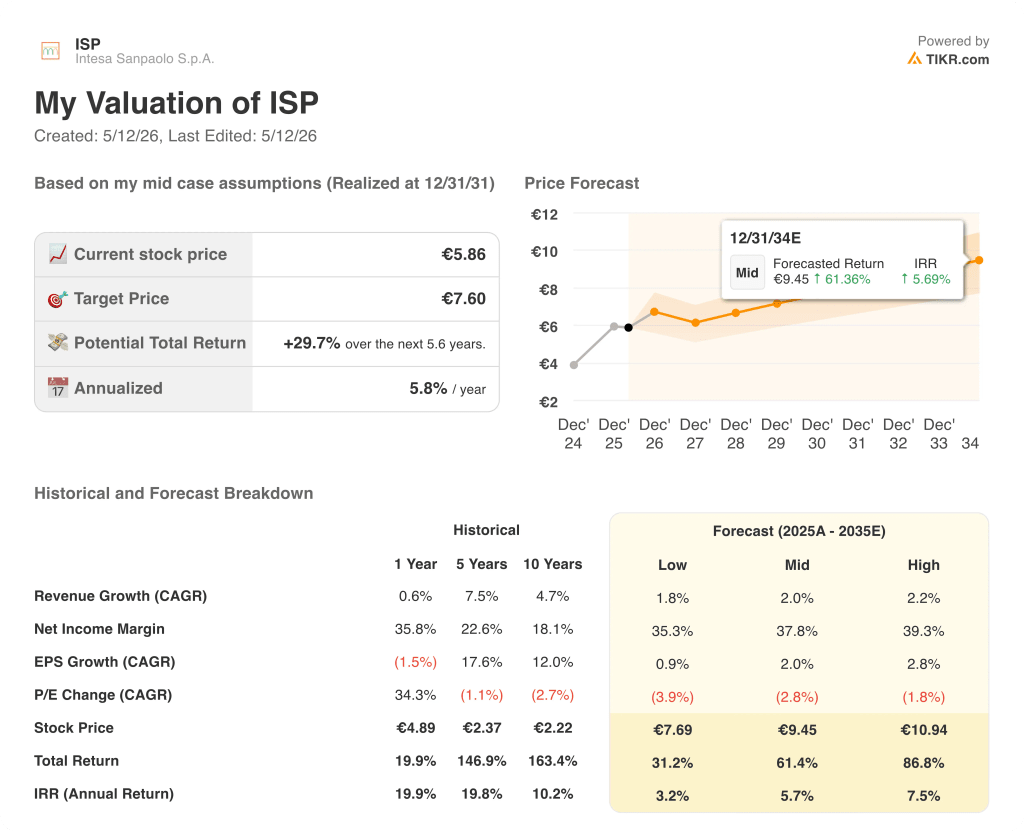

Intesa Sanpaolo Stock: Valuation Model Take

TIKR’s model puts Intesa Sanpaolo stock at €7.60 on the mid case, a 30% potential total return from the current €5.86 over the next 5.6 years.

The low case lands at €7.69 with a 31% total return, the mid at €9.45 with 61%, and the high at €10.94 with 87%, all realized by December 2031.

The spread between low and high is narrower than it looks: even the bear scenario implies the stock is undervalued at current prices, which says more about where ISP trades today than it does about execution risk.

The mid case assumes a revenue CAGR of 2.0% and a net income margin of 37.8%, conservative benchmarks given Q1 already delivered a 64% EBIT margin and a cost/income ratio below 36%.

With a cost of risk running at 16 basis points against a guided ceiling of 30, and €500M in NII hedge contribution locked in for both 2026 and 2027, the model assumptions look more like a floor than a ceiling.

At €5.86, the stock is priced as if the record Q1 is an anomaly. The scenario table suggests the market is wrong on all three cases.

Should You Invest in Intesa Sanpaolo S.p.A.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Intesa Sanpaolo stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Intesa Sanpaolo stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ISP stock on TIKR for Free →