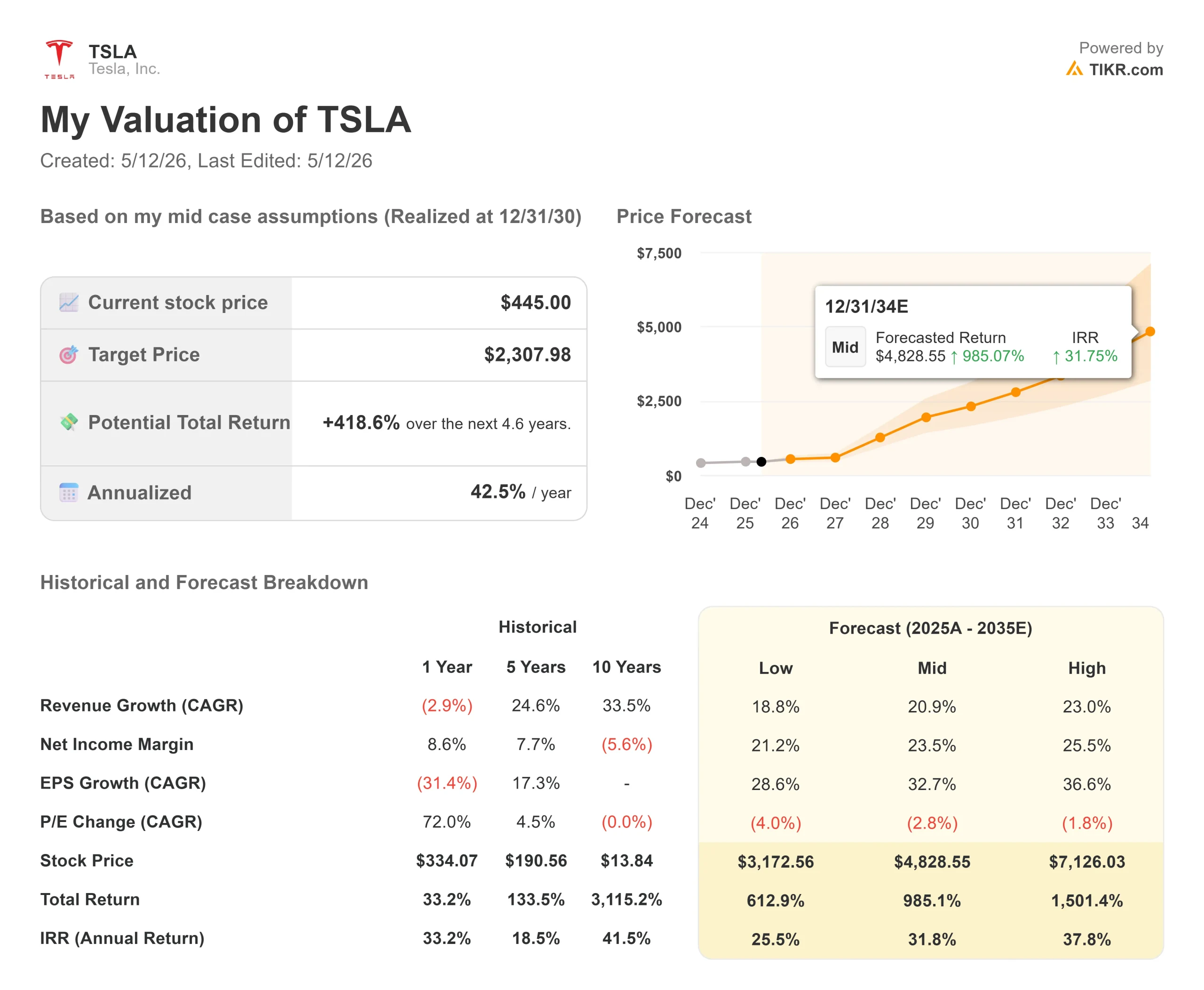

Key Stats for Tesla Stock

- Current Price: $445.00

- Target Price (Mid): ~$2,308

- Street Target: ~$412

- Potential Total Return: ~419%

- Annualized IRR: ~43% / year

- Earnings Reaction: -3.56% (April 23, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Tesla (TSLA) stock doesn’t move on earnings anymore. It moves on belief.

That dynamic played out clearly this week when Piper Sandler analyst Alexander Potter published his firm’s updated “Definitive Guide to Investing in Tesla,” sending shares up nearly 4% on Monday to close at $445.00. Potter built a discounted cash flow model across 17 separate product lines: vehicles, energy storage, Supercharging, in-house insurance, FSD subscriptions, and a standalone Robotaxi valuation, and concluded that Tesla’s core businesses are worth roughly $400 per share on their own. Optimus, Tesla’s forthcoming humanoid robot, was left out entirely. As reported by Yahoo Finance, Potter wrote: “At $400/share, we think investors can buy Optimus for free.”

Bulls say this finally gives structure to a stock that has long defied conventional analysis. Bears note that the “$400 floor” rests on a 233x fiscal year 2027 earnings multiple, as reported by Yahoo Finance, not a conservative assumption. The real debate: does the $45 premium above that base undervalue Optimus, or is the whole framework too rich before Tesla has shipped a robot at volume?

A second catalyst drove Monday’s move. Bloomberg reported that Elon Musk is expected to accompany President Trump on an official visit to China this week, putting Tesla at the center of U.S.-China trade discussions. That backdrop matters: China represented $20,962 million of Tesla’s $94,827 million in 2025 revenue, per TIKR segment data, and Tesla has been losing ground there to BYD and domestic competitors.

The Q1 Print Behind the Debate

The Piper Sandler note is a direct response to what Tesla reported on April 22.

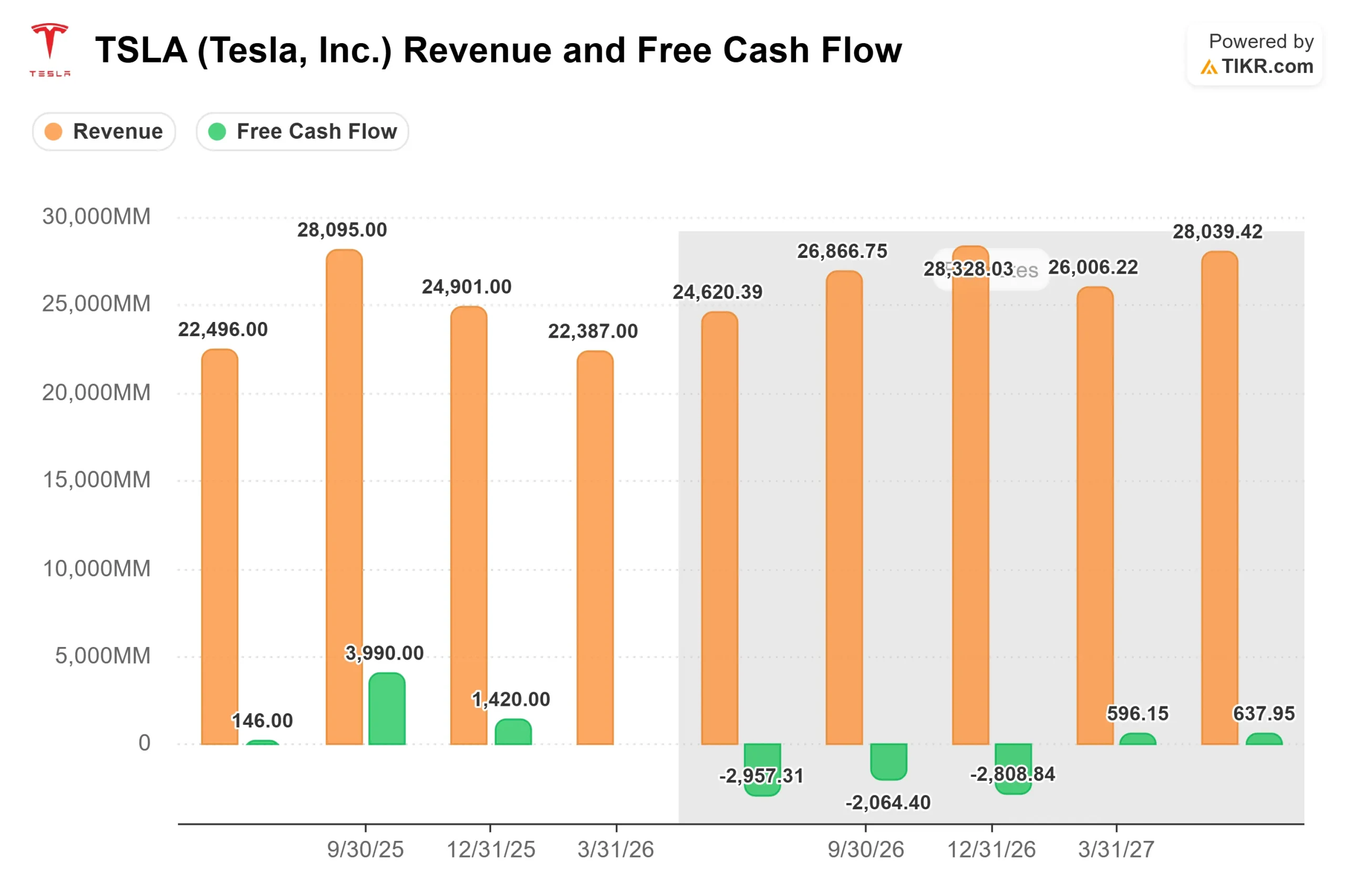

Q1 2026 revenue came in at $22,387 million against a consensus estimate of $22,208 million, per TIKR’s Beats & Misses data. Adjusted EPS of $0.41 beat the $0.35 consensus by 17.15%. Automotive gross margin, excluding regulatory credits, improved from 17.9% to 19.2% sequentially, per CFO Vaibhav Taneja on the earnings call.

Then came the reset. Taneja confirmed 2026 capital expenditure would exceed $25 billion, up from $8,527 million Tesla spent in all of 2025, per TIKR financials. He also confirmed free cash flow would be negative for the remaining three quarters of 2026. TIKR’s 2026 consensus FCF sits at around negative $9.3 billion, with FCF not expected to recover until 2028.

Tesla shares fell 3.56% the next day to $373.60. From that low, the stock has since recovered roughly 19% to $445.

Taneja explained the rationale on the call: “We are paying for 6 factories which were going to go into operation. We’re further increasing our investment in AI-related initiatives, including the AI infrastructure to support Robotaxi and the launch of Optimus. We will make such investments in a very capital-efficient manner.”

See historical and forward estimates for Tesla stock (It’s free!) >>>

What the Earnings Call Transcript Actually Says About Optimus

Piper Sandler assigns $100 per share to Optimus and admits it is probably too low. The Q1 call adds context to what that bet actually involves.

Musk confirmed that Fremont is being retooled after the last Model S and X vehicles exit in early May. He was clear-eyed about timing: “If we’re able to go from stopping production on one line, dismantling that entire line, reinstalling a whole new line and turning that on in a matter of 4 months, that is an insanely fast speed.” On volumes, he said it was “literally impossible to predict” output this year. A product with over 10,000 unique supply chain components means the ramp is governed by its slowest-solving part.

What Musk did confirm was the structural buildout. Tesla is constructing a second Optimus factory at Giga Texas, targeting production around summer 2027. The V3 design is being held back to prevent competitors from copying it ahead of launch. AI5, Tesla’s new inference chip, completed ahead of schedule, will go into Optimus and Tesla’s data centers rather than vehicles, because Musk said AI4 already achieves unsupervised driving safety above human levels. And Tesla has finalized plans for a $3 billion research semiconductor fab at Giga Texas, with Intel partnering using its 14A manufacturing process.

The bear reads this as ambition stacked on ambition before anything ships at scale. The bull reads it as the same pattern Tesla ran with EVs a decade ago.

Does the Valuation Hold Up?

At 100.22x NTM EV/EBITDA, Tesla has no precedent among auto peers. Per TIKR’s Competitors page, BYD sits at 7.05x and General Motors at 7.28x, against a peer median of 5.88x. Tesla’s multiple is a technology platform premium, and it demands that the Robotaxi and AI revenue transition actually happens.

The Street is split on whether it does. Per TIKR’s Street Targets data, 41 analysts currently cover Tesla: 18 Buy, 5 Outperform, 17 Hold, 3 Underperform, 4 Sell, and 4 No Opinion. The mean target is $412.25 below today’s $445, meaning the average analyst already sees Tesla as slightly ahead of fair value on conventional metrics. Potter’s $500 target is among the more optimistic on the Street.

Potter also cut his 2026 and 2027 estimates below consensus, citing lower deliveries from discontinued models and a shrinking contribution from high-margin regulatory credits. But as reported by Yahoo Finance, he argued that “historically relevant metrics are growing less important” as FSD subscriber counts and Robotaxi data take center stage. Nearly 1.3 million paid FSD customers globally as of Q1, with subscriber churn declining, is the early proof point.

That argument is either prescient or premature. The next two quarters decide which.

See how Tesla performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $445.00

- Target Price (Mid): ~$2,308

- Potential Total Return: ~419%

- Annualized IRR: ~43% / year

See analysts’ growth forecasts and price targets for Tesla stock (It’s free!) >>>

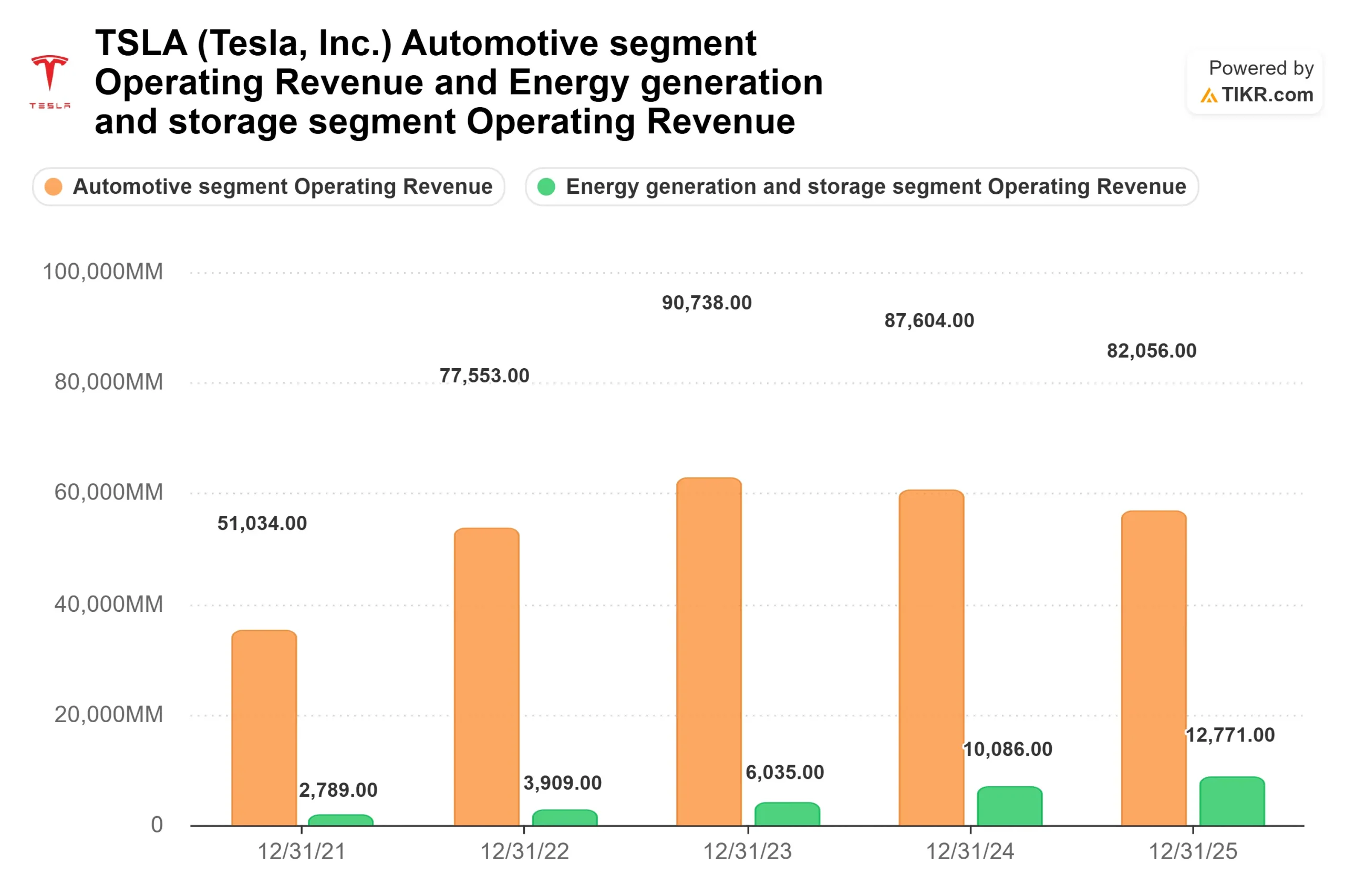

The TIKR mid-case model assumes a revenue CAGR of around 21% from 2025 to 2035, with net income margins expanding from around 6% today to around 24% by 2035. The two drivers are the energy storage segment, which grew from $3,909 million in 2022 to $12,771 million in 2025 per TIKR segment data, and the Robotaxi and FSD software stack, which Musk said on the call will be “material in a significant way” in 2027.

The upside scenario assumes Robotaxi reaches commercial scale across multiple U.S. metros by 2027, EU-wide FSD approval converts to meaningful subscription revenue, and Optimus production scales into the tens of thousands by 2028. The downside risk is sequencing: TIKR’s consensus shows FCF at around negative $9.3 billion in 2026 and around negative $1.9 billion in 2027. If Robotaxi faces a regulatory delay or a safety incident, or if Waymo, which already operates paid rides at scale in Phoenix, Los Angeles, and San Francisco, takes durable market share, the model’s 2027 inflection point slips.

The Street’s $412 mean target reflects exactly that skepticism.

Conclusion

Watch Tesla’s Robotaxi fleet count at the Q2 2026 report, expected around July 29, 2026. If Tesla exits Q2 operating in more than five U.S. states with unsupervised FSD advancing toward the broader customer fleet, the $45 premium above Piper’s $400 base starts to look justified. If the fleet stays at three cities and FSD V15 slips into 2027, that premium disappears quickly.

Tesla is not a car company being valued as one. It is a bet on whether Robotaxi, Optimus, and a vertically integrated AI stack can compound fast enough to justify a multiple the auto industry has never seen.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Tesla?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Tesla, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Tesla alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!