Key Takeaways:

- HCA Healthcare reported Q1 2026 revenue of $19.1B, roughly matching the IBES consensus, while adjusted profit topped estimates despite a weaker flu season, per Reuters.

- HCA stock trades near $429, down around 23% from its 52-week high of $557, while analysts hold a consensus price target of $513.

- That would represent a 29.7% total return, or 10.3% annualized over the next 2.7 years.

What Happened?

HCA Healthcare, Inc. (HCA) beat adjusted profit estimates in Q1 2026, but the stock sold off after the company reported lower inpatient volumes tied to a weaker flu season. Revenue came in at $19.1B, essentially matching the IBES consensus of $19.1B, per Reuters. Adjusted profit topped estimates, showing the underlying business stayed resilient. But investors reacted negatively to the softer volume numbers.

HCA is the largest investor-owned hospital system in the United States. The company operates more than 180 hospitals and around 2,000 care sites across 20 states and the United Kingdom. Revenue comes primarily from inpatient and outpatient care, including surgeries, emergency services, and intensive care. HCA earns the majority of its revenue through Medicare, Medicaid, and private insurance reimbursements.

Hospital volumes are a key metric for HCA and for the sector broadly. A weaker flu season means fewer inpatient admissions, and that directly reduces revenue in a given quarter. Investors watch these volume trends closely because they can signal whether underlying demand is softening. But management has consistently expanded profit margins, even during lower-volume periods, through disciplined cost management.

Despite the post-earnings stock drop, HCA’s fundamentals remain intact. The stock now trades near $429, down around 23% from its 52-week high of $557. Analysts maintain a consensus price target near $513, implying meaningful upside from current levels. And the company continues to invest in capacity expansion and technology to grow market share.

Here’s why HCA stock could recover and deliver strong returns through 2028 as patient volumes normalize and margins expand.

What the Model Says for HCA Stock

We analyzed the upside potential for HCA Healthcare stock based on its dominant position in U.S. hospital markets, continued expansion of outpatient capacity, and improving profitability through cost efficiency and favorable commercial insurance mix.

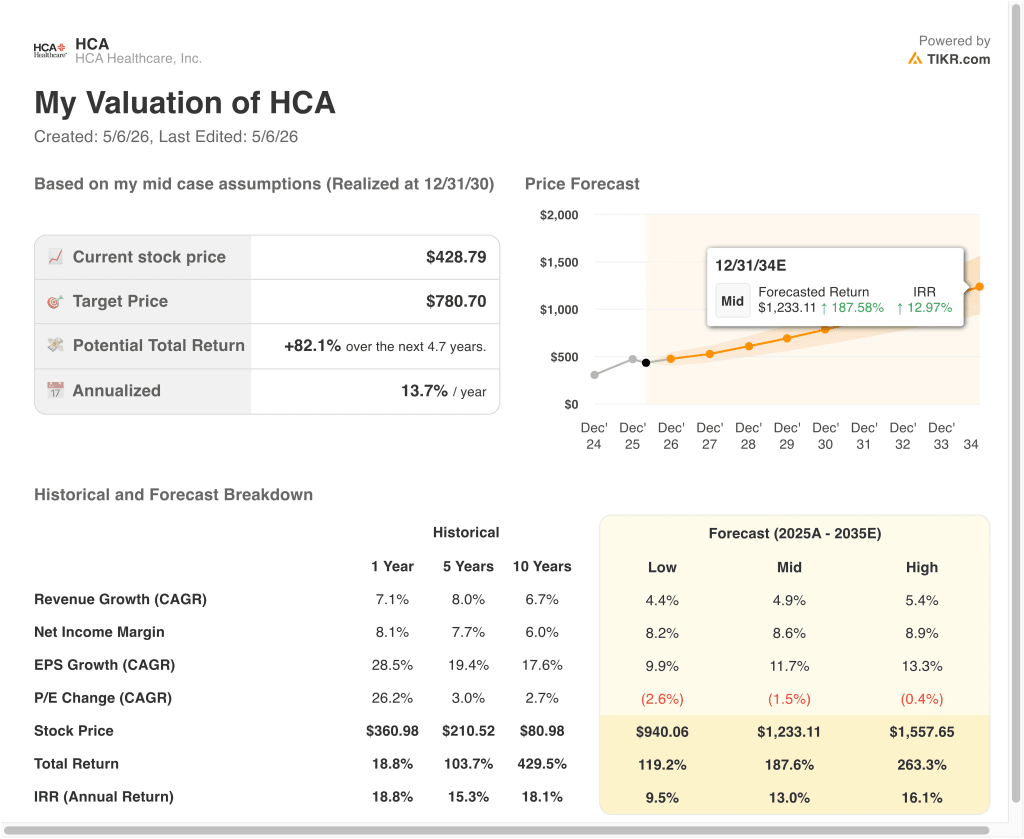

Based on estimates of 4.0% annual revenue growth, 15.0% operating margins, and a normalized P/E multiple of 13.9x, the model projects HCA Healthcare stock could rise from $429 to around $556 per share.

That would be a 29.7% total return, or a 10.3% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for HCA stock:

1. Revenue Growth: 4%

HCA has grown its revenue steadily. The one-year revenue compound annual growth rate (CAGR) is 7.1%, and the five-year rate is 8.0%, reflecting strong volume trends and consistent pricing power with insurance payers. The company has beaten revenue estimates in multiple consecutive quarters, as seen in both Q3 2025 and Q1 2026.

Outpatient care is a growing segment for HCA, and it carries different demand dynamics than traditional inpatient hospital stays. As more procedures shift to ambulatory surgery centers and outpatient clinics, HCA is investing to capture that volume. This shift supports revenue growth even when flu-related inpatient admissions temporarily slow.

Based on analysts’ consensus estimates, we used 4.0% annual revenue growth. This reflects a moderation from recent rates as the post-pandemic rebound effect fades, but accounts for HCA’s continued investment in new hospital capacity and outpatient expansion.

2. Operating Margins: 15%

HCA’s trailing operating margin is around 15.7%, and the five-year average has hovered near 14.2%. The company has demonstrated strong cost discipline, particularly in labor, which is the single largest operating expense for hospital systems. Staffing improvements after the pandemic-era nurse shortage have also helped margins recover meaningfully.

Medicare reimbursement rates and private insurance negotiations are central to margin management for HCA. The company has benefited from favorable rate updates and a strong commercial payer mix in recent years. But regulatory risk around Medicaid funding and potential reimbursement policy changes remains an important variable.

Based on analysts’ consensus estimates, we use 15.0% operating margins. This reflects HCA’s ongoing ability to manage labor costs and payer negotiations, balanced against the risk of adverse reimbursement changes.

3. Exit P/E Multiple: 13.9x

HCA currently trades at a trailing P/E of 14.75x, and the next-twelve-months P/E is around 13.9x. Hospital operators typically trade at lower multiples than the broader market because of regulatory exposure and reimbursement risk. The current multiple is consistent with HCA’s historical range and its peer group.

Competitors like Universal Health Services also trade in a similar valuation band. A 13.9x exit multiple reflects a fair but conservative assumption for where HCA’s earnings multiple could settle by 2028. The forward P/E reflects expected earnings growth over the next two years.

Based on analysts’ consensus estimates, we maintain a 13.9x exit multiple. This accounts for the company’s stable earnings growth trajectory, strong free cash flow, and ongoing capital return program through buybacks and dividends.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for HCA stock through 2035 show varied outcomes based on hospital volume trends, insurance reimbursement rates, and margin execution (these are estimates, not guaranteed returns):

- Low Case: Volume growth disappoints, and reimbursement headwinds intensify → 9.5% annual returns

- Mid Case: Steady volume recovery and margin expansion as outpatient mix grows → 13.0% annual returns

- High Case: Accelerating surgical volumes and a favorable policy environment → 16.1% annual returns

Going forward, HCA’s near-term performance will depend on whether inpatient volumes recover as flu-related weakness fades. Analysts see $513 as fair value, suggesting the market may be pricing in more risk than fundamentals currently justify. Regulatory and reimbursement policy changes remain the key risks to watch for HCA stock.

See what analysts think about HCA stock right now (Free with TIKR) >>>

Should You Invest in HCA Healthcare?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HCA, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track HCA alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze HCA Healthcare stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!