Key Takeaways:

- CRH plc reported Q1 2026 revenue of $7.4B, up 9% year over year, and completed a $300M share buyback phase, per Reuters.

- The company sold Oldcastle Lawn and Garden to Pacific Avenue Capital for more than $1.1B, sharpening its focus on core construction materials.

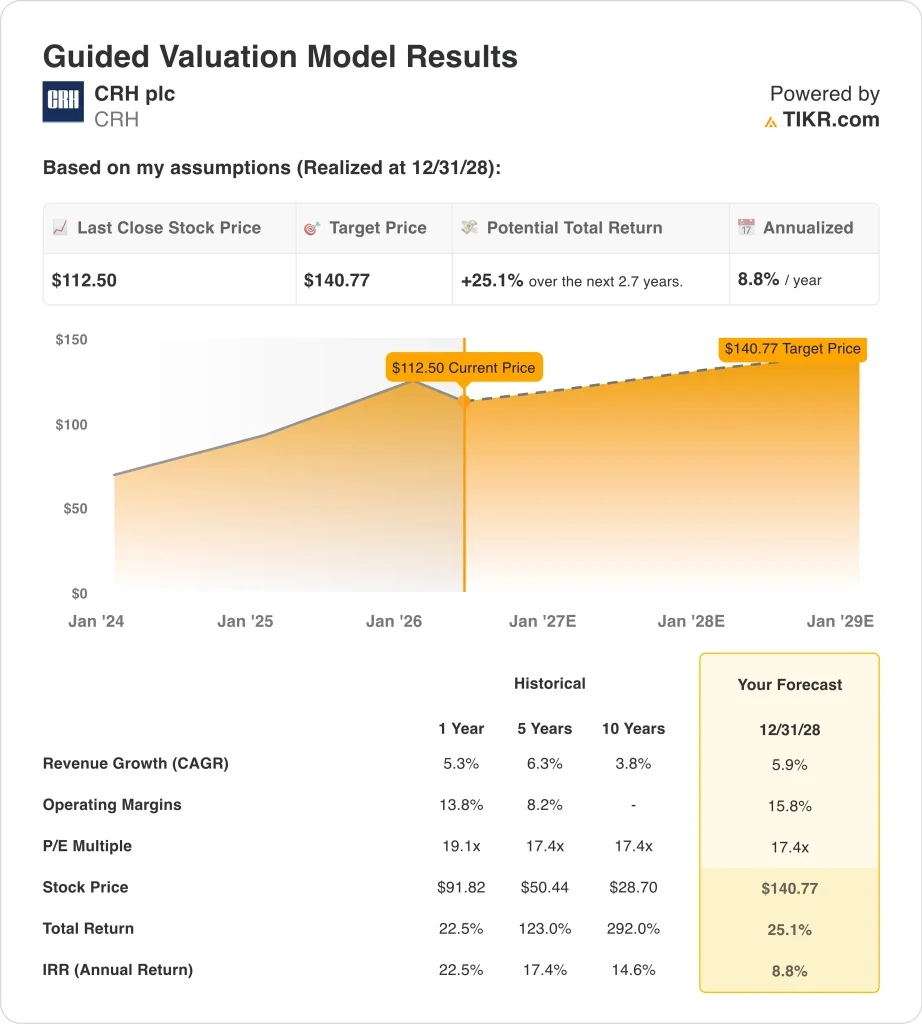

- CRH stock trades near $113, around 14% below its 52-week high of $132, while analysts hold a consensus price target of $142.

- The model projects CRH could rise from $113 to around $141 per share by the end of 2028, based on 5.9% revenue growth, 15.8% operating margins, and a 17.4x P/E multiple.

- That would represent a 25.1% total return, or 8.8% annualized over the next 2.7 years.

What Happened?

CRH plc (CRH) posted Q1 2026 revenue of $7.4B, a 9% increase year over year, per Reuters. The company reported a seasonal net loss of around $0.2B, which widened from the prior year. Construction companies typically report losses in the first quarter because winter months see much lower building activity across North America. But the revenue growth signal is encouraging for the full-year outlook.

CRH is one of the world’s largest building materials companies, manufacturing and distributing products including cement, aggregates, asphalt, and ready-mixed concrete. The company operates primarily in North America, which now accounts for a large majority of its profits.

CRH significantly expanded its U.S. presence through acquisitions and organic growth over the past decade. And it moved its primary listing from Dublin to the New York Stock Exchange in 2023, reflecting its growing North American focus.

The company made two significant portfolio moves in early 2026. First, CRH announced plans to delist from the London Stock Exchange (LSE), simplifying its corporate structure and concentrating on its NYSE listing.

Second, it agreed to sell Oldcastle Lawn and Garden to Pacific Avenue Capital for over $1.1B. These moves reflect management’s strategy to concentrate capital in its highest-margin infrastructure materials business.

CRH was added to the S&P 500 in December 2025, which brought new index-based institutional demand for the stock. But CRH has since pulled back around 11% year to date, reflecting broader market uncertainty and concerns about U.S. construction spending trends.

Here’s why CRH stock could still deliver moderate returns through 2028 as infrastructure spending supports long-term demand for its core materials.

What the Model Says for CRH Stock

We analyzed the upside potential for CRH stock based on its dominant position in North American construction materials, continued U.S. infrastructure investment from federal programs, and a track record of margin expansion through disciplined acquisition integration.

Based on estimates of 5.9% annual revenue growth, 15.8% operating margins, and a normalized P/E multiple of 17.4x, the model projects CRH stock could rise from $113 to around $141 per share.

That would be a 25.1% total return, or an 8.8% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CRH stock:

1. Revenue Growth: 5.9%

CRH grew revenue 9% year over year in Q1 2026 and 5.3% on a trailing one-year basis. The U.S. Infrastructure Investment and Jobs Act continues to drive multi-year demand for aggregates, cement, and asphalt used in roads, bridges, and highways. CRH is one of the primary suppliers for these types of large-scale public infrastructure projects.

The company completed the acquisition of Eco Material Technologies in 2025, adding supplementary cementitious materials to its portfolio. This acquisition expands CRH’s exposure to lower-carbon construction solutions, which are becoming more important in public infrastructure contracts. Geographic concentration in the U.S. continues to improve, providing exposure to the world’s most resilient construction market.

Based on analysts’ consensus estimates, we used 5.9% annual revenue growth. This reflects sustained infrastructure spending from federal programs and steady private sector construction activity, balanced against the typical cyclicality of the building materials sector.

2. Operating Margins: 15.8%

CRH’s trailing EBIT margin is near 14.0%, and management has targeted margin expansion as the company shifts its focus toward higher-value infrastructure materials. The company raised the lower end of its 2025 earnings forecast in August 2025, citing positive demand and improving margins across all product lines.

CRH has a strong track record of margin improvement through acquisition integration. The company typically acquires regional building materials businesses and drives cost synergies by integrating supply chains, logistics, and procurement. U.S. backlogs have been growing in both volume and margin across product categories, per management commentary from Reuters.

Based on analysts’ consensus estimates, we use 15.8% operating margins. This reflects the expected benefit of a higher-value infrastructure product mix and ongoing efficiency gains from integration, balanced against input cost pressures in energy and labor.

3. Exit P/E Multiple: 17.4x

CRH currently trades at a trailing LTM P/E of 20.8x. The next twelve months’ P/E is around 18.8x, reflecting near-term earnings growth expectations. A 17.4x exit multiple represents a slight discount to both current levels and the long-term peer average for the sector.

Building materials companies like Vulcan Materials and Martin Marietta trade at higher multiples in the U.S. because of their aggregate market dominance. CRH’s global scale and diversified product range justify a premium relative to pure-play regional operators, but investors also factor in its ongoing corporate simplification.

Based on analysts’ consensus estimates, we maintain a 17.4x exit multiple. This reflects CRH’s infrastructure-driven revenue quality and expanding U.S. presence, balanced against cyclical exposure and ongoing structural simplification of the business.

Build your own Valuation Model to value any stock (It’s free!) >>>

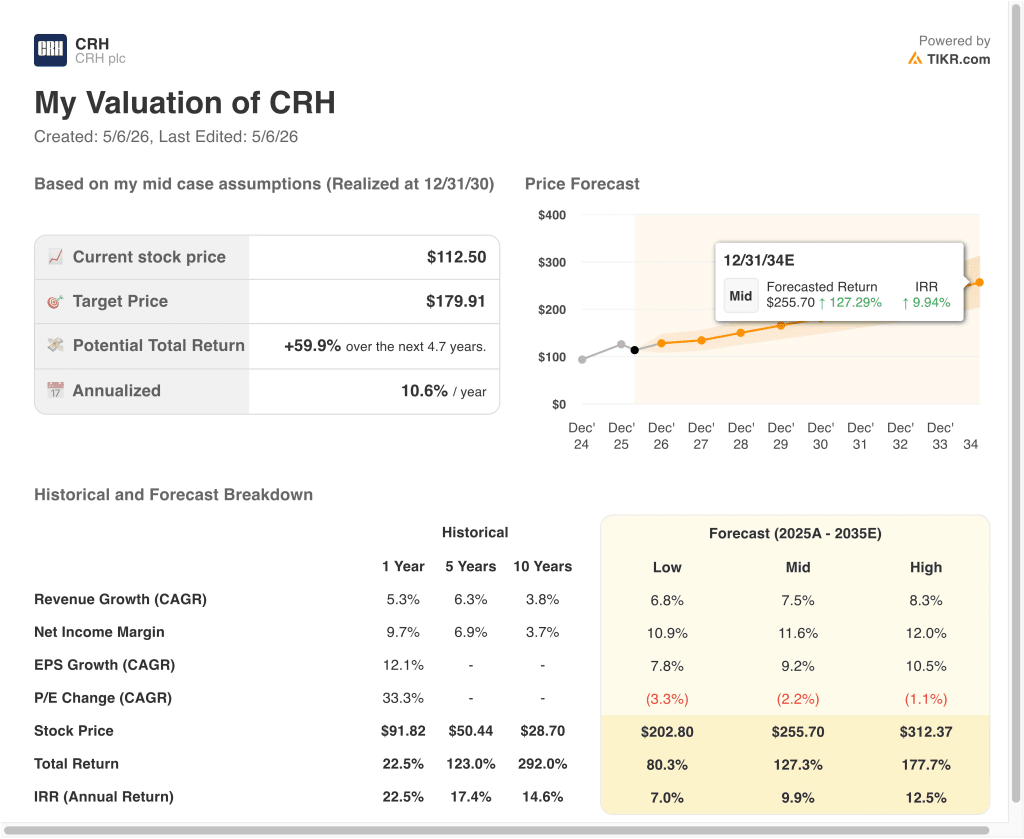

What Happens If Things Go Better or Worse?

Different scenarios for CRH stock through 2035 show varied outcomes based on U.S. infrastructure spending levels, construction volumes, and margin execution (these are estimates, not guaranteed returns):

- Low Case: Infrastructure spending slows, and the construction cycle weakens → 7.0% annual returns

- Mid Case: Steady federal infrastructure demand supports volumes and pricing → 9.9% annual returns

- High Case: Accelerating U.S. construction activity and strong margin expansion → 12.5% annual returns

Going forward, CRH is well-positioned to benefit from multi-year U.S. infrastructure investment under the Infrastructure Investment and Jobs Act. The near-term model suggests around 8.8% annualized returns, just below the 10% threshold often linked to clearly compelling setups.

For investors with a longer horizon, the high case scenario suggests up to 12.5% annual returns if CRH executes on its simplification strategy.

See what analysts think about CRH stock right now (Free with TIKR) >>>

Should You Invest in CRH plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CRH, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CRH alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze CRH stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!