Key Stats for NVIDIA Stock

- Current Price: $220.78

- Target Price (Mid): ~$495

- Street Target: ~$270

- Potential Total Return: ~124%

- Annualized IRR: ~19% / year

- Earnings Reaction: -5.46% (February 25, 2026)

- Max Drawdown: 20.22% (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

NVIDIA Corporation (NVDA) has spent most of 2026 as the world’s most valuable company, carrying one uncomfortable question: what happens to a business priced for dominance when its second-largest market has been effectively closed by government order? That question got more interesting this week.

On Tuesday, President Trump personally called Jensen Huang, Founder and CEO of NVIDIA, and asked him to fly to Alaska to board Air Force One, joining the U.S. delegation heading to Beijing for a summit with Chinese President Xi Jinping. Huang had initially been left off the list. Semafor reported that his exclusion was deliberate, intended to avoid “awkward conversations” around chip sales. The last-minute reinstatement made the signal louder. NVDA shares jumped approximately 2.4% premarket on the news, bringing the stock to $220.78, near its 52-week high of $223.75.

Two questions are driving the trade. Can the China overhang that has compressed NVDA’s valuation begin to lift? And does it even matter when Q1 FY2027 earnings land on May 20?

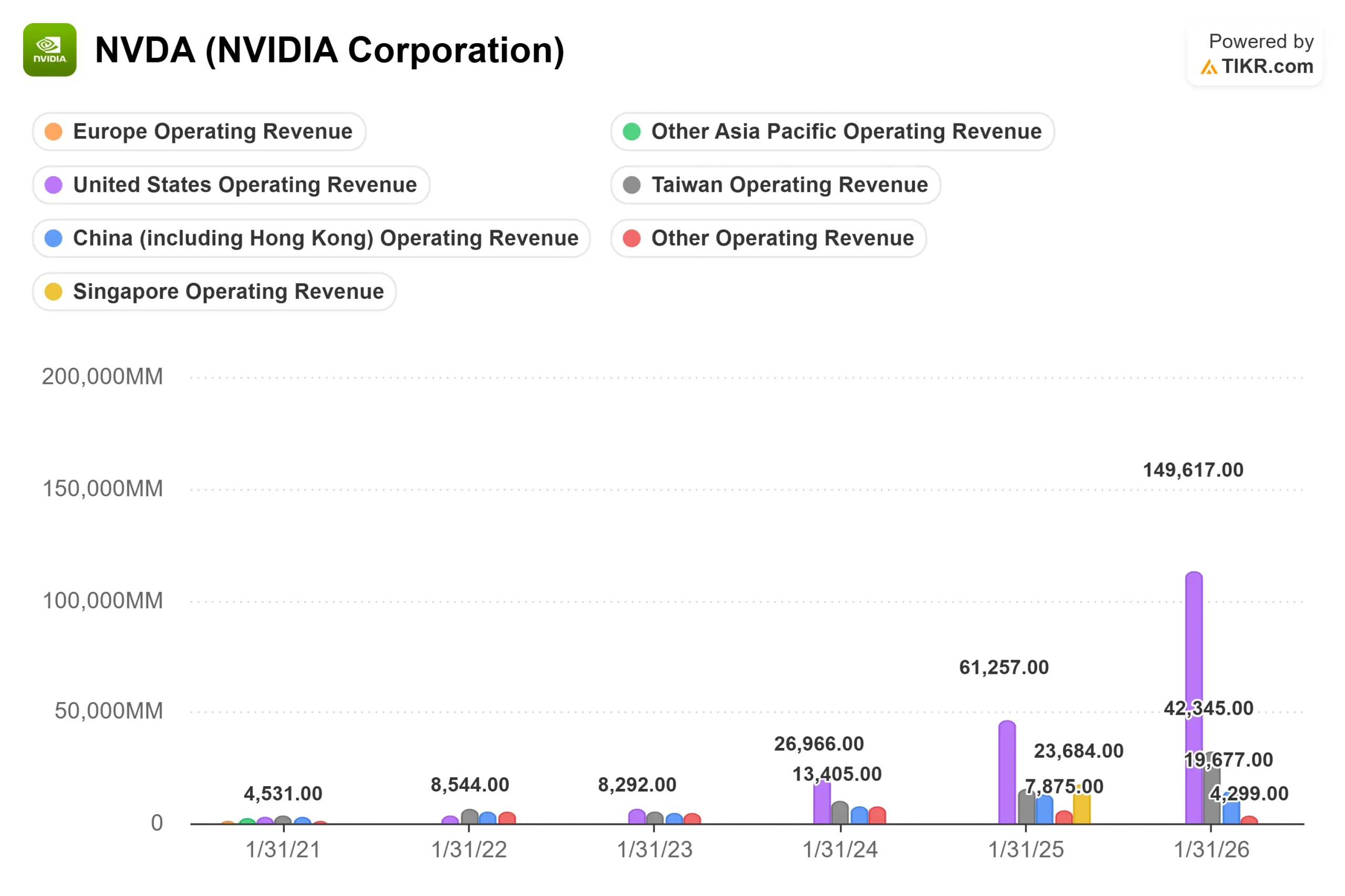

The China Problem, in Numbers

NVIDIA’s China exposure has been measurable and painful. China and Hong Kong contributed $17.1 billion to revenue in fiscal year 2025, per TIKR segment data. That figure is now effectively zero. Management’s Q1 FY2027 guidance of approximately $78 billion explicitly excluded all China data center compute revenue, and Huang has estimated the total Chinese AI chip market at roughly $50 billion annually.

Huang’s presence in Beijing does not guarantee a policy change. Any modification to export control thresholds requires a regulatory process and time. What it signals is that the Trump administration is treating AI chip access as a negotiating variable, and NVIDIA is at the table. Every analyst model currently assumes zero China data center revenue. Any reopening is pure upside against a base case that already prices in total exclusion.

See historical and forward estimates for NVIDIA stock (It’s free!) >>>

What the $1 Trillion Order Book Says About the Business Without China

The underlying business is already compounding without China. At the GTC 2026 analyst session on March 18, Huang was direct: “We have strong confidence and visibility of $1 trillion plus of Blackwell plus Rubin” in purchase orders through end-2027. He was explicit that the figure excludes Rubin Ultra, Feynman, and Groq stand-alone entirely, making it a floor rather than a ceiling.

TIKR’s estimates show FY2027 revenue at approximately $372 billion, up around 72% year-over-year. FY2028 consensus sits at approximately $488 billion. Both figures assume zero China data center revenue.

The driver behind that growth is what Huang called the third AI inflection point: agentic systems. He framed it at GTC this way: “What used to be a thing for engineers is when you come to work, they give you a laptop. Now, when you come to work, they give you a laptop and tokens.” His argument is that the GPU cluster has become manufacturing equipment, where the right measure is tokens per second per watt rather than chip price. It is not just a marketing argument. NVIDIA’s trailing twelve months gross margin sits at 71.1%, and LTM free cash flow reached $96.7 billion in fiscal 2026. CFO Colette Kress, Executive Vice President and CFO, told analysts at the same GTC session that NVIDIA plans to return approximately 50% of free cash flow to shareholders through buybacks and dividends.

Why the Stock Trades at a Discount and What Would Change That

At $220.78, NVDA trades at 26.42x next twelve months P/E and 21.15x NTM EV/EBITDA. Per TIKR’s Competitors page, Broadcom trades at 31.17x NTM P/E, ASML at 37.40x, and Marvell Technology at 43.22x. NVIDIA, which generated more free cash flow than those three peers combined in fiscal 2026, carries the lowest forward multiple in the group. The discount has one name: China. Remove it, and the compression rationale largely disappears.

The risk that keeps it in place is not only geopolitical. Morgan Stanley analysts project the five largest hyperscalers will increase capex by nearly 80% to approximately $805 billion in 2026, followed by around 39% growth to $1.1 trillion in 2027. If that spending cycle peaks before Vera Rubin Ultra and the next product generation reaches volume, revenue estimates move lower, and the multiple compresses from both directions. Huang’s counterargument at GTC was direct. When asked which segment of token generation would grow fastest, he said, “They’re all going to grow really fast at the moment. They’re all growing exponentially.”

Wells Fargo analyst Aaron Rakers has set a target of around $315, citing durable AI demand through 2027, while the Street’s mean of around $270 implies roughly 22% upside with no China recovery assumed.

See how NVIDIA performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $220.78

- Target Price (Mid): ~$495

- Potential Total Return: ~124%

- Annualized IRR: ~19% / year

See analysts’ growth forecasts and price targets for NVIDIA stock (It’s free!) >>>

The TIKR mid-case model prices NVDA at approximately $495 by January 31, 2031, for a total return of around 124% and an annualized IRR of approximately 19%. Two revenue drivers anchor the model: sustained hyperscaler infrastructure buildout through the Blackwell-to-Vera Rubin transition, and NVIDIA’s expanding non-hyperscaler segment covering enterprise on-premises deployment, regional sovereign clouds, and early physical AI. The margin driver is operating leverage, with the model projecting net income margins of around 51%, a normalization from today’s 57% as manufacturing and ecosystem investment scale. The primary risk is multiple compression: if hyperscaler compound annual growth rate in capex slows materially before the next product cycle is ready, or a competitor matches NVIDIA’s tokens-per-second-per-watt efficiency at lower cost, the upside compresses, and the timeline extends.

Conclusion

The thesis is due on May 20. Q1 FY2027 earnings will show whether the $78 billion guide was a floor or a ceiling. Data center revenue needs to hold at a level consistent with management’s guidance for the Vera Rubin ramp story to stay intact. A meaningful miss without a China explanation would confirm the hyperscaler slowdown bears have been flagging all year.

Beijing adds a second layer. If the summit produces any framework around AI chip licensing, even a narrow one, it would be the first concrete sign that $17 billion in lost annual revenue has a path back. Watch for any Commerce Department or BIS language in the days following the summit. The absence of a statement is also data. May 20 is the first answer. Beijing is the second.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in NVIDIA?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NVIDIA, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NVIDIA alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!