Key Stats for ServiceNow Stock

- 52-Week Range: ~$80 to ~$207

- Current Price: $91.49

- Street Mean Target: ~$120

- TIKR Target Price (Mid): ~$229

- TIKR Annualized IRR (Mid): ~22% per year

- Q1 2026 Subscription Revenue: $3.67B (up 22% YoY)

- Q1 2026 Non-GAAP Operating Margin: 32%

- FY2026 Subscription Revenue Guidance: $15.74B to $15.78B (up ~21%)

Value your favorite stocks like NOW with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

Why ServiceNow Beat Q1 and the Stock Still Fell 13%

ServiceNow’s (NOW) Q1 2026 results, reported on April 22nd, were not ambiguous. Subscription revenue of $3.67 billion grew 22% year over year. Current remaining performance obligations (cRPO) grew 22.5% to $12.64 billion.

The number of customers spending more than $1 million annually on Now Assist, the company’s AI product suite, grew by more than 130% year over year. Management raised its full-year subscription revenue guidance by $205 million at the midpoint and lifted its 2026 AI-specific revenue target from $1 billion to $1.5 billion. The stock fell 13% in after-hours trading anyway.

The disconnect reflects a dynamic that has been weighing on ServiceNow throughout 2026. The market is not questioning the business. It is questioning what multiple the business deserves at a time when enterprise software valuations have broadly compressed, and investors are demanding faster proof that AI investments translate into durable revenue.

CEO Bill McDermott was direct on the call: “Our AI growth is far exceeding even our own expectations, reinforcing our position as one of the fastest growing enterprise software companies ever.” The business is delivering on that framing. The stock has not been rewarded for it.

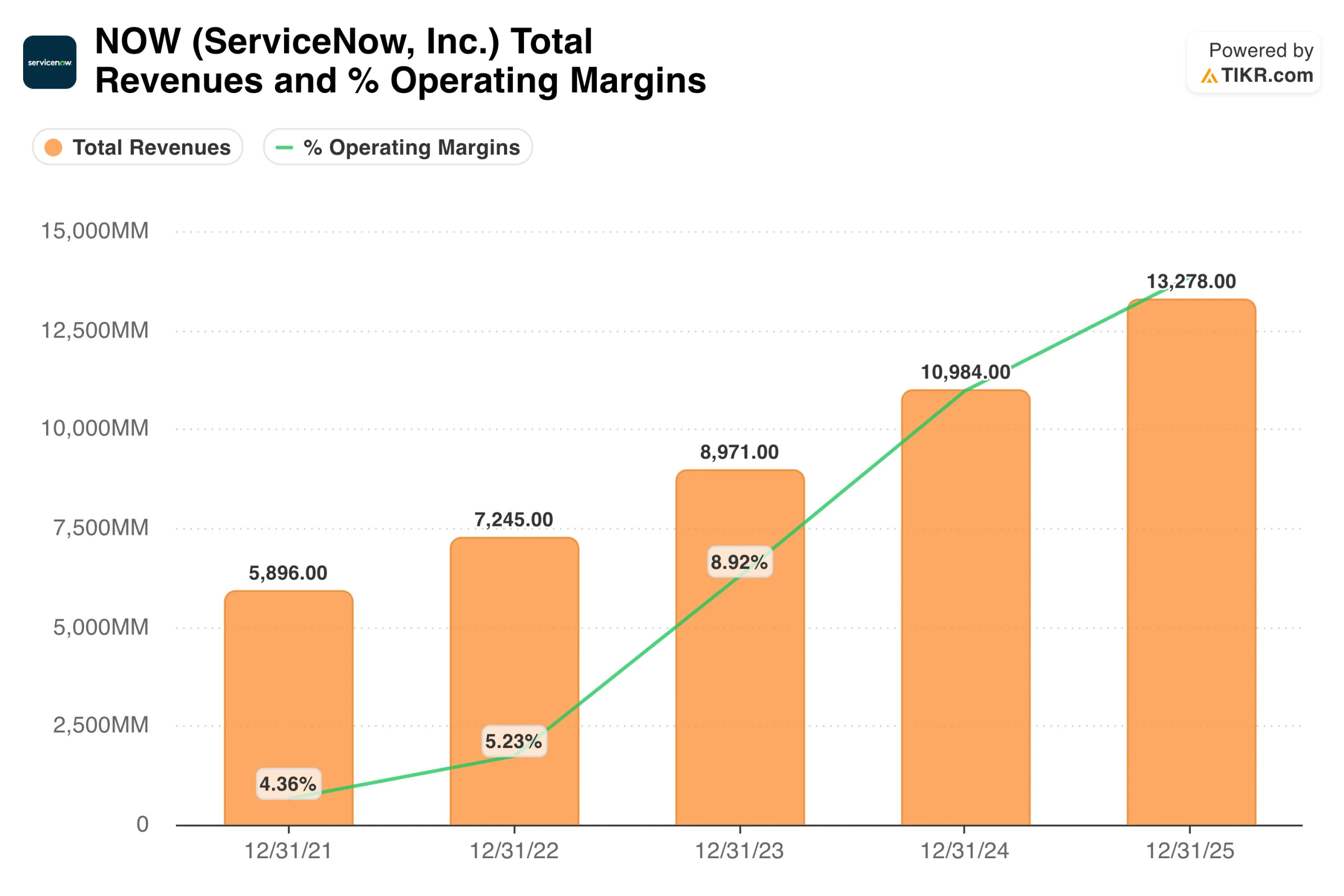

The revenue chart shows what consistent compounding looks like at scale. ServiceNow grew from $5.9 billion in 2021 to $13.3 billion in 2025, nearly doubling in four years while GAAP operating margins expanded steadily throughout.

On a non-GAAP basis, which strips out stock-based compensation, the company runs at 32% operating margins. Few software businesses of this scale sustain that level of profitability while still growing at 22% annually. McDermott calls it the “Rule of 55”: revenue growth rate plus non-GAAP operating margin, consistently above 55.

See analysts’ growth forecasts and price targets for NOW stock (It’s free!) >>>

Why Wall Street Has Not Given Up on NOW Despite the Selloff

Street consensus remains positive, with price targets clustering around $110 to $130, implying meaningful upside from current levels. The hesitation to push targets higher reflects multiple concerns about compression, not skepticism about the business itself.

The product momentum from Knowledge 2026 last week is real. ServiceNow unveiled Otto, a unified AI experience combining conversational AI, enterprise search, autonomous workflows, and voice agents. The company also launched its Autonomous Workforce platform, which deploys AI specialists capable of executing end-to-end enterprise tasks in IT, customer service, and security.

Internally, ServiceNow’s own agents now resolve 90% of employee IT cases, 99% faster than human agents. The competitive moat McDermott keeps returning to is the Context Engine: 22 years of enterprise workflow data that grounds AI actions in specific business rules and governance requirements that a standalone large language model simply cannot replicate.

What the EPS Trajectory Says About ServiceNow’s Earnings Power

ServiceNow grew normalized EPS from $1.18 in 2021 to $3.51 in 2025, roughly 24% annual compounding. Consensus then projects around $4 in 2026, accelerating to around $5 in 2027, around $6 in 2028, and approaching $9 by 2030. There is no earnings dip in this chart, no guidance cut, no year-over-year compression. The line goes up consistently, even as the stock has moved in the opposite direction.

That divergence is the central tension in the ServiceNow investment case. The business is growing earnings at roughly 20% per year. The stock has been re-rated lower because the market is paying less per dollar of those earnings than it was a year ago. Whether that multiple contraction has run its course is the variable that matters most.

Value NOW instantly (Free with TIKR) >>>

What the TIKR Model Implies at the Current Entry Point

The TIKR model targets around $229 per share in the mid case, implying a total return of roughly 150% over about 4.6 years, or about 22% annually.

The model uses revenue growth of around 16% per year, meaningfully below the 22% ServiceNow just delivered and the 21% full-year guidance management raised. Net income margins of around 32% are in line with current non-GAAP performance.

These are not optimistic assumptions; they are roughly in line with where the business is operating today, applied forward. The high case implies around $590 by 2035. Even the low case targets around $310. The range of outcomes skews heavily to the upside from the current price.

The Case for NOW: Sticky Workflows, AI Monetization, and a $30 Billion Revenue Target

The workflow lock-in is structural. ServiceNow sits at the center of how large enterprises manage IT, HR, customer service, and security operations. Replacing it is not a software swap; it is a multi-year operational disruption. That stickiness has historically produced gross retention rates above 98%, which means growth compounds on an extremely stable base.

Now Assist is already generating measurable revenue at scale, with AI ACV growing 130% year over year and a revised 2026 target of $1.5 billion reflecting contracts already signed, not projections. Management has embedded Now Assist across all SKUs rather than selling it as a separate add-on, so every renewal and expansion includes AI monetization.

Management’s stated conservative target is $30 billion in subscription revenue by 2030. At $13.3 billion in 2025, reaching that number requires roughly 18% annual growth, and the current trajectory supports that math.

The Risks: Multiple Compression, Integration Costs, and a High Bar to Clear

The multiple compressions may not be finished. ServiceNow still trades at a premium to the broader software sector, even after a 40% decline, and if enterprise software valuations continue to contract, the stock could remain under pressure regardless of execution.

The Armis acquisition also introduces near-term margin headwinds through 2026, with normalization expected in 2027. For a stock where every quarterly margin print gets scrutinized, that creates a window of elevated sensitivity.

And the current valuation prices in a long runway of AI revenue acceleration; if large deal signings moderate or enterprise AI spending commitments slow, the premium embedded in the multiple becomes harder to justify.

Is NOW Worth Buying at $91?

ServiceNow has compounded revenue at over 20% annually for more than a decade, maintained non-GAAP operating margins above 30%, and built a platform that is genuinely difficult to displace. The current selloff has not changed any of those facts.

The TIKR mid-case target of around $229 at roughly 22% per year is one of the more compelling return profiles in large-cap software at the current price, built on assumptions that are conservative relative to what the company is actually delivering. The EPS trajectory, with uninterrupted compounding from $1.18 to an estimated $8.66 by 2030, suggests the underlying business has not noticed the stock’s decline.

The question is patience, as ServiceNow is not cheap in absolute terms, and the multiple could keep compressing before it recovers. But for investors with a 3- to 5-year horizon, the combination of durable growth, AI monetization already showing up in contract data, and an entry point 40% below a year ago is a setup that is difficult to find in quality software.

See analysts’ growth forecasts and price targets for NOW stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!