Key Stats for Apple Stock

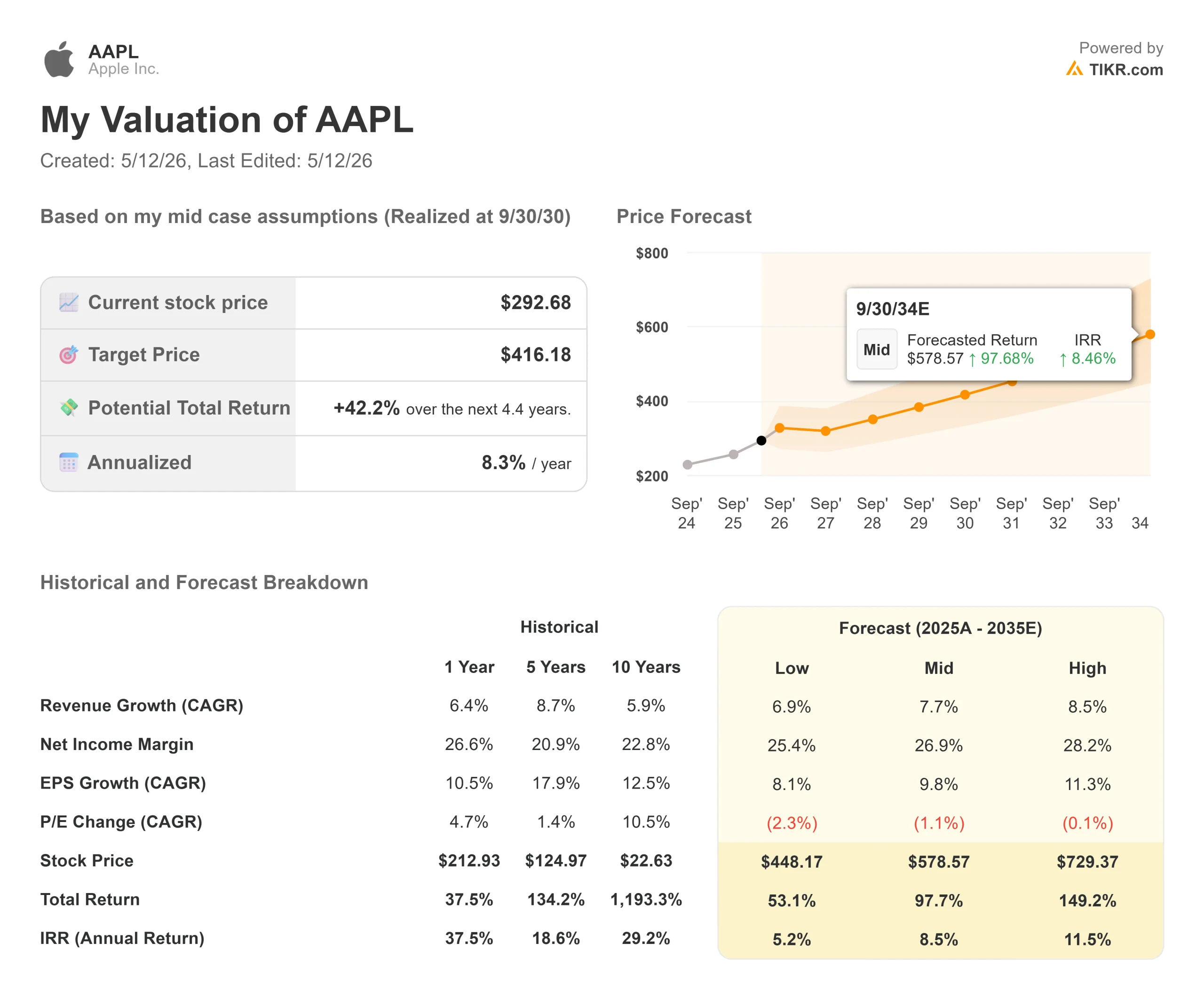

- Current Price: $292.68

- Target Price (Mid): ~$416

- Street Target: ~$305

- Potential Total Return (Mid): ~42%

- Annualized IRR: ~8% / year

- Earnings Reaction: +3.24% (April 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

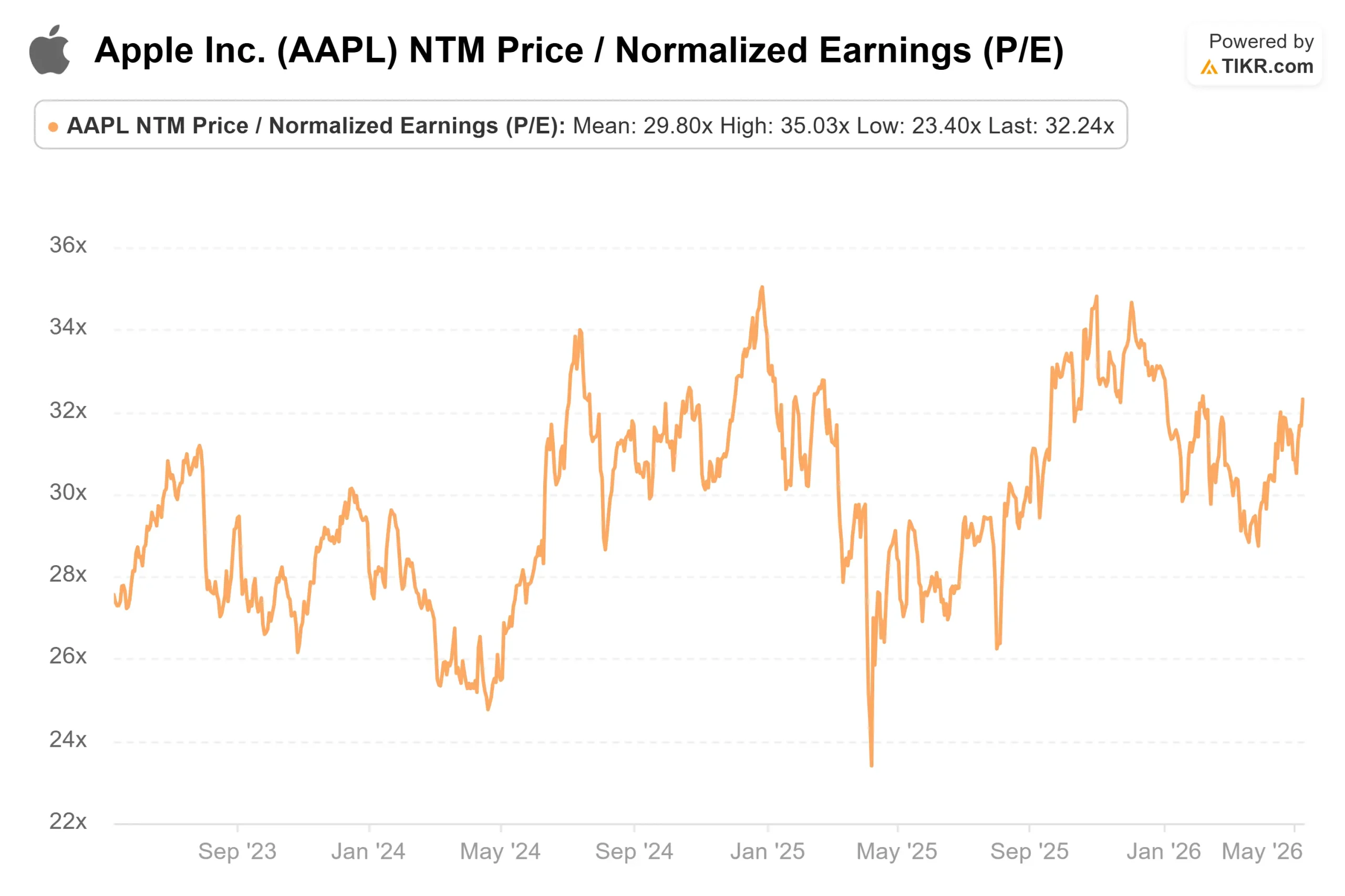

Apple (AAPL) stock rose 3.24% on April 30 after the company posted its strongest March quarter ever, and the stock has continued climbing since. Bulls point to a record quarter, a guidance raise that blew past consensus, and Wedbush’s Daniel Ives setting a Street-high $400 price target this week, calling Apple “the sleeping tech giant about to see a major inflection point.” Bears argue that memory cost headwinds are accelerating, and at 32x next twelve months P/E, there is limited room for disappointment. The key question: Is WWDC 2026, scheduled for June 8, the catalyst that finally closes the gap between Apple’s installed base and its AI monetization?

What Wedbush Sees That the Street Doesn’t

On May 8, Wedbush raised its Apple price target from $350 to $400, the highest figure any investment firm has ever set on AAPL, per AppleInsider’s review of the note. Analyst Daniel Ives kept his Outperform rating and described Apple as the “consumer hub of AI,” arguing that roughly 20% of the world’s population will access AI through an Apple device in the coming years. The thesis centers on a $15 billion annual revenue opportunity from Apple monetizing third-party AI models across its 2.5 billion active devices. With iOS 27 reportedly set to let users choose their preferred AI model as a default, Apple would collect a cut of usage from ChatGPT, Gemini, and other services through the world’s most loyal device ecosystem.

The Q2 2026 earnings call supports this premise concretely. CFO Kevan Parekh said on the call that AI startup Perplexity chose Mac as its preferred platform for building enterprise AI assistants and autonomous agents, a named account validating Apple Silicon as an agentic AI development platform today. Parekh also confirmed that advertising will come to Apple Maps in the U.S. and Canada this summer, adding a monetized layer to a service used by hundreds of millions of people daily.

The broader Street is more cautious. Per TIKR’s Street Targets, the mean analyst price target sits at around $305, with 24 Buys, 7 Outperforms, 15 Holds, 1 Underperform, 1 Sell, and 2 No Opinions. That implies only modest upside from today’s price.

See historical and forward estimates for Apple stock (It’s free!) >>>

The Quarter That Earned the Upgrade

Revenue reached $111.2 billion in Q2 FY2026, up 17% year-over-year, a March quarter record that came in above the high end of guidance despite supply constraints on iPhone and Mac. Diluted EPS was $2.01, up 22% year-over-year, beating the $1.94 average analyst estimate per TIKR’s Beats & Misses data.

iPhone revenue was $57 billion, up 22% year-over-year, the strongest March quarter in company history. CEO Tim Cook said on the call that customer satisfaction for the iPhone 17 family in the U.S. was measured at 99% by 451 Research. According to IDC, Apple gained smartphone market share during the quarter despite running below demand.

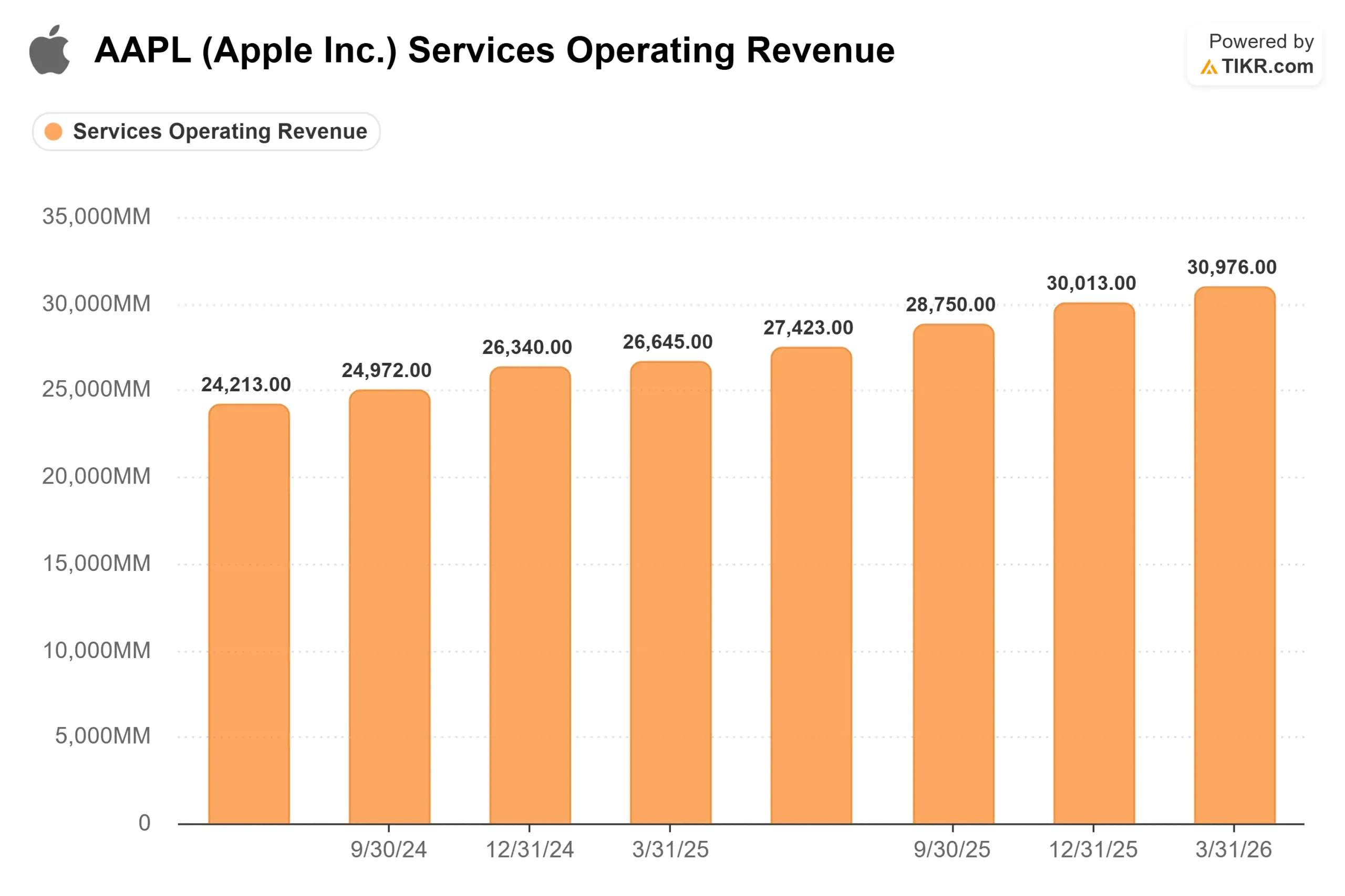

Services hit an all-time record of $31 billion, up 16% year-over-year. Per Parekh’s prepared remarks on the call, the segment ran at a 76.7% gross margin, versus a product gross margin of 38.7%. Each additional dollar of Services revenue generates roughly twice the gross profit of an equivalent hardware dollar. Both transacting and paid accounts reached new all-time highs.

Mac revenue was $8.4 billion, up 6%, driven by MacBook Neo. Cook called the customer response “off the charts,” with school systems like Kansas City Public Schools switching from Chromebooks and Windows PCs to MacBook Neo.

For the June quarter, management guided total revenue growth of 14% to 17% year-over-year, well above what analysts had expected, which was the primary driver of the after-hours stock move. The board authorized an additional $100 billion in share repurchases and raised the quarterly dividend 4% to $0.27 per share.

Where the Risks Are

Cook was direct on the earnings call: “beyond the June quarter, we believe memory costs will drive an increasing impact on our business.” Apple already guided June quarter gross margin at 47.5% to 48.5%, down from 49.3% in Q2, incorporating what Parekh called “significantly higher memory costs.” If those costs persist into fiscal 2027, the pressure would last longer than current consensus estimates assume.

The June quarter will also bring supply constraints on Mac Mini, Mac Studio, and MacBook Neo. Cook said the Mac Mini and Mac Studio may take “several months to reach supply-demand balance,” meaning Apple is leaving hardware revenue on the table into at least September, the same quarter John Ternus officially becomes CEO.

On valuation multiples, TIKR’s Competitors page shows Samsung at 3.90x NTM EV/EBITDA and Xiaomi at 15.41x, against Apple’s 24.57x. That premium reflects margins and an installed base neither peer can replicate. But at 32x NTM P/E, any execution stumble at WWDC 2026 or delay in AI monetization could compress the multiple faster than free cash flow growth can absorb it.

See how Apple performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $292.68

- Target Price (Mid): ~$416

- Potential Total Return: ~42%

- Annualized IRR: ~8% / year

See analysts’ growth forecasts and price targets for Apple stock (It’s free!) >>>

The mid-case uses a revenue CAGR of around 8% through fiscal 2030, built on two drivers: continued Services monetization across 2.5 billion active devices, and sustained iPhone replacement demand through the Apple Intelligence cycle. Cook confirmed double-digit iPhone growth for two consecutive quarters despite supply constraints. The margin driver is Services mix shift: as Services grows as a share of revenue, each additional dollar gained carries roughly twice the gross profit of an equivalent hardware dollar, per the Q2 earnings call margins. The mid-case assumes a net income margin of around 27%, a modest improvement from the 26.6% one-year historical figure shown in TIKR’s model.

The primary risk is sustained memory cost pressure through fiscal 2027, which would require stronger Services growth to compensate. The upside requires a credible AI roadmap at WWDC 2026 and early monetization of third-party AI access. Both outcomes are possible from where the stock sits today.

Conclusion

Watch Services’ gross margin at Apple’s next earnings report, expected July 30, 2026. If it holds above 76% while total revenue comes in at or above the midpoint of the 14% to 17% guidance range, it confirms the high-margin monetization engine is holding up against the memory headwind. Apple delivered a record quarter, guided well above consensus, and just received the highest analyst price target in its history. WWDC 2026 on June 8 is where the AI story either accelerates or stalls.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Apple?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Apple, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Apple alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!