Key Takeaways:

- ServiceNow (NOW) stock has fallen around 40% year to date and around 52% below its 52-week high of $211, but the underlying business continues to grow revenue at more than 20% annually.

- Management revealed plans for total revenue to reach $32 billion by 2030, roughly doubling from current levels, and analysts forecast over $30 billion in subscription revenue alone by 2030.

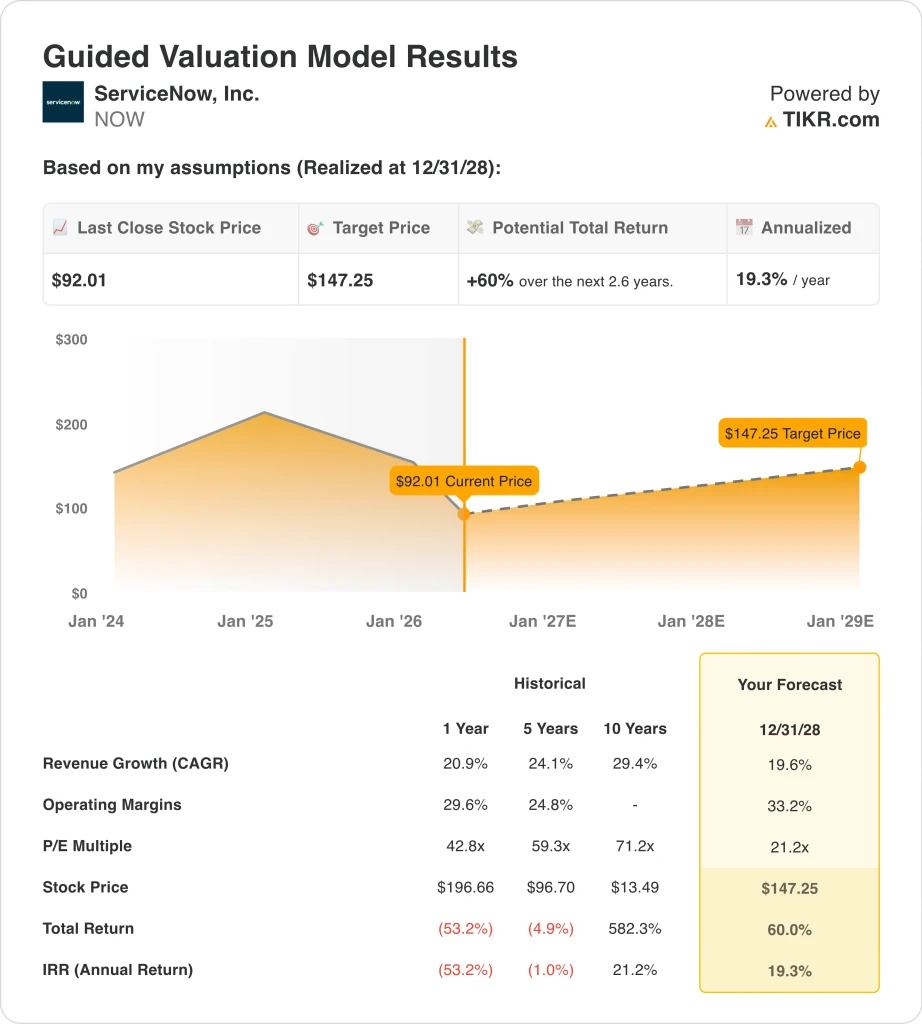

- Our valuation model projects NOW stock could rise from $92 to around $147 per share by December 2028, based on around 20% annual revenue growth, 33.2% operating margins, and a 21.2x P/E multiple.

- That implies a 60% total return and an annualized return of around 19% over the next 2.6 years.

What Happened?

ServiceNow (NOW) has had a brutal 2026 so far. But the underlying business continues to grow at impressive rates. The stock has fallen around 40% year to date and now sits near its 52-week low of $81. Revenue for Q1 2026 came in at $3.77 billion, beating analyst estimates of $3.74 billion and growing around 22% year over year.

AI is now the central theme driving ServiceNow’s long-term story. The company unveiled an enterprise AI assistant called Otto at its Knowledge 2026 conference in early May. Management also shared plans for revenue to reach $32 billion by 2030, and analysts followed with forecasts of over $30 billion in subscription revenue alone. These announcements lifted investor excitement even as the stock remains near multi-year lows.

The company also expanded its ecosystem through new deals and key partnerships. ServiceNow launched a zero-copy data connector with Cloudera to support AI workflows, and BigPanda announced a new build partnership with the platform. A previously reported $1.2 billion cloud contract with Google, as noted by Bloomberg, further demonstrates the scale of enterprise demand. So the business momentum is strong even as the stock price tells a different story.

Investors are balancing excitement about AI with caution about valuations and macro risk. NOW stock now trades at a forward price-to-earnings ratio (P/E) of around 21x, far below its five-year historical average of over 100x. That compression has created what some investors see as a compelling entry point.

Here’s why ServiceNow stock could deliver strong returns as its AI platform scales toward a $32 billion revenue target.

What the Model Says for NOW Stock

We analyzed the upside potential for ServiceNow stock using valuation assumptions based on its AI enterprise platform expansion, high-margin subscription revenue growth, and improving operating leverage as the business scales toward its $32 billion ambition.

Based on estimates of around 20% annual revenue growth, 33.2% operating margins, and a normalized P/E multiple of 21.2x, the model projects ServiceNow stock could rise from $92 to around $147 per share.

That would be a 60% total return, or an annualized return of around 19% over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for NOW stock:

1. Revenue Growth: 20%

ServiceNow delivered Q1 2026 revenue of $3.77 billion, growing around 22% year over year. The company beat consensus estimates and showed strength across North America, EMEA, and Asia-Pacific. Its Now platform is gaining adoption among large enterprise customers in government, healthcare, and financial services. Management has set a $32 billion revenue target by 2030.

Based on analysts’ consensus estimates, we used around 20% annual revenue growth. This reflects the company’s expanding AI product suite and its ability to upsell existing customers to higher-value contracts while also adding new enterprise logos globally. Acquisitions are also adding meaningful revenue optionality.

The $2.85 billion deal for Moveworks and the deal for Data. World expands the company’s AI capabilities in enterprise automation. So revenue should grow both organically and through targeted acquisitions, and both channels support the 20% growth assumption over the forecast horizon.

2. Operating Margins: 33.2%

ServiceNow carries one of the highest gross margins in enterprise software at around 76.6%. The business is highly scalable because it sells subscriptions with very low incremental delivery costs. AI is also being used internally to reduce operational expenses and improve service efficiency across the platform.

Based on analysts’ consensus estimates, we used 33.2% operating margins. This reflects improvement from current reported levels as AI investments begin generating efficiency gains. The company has guided for continued margin expansion as its product suite matures and R&D costs grow more slowly than revenue over time.

The company generated an operating cash flow of $1.67 billion in Q1 2026 alone. So the business already produces substantial cash, and margin expansion should further accelerate free cash flow generation as revenue scales toward the $32 billion goal.

3. Exit P/E Multiple: 21.2x

ServiceNow currently trades at a forward P/E of around 21x, a dramatic compression from its five-year average of nearly 60x. The multiple reflects macro headwinds, interest rate uncertainty, and concerns about enterprise IT spending cycles. But the business growth profile remains among the strongest in the software sector.

Based on analysts’ consensus estimates, we maintained a 21.2x exit P/E. This is a conservative assumption relative to the company’s historical trading range but accounts for a prolonged valuation reset period. It implies investors are buying the business at a significant discount to prior years.

If execution stays on track and AI enterprise budgets recover, the exit multiple could expand meaningfully above 21x. So the around 19% annualized return could represent a conservative floor for patient investors who believe in the company’s long-term AI ambitions.

Build your own Valuation Model to value any stock (It’s free!) >>>

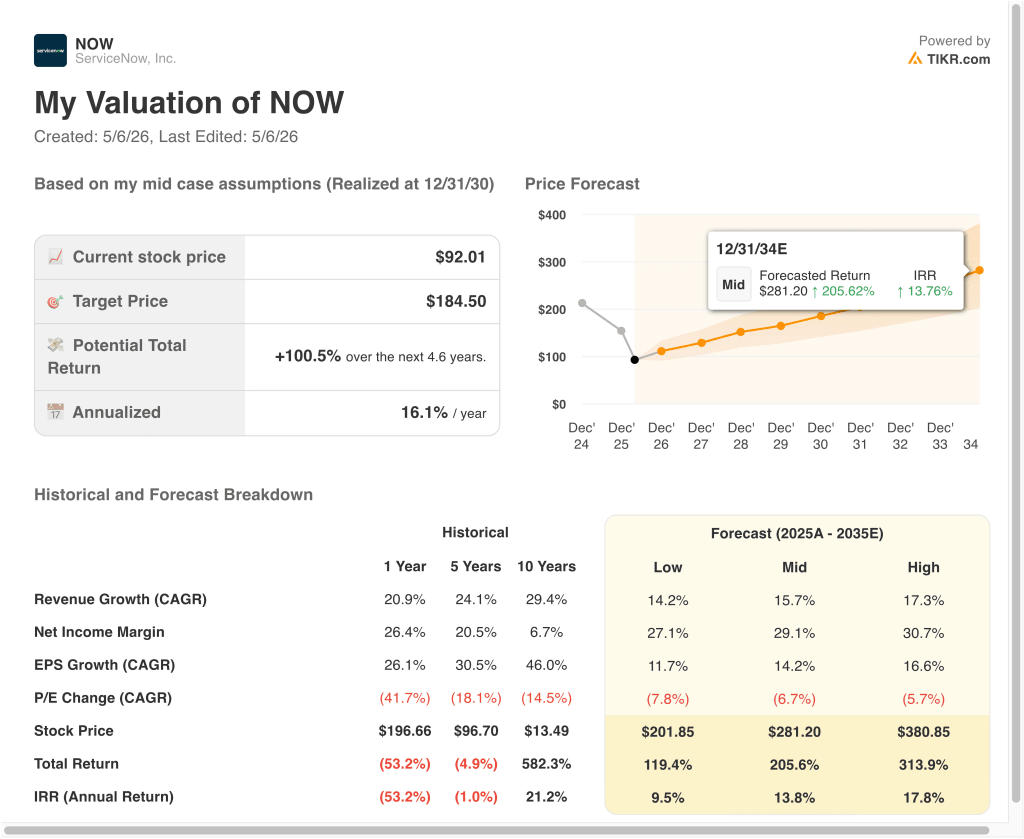

What Happens If Things Go Better or Worse?

Different scenarios for NOW stock through 2030 show varied outcomes based on AI platform adoption and enterprise revenue growth rates (these are estimates, not guaranteed returns):

- Low Case: AI spending disappoints and revenue growth moderates to around 14% annually → around 10% annual returns

- Mid Case: AI platform scales well, and the company executes on its $32 billion revenue goal → around 14% annual returns

- High Case: Rapid AI enterprise adoption and meaningful multiple recovery drive outperformance → around 18% annual returns

Going forward, ServiceNow’s ability to convert its AI ambitions into durable recurring subscription revenue will determine the stock’s trajectory. The business is already growing fast and generating strong cash flow, so the long-term setup remains compelling even at conservative assumptions. But investors should watch closely for signals that enterprise AI budgets are translating into sustainable ServiceNow contract wins rather than short-term platform trials.

See what analysts think about NOW stock right now (Free with TIKR) >>>

Should You Invest in ServiceNow?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NOW, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NOW alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze ServiceNow stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!