Key Stats for Palantir Stock

- Current Price: $136.89

- Street Target (Mean): ~$182

- Target Price (Mid): ~$786

- Potential Total Return: ~474%

- Annualized IRR: ~46% / year

- Earnings Reaction: -6.93% (May 5, 2026)

- Max Drawdown: -38.19% (April 10, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

The software sector has been waiting for proof that AI is a genuine revenue engine. Palantir (PLTR) just delivered that proof, and the stock fell anyway.

On May 4, 2026, Palantir reported its strongest quarter since its 2020 direct listing. Revenue grew 85% year over year to $1.633 billion against a $1.54 billion consensus. U.S. revenue crossed 100% growth for the first time, rising 104% to $1.282 billion. Adjusted free cash flow reached $925 million on a 57% margin. Management raised full-year 2026 revenue guidance to $7.656 billion, representing 71% growth. The next day, PLTR fell 6.93%.

The selloff had a logic to it. Valuation concerns, a DA Davidson price target cut from $180 to $165, and a prior HSBC trim from $205 to $151, combined with broader pressure on high-multiple software stocks. At 62x NTM EV/EBITDA and a $328 billion market cap, even a perfect quarter can disappoint on the margin.

But the reaction misses what the earnings call actually revealed. Most investors are debating the multiple. Few are reading the transcript closely enough.

Why Cheaper AI Tokens Are Actually Good for Palantir

CTO Shyam Sankar opened with an argument that explains why Palantir’s growth is accelerating while the rest of the enterprise software is getting disrupted. He called it Jevons paradox the economic principle that greater efficiency in resource use tends to increase total consumption.

“GPT-4 equivalent performance that cost $20 per million tokens in early 2023 is now approximately 1,000x cheaper three years later,” Sankar said on the call. As inference costs collapse, the number of tasks companies can economically assign to AI grows exponentially. But the more AI an enterprise deploys without proper controls, the more it risks what Karp calls “slop” AI outputs that look correct but cannot be governed or verified in a production environment. “Tokens are the new coal,” Sankar said. “AIP is the train.”

AIP (Palantir’s AI Platform) solves this through the Ontology, a proprietary representation of an organization’s data and relationships that lets AI agents operate with precision rather than guesswork. The commercial evidence is concrete. AIG is deploying AIP to run a multi-agentic underwriting and claims system, with agents evaluating risk and detecting fraud coordinated through the Ontology. GE Aerospace deepened its Palantir partnership after AIP drove a 26% increase in engine production. A major telecom used AIP not to reduce customer service calls but to generate proactive outreach for customers who would otherwise churn silently.

The pipeline behind those deployments reinforces the picture. U.S. commercial total contract value bookings hit $1.2 billion in Q1, the third straight quarter above $1 billion and $4.7 billion over the trailing twelve months, up 115% year over year. Net dollar retention, which measures how much existing customers spent relative to the prior period, hit 150%, up 1,100 basis points quarter over quarter. Total remaining deal value across the business reached $11.8 billion, up 98% year over year.

See historical and forward estimates for Palantir stock (It’s free!) >>>

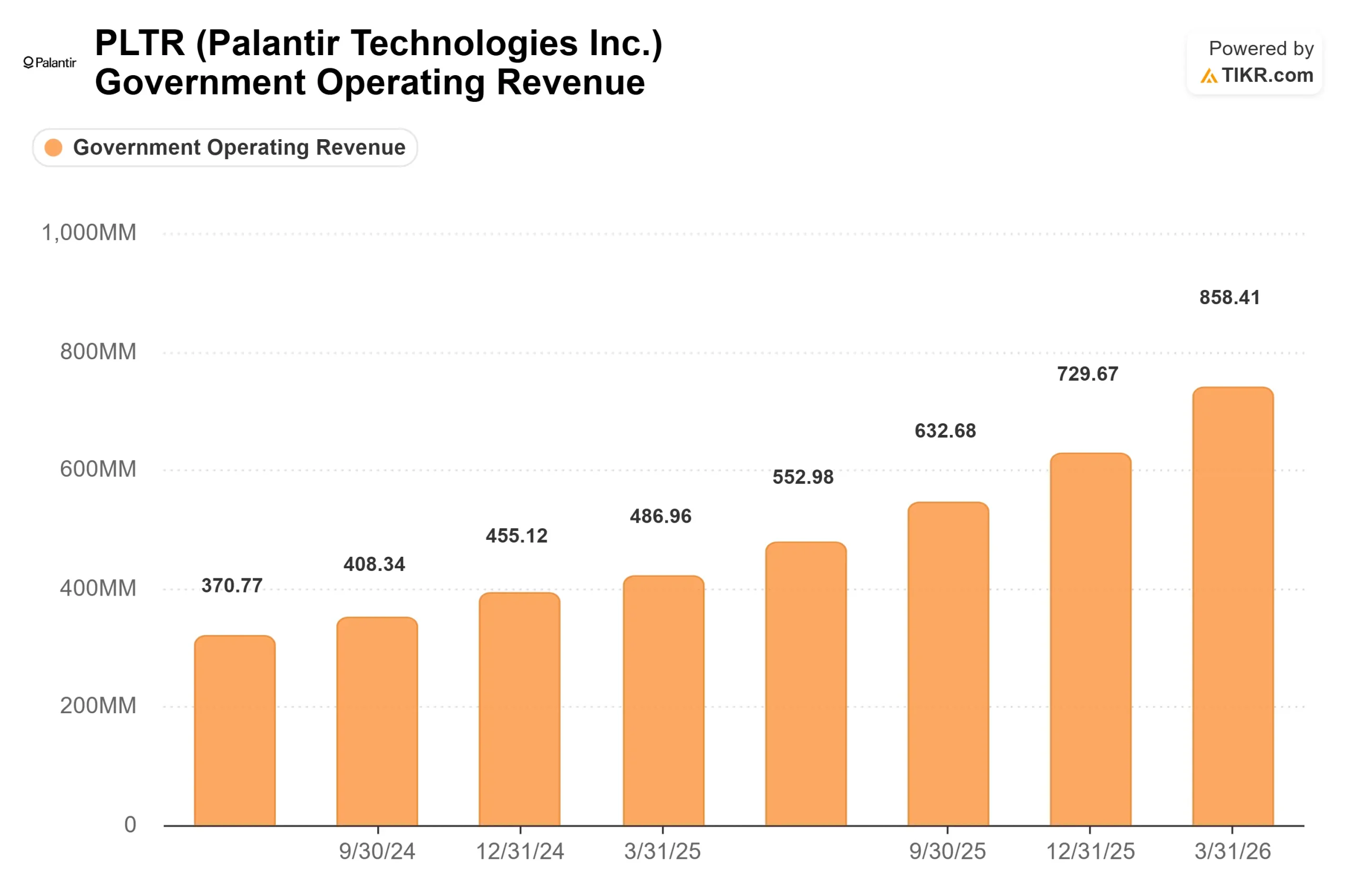

The Government Acceleration Is Being Underestimated

The commercial numbers get the headlines, but the government segment may be the more durable driver over the next two to three years.

Maven Smart System, Palantir’s AI platform deployed across U.S. military operations, doubled in usage over the four months through March 2026 and grew 4x over the prior twelve months across the services, combatant commands, joint staff, and intelligence community. ShipOS, Palantir’s Navy manufacturing platform, produced even starker results at industrial-base suppliers already using it: bill of materials approval time fell from 200 hours to 15 seconds, contract review cycles accelerated 57% to 73%, and monthly material planning time dropped 94%. Numbers like those make a government program politically protected. The alternative is measured in shipbuilding delays.

On the civil side, the USDA awarded Palantir a contract worth up to $300 million in April 2026 to implement its “One Farmer, One File” initiative, consolidating fragmented legacy farmer databases into a unified Foundry platform under the National Farm Security Action Plan. It extends Palantir’s footprint well beyond defense, and the national security framing makes the contract difficult to reverse under future administrations.

This pipeline is why CEO Alex Karp told CNBC after the earnings release that he expects the U.S. business to double again in 2027. He was blunter on the call: “Our biggest problem currently is demand in the U.S. We just cannot meet demand.” That is a demand-constrained business not a competition-constrained one.

The Valuation Premium in Plain Terms

Palantir trades at 37.62x NTM EV/Revenue and 62.02x NTM EV/EBITDA. The software peer mean across 26 comparables on TIKR sits at 4.07x NTM EV/Revenue and 10.60x NTM EV/EBITDA. For context, Microsoft trades at 8.46x NTM EV/Revenue and ServiceNow at 5.25x.

The premium only makes sense if Palantir’s growth is structurally different from software peers, and Q1 makes the case. U.S. commercial revenue grew 133% year over year. U.S. government revenue grew 84%. Free cash flow margin hit 57%. Per TIKR data, LTM ROIC is 22.7%, and LTM gross margin is 84.1%. No other software company at this scale is delivering those figures simultaneously.

The risk is equally structural. Any sustained deceleration in U.S. commercial growth, or a competing platform that replicates Ontology’s function without Palantir’s implementation model, would force a re-rating well before the revenue line shows it. That is the DA Davidson and HSBC argument in plain terms, and at 62x forward EBITDA, it is not without merit.

See how Palantir performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $136.89

- Target Price (Mid): ~$786

- Potential Total Return: ~474%

- Annualized IRR: ~46% / year

See analysts’ growth forecasts and price targets for Palantir stock (It’s free!) >>>

The TIKR mid-case uses a revenue CAGR of around 46% through 2035 and a net income profit margin expanding to around 49%. The two primary growth drivers are U.S. commercial AIP adoption, where the boot camp model converts enterprise prospects in days, and U.S. government expansion, where Maven, ShipOS, and civil contracts like the USDA deal extend Palantir’s footprint into spending categories that barely existed for the company three years ago.

The margin driver is operating leverage. With 60% adjusted operating margins and $8 billion in cash against no debt, incremental revenue increasingly flows to the bottom line. The 150% net dollar retention rate confirms this is already happening inside the existing customer base.

The primary risk is multiple compression across a nine-year forecast. Palantir’s returns depend on the market sustaining a premium valuation multiple through 2034. If competitors reduce the Ontology’s uniqueness or government priorities shift, re-rating happens well before revenue slows. The high case of approximately $4,756 requires around 51% revenue CAGR; any guidance miss in 2026 or 2027 pushes realistic outcomes well below that.

Conclusion

Watch U.S. commercial revenue on August 3, 2026, the Q2 earnings date. Management guided full-year U.S. commercial revenue above $3.224 billion (at least 120% growth). With $595 million in Q1, the remaining three quarters need to average roughly $877 million each to hit that floor. If Q2 clears $750 million, the annual target stays on track, and the most common bear argument loses its footing.

Palantir’s Q1 2026 results show a market underestimating what structural competitive advantage looks like when it shows up as ordinary revenue growth because most investors are not reading the transcript.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Palantir?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Palantir, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Palantir alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Palantir on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!