Key Stats for eBay Stock

- Current Price: $108.13

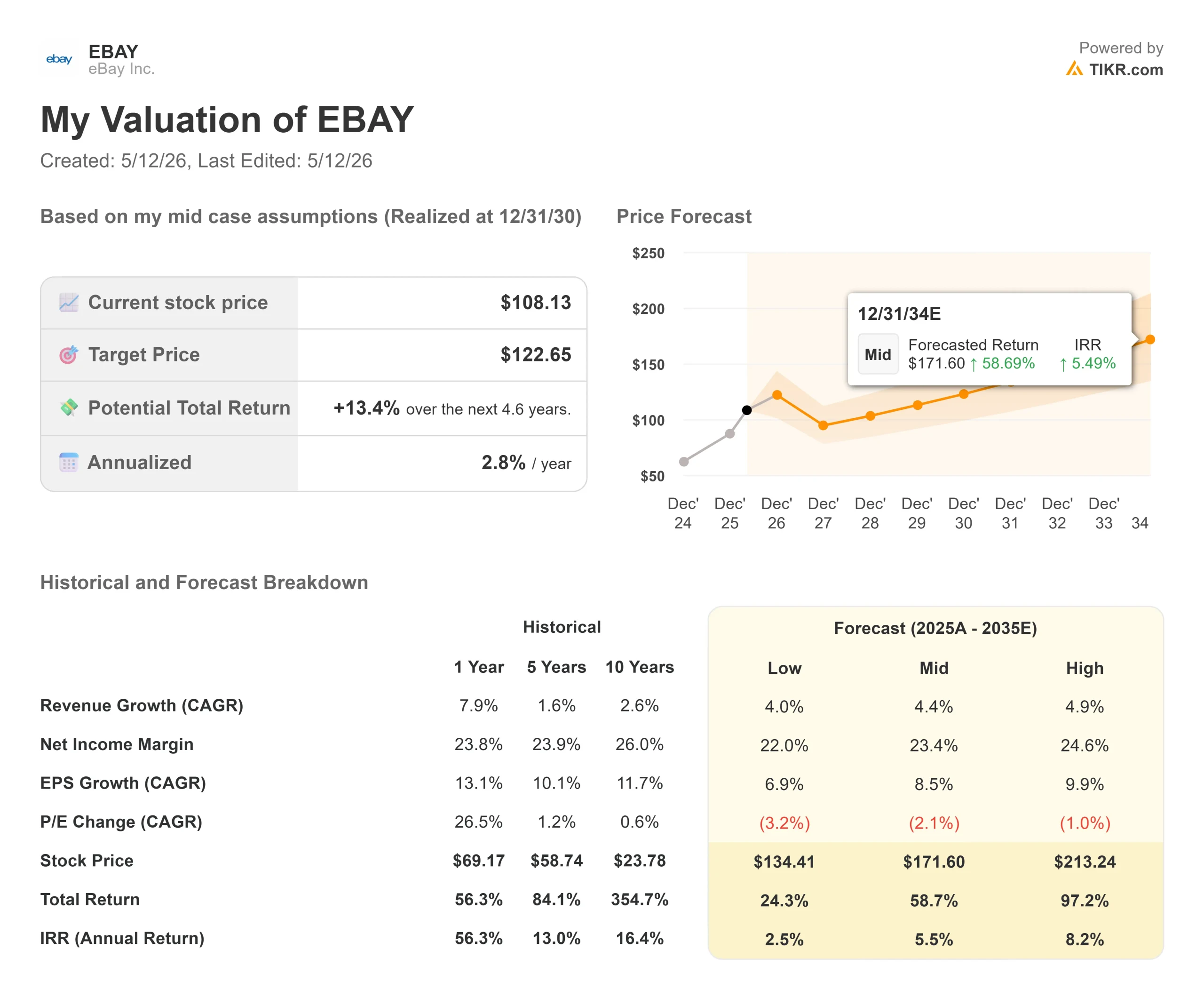

- TIKR Target Price (Mid): ~$123

- Street Target (Mean): ~$107

- Potential Total Return (Mid): ~13%

- Annualized IRR (Mid): ~3% / year

- Earnings Reaction: (0.30%) on April 29, 2026

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

eBay (EBAY) stock spent the past week trading with a bid-inflated tailwind that most investors never believed would pay off. That changed this morning. eBay’s board formally rejected GameStop’s $125-per-share offer, calling it “neither credible nor attractive,” and the stock slipped roughly 1% to around $107 in premarket trading.

Bulls say the rejection is a non-event because eBay’s business is accelerating on its own merits, and the Q1 results back that up. Bears point out the stock at $108.13 already trades above the Street’s mean analyst target of $107, and the TIKR mid-case model shows only around 3% annualized returns through 12/31/30. The question the market is now asking: do eBay’s fundamentals justify the price without a deal premium?

What eBay Rejected

On May 3, GameStop submitted a non-binding proposal to acquire eBay for $125 per share, 50% cash and 50% GameStop stock, valuing eBay at roughly $55.5 billion. GameStop said it had built a 5% stake in eBay and had a $20 billion debt financing commitment from TD Securities. The market was skeptical from the start: eBay peaked at its 52-week high of $111.38 after the announcement, a full $14 below the offer price, and never traded close to $125.

On May 12, eBay chairman Paul Pressler rejected the offer in a letter to GameStop CEO Ryan Cohen, citing financing uncertainty, leverage risks, and eBay’s stronger standalone prospects. Cohen has said he is willing to take the offer directly to eBay shareholders, so a hostile bid or proxy fight remains a possibility but not a certainty.

Q1 2026: What the Business Actually Looks Like

eBay’s investor relations materials show a business that genuinely accelerated in Q1 2026. Gross merchandise volume (GMV), the total dollar value of goods sold on the platform, rose 14% year-over-year to $22.2 billion on a foreign-exchange-neutral basis. Revenue grew 17% to $3.09 billion, beating the consensus estimate of $3.03 billion. Non-GAAP EPS of $1.66 beat the $1.58 consensus by 5%.

CEO Jamie Iannone described the momentum on the April 29 earnings call: “Our first quarter results exceeded our guidance and consensus estimates across the board despite ongoing macroeconomic and geopolitical uncertainty across many of our major markets.”

The growth was broad-based, which matters more than the headline numbers. U.S. GMV rose nearly 27%. eBay’s three strategic priorities, focused categories, consumer-to-consumer (C2C) selling, and recommerce (pre-owned and refurbished goods), now account for roughly 70% of total GMV, and each grew faster than the overall marketplace. Focus category GMV alone was up 24%, led by collectibles, but Motors, Parts, and Accessories also delivered its strongest year-over-year growth since 2021, and fashion GMV accelerated with luxury growing at healthy double digits.

First-party advertising revenue grew 28% to $555 million, with total advertising reaching $581 million and representing more than 2.6% of GMV. eBay generated $898 million in free cash flow in Q1 and returned $639 million to shareholders through $500 million in buybacks and a $139 million cash dividend.

The AI tools are also producing verifiable operating results. eBay’s magical listing tool, which generates listing titles, categories, and pricing from a single photo, drove a greater than 50% increase in new listing creation rates in the U.S. rollout. eBay’s agentic search beta is showing approximately 50% more engagement in sessions where it is used, translating into double-digit increases in purchase behavior. eBay Live, the platform’s live shopping feature, is running at a GMV annual run rate more than 8x higher year-over-year.

See historical and forward estimates for eBay stock (It’s free!) >>>

The Valuation After the Noise Clears

Here is the harder part. eBay at $108.13 is already above the Street’s mean analyst target of $107, based on a breakdown of 5 Buy, 5 Outperform, 19 Hold, 1 Underperform, and 2 Sell ratings. Most analysts covering the stock are on Hold.

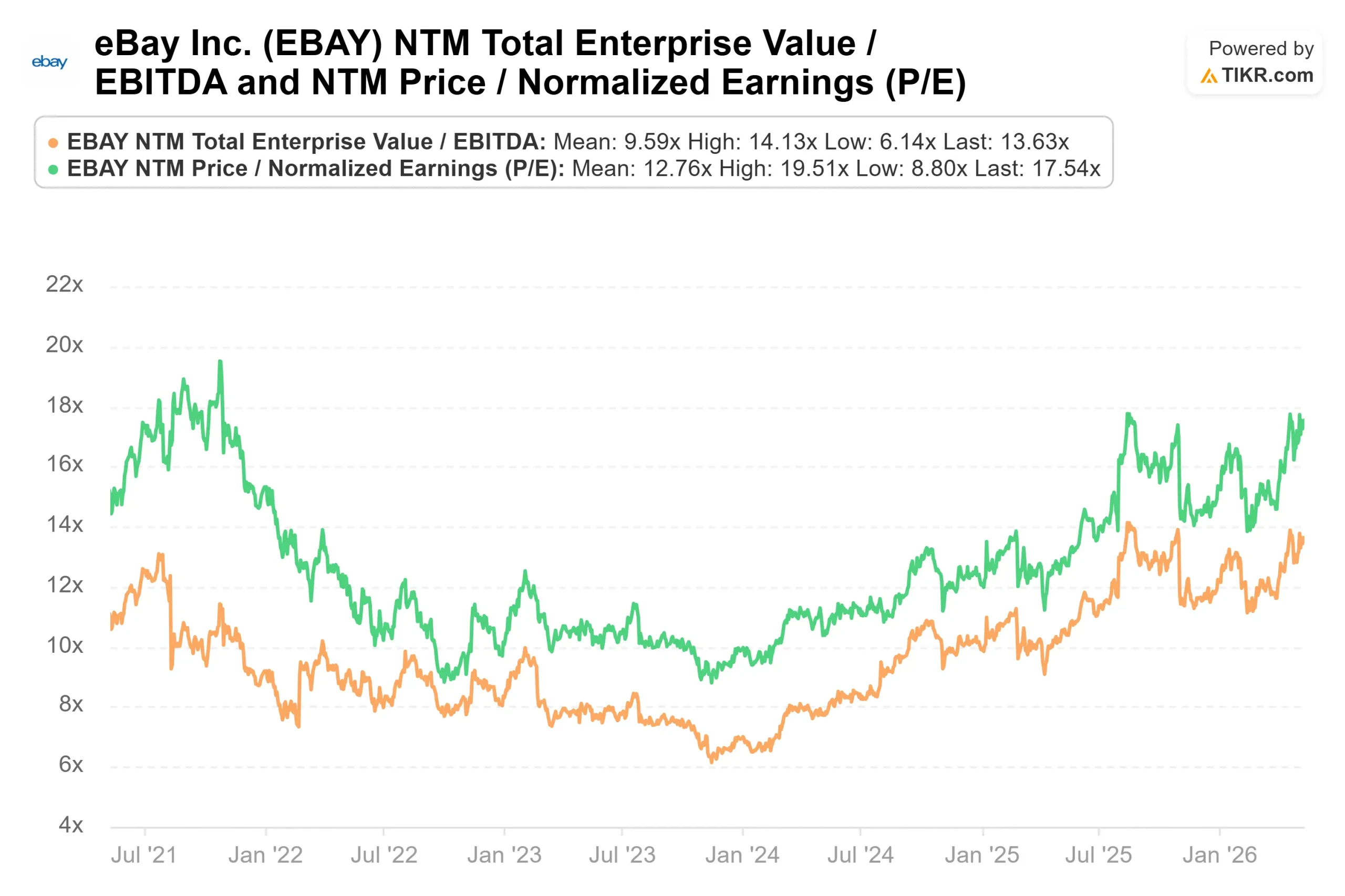

The TIKR mid-case valuation model puts the target at around $123 by 12/31/30, implying roughly 13% total return and around 3% annualized return from the current price. That model assumes a revenue CAGR of around 4% and a net income margin of around 23%. The stock is not cheap at 13.63xNTM EV/EBITDA and 17.54x NTM P/E.

The deceleration in eBay’s own guidance is the primary risk. CFO Peggy Alford projected, as management’s expectation, Q2 GMV growth of 8% to 10%, a significant step down from the 14% delivered in Q1, driven by tougher year-over-year comparisons and the expected normalization of gold and silver bullion demand that provided a temporary lift in Q1. Full-year GMV growth guidance of 7% to 7.5% and operating income growth of 9% to 11% are also management’s projections and not guaranteed outcomes.

The pending Depop acquisition, which Alford projected would close by the end of Q3 2026, is expected by management to add approximately 1 percentage point to full-year GMV growth while modestly diluting earnings per share in the near term.

See how eBay performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $108.13

- TIKR Target Price (Mid): ~$123

- Potential Total Return: ~13%

- Annualized IRR: ~3% / year

See analysts’ growth forecasts and price targets for eBay stock (It’s free!) >>>

The mid-case target of around $123 by 12/31/30 is driven by two revenue growth vectors: advertising monetization continuing to outpace GMV growth, and eBay Live and Depop scaling into meaningful contributors. The margin driver is operating leverage from AI-driven efficiency gains, with net income margins held at around 23%. The primary risk is a steeper-than-guided GMV deceleration in the back half of 2026, which would pressure the multiple at a stock already trading above analyst consensus.

At 3% annualized returns in the mid case, the standalone valuation does not make an obvious case for buying the stock at current prices. The Q1 results confirm the business is improving. Whether that improvement is already priced in is the question investors are left with now that the deal premium is gone.

Conclusion

With the GameStop bid rejected, the next real catalyst is Q2 earnings on July 29, 2026. The number to watch is GMV growth: if eBay delivers above the high end of its guided 8% to 10% FX-neutral range, it signals the Q1 momentum was not just noise. Below the low end would confirm the deceleration story the bears are pricing. The standalone case is real the valuation just doesn’t leave much margin for error at $108.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in eBay?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up eBay, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track eBay alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!