Key Stats for United Airlines Stock

- 52-Week Range: $72 to $118

- Current Price: $96.62

- Street Mean Target: ~$132

- TIKR Target Price (Mid): ~$137

- TIKR Annualized IRR (Mid): ~8% per year

- Q1 2026 Adjusted EPS: $1.19 (beat $1.08 estimate)

- Q1 2026 Revenue: $14.6B (up ~11% year over year)

- FY2026 Adjusted EPS Guidance: $7 to $11

Value your favorite stocks like UAL with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

How a Fuel Cost Shock Sent UAL Down 18% in 2026

The story of United Airlines (UAL) in 2026 is a study in the distance between a business and its stock price.

United reported genuinely strong Q1 2026 results. Revenue came in at $14.6 billion, up 11% year over year. Adjusted EPS of $1.19 beat the consensus estimate by double digits. CEO Scott Kirby reiterated the vision he has been building toward for years, describing United as “becoming a loyalty business that runs an airline.”

That framing reflects something real: MileagePlus now has more than 130 million members, generating revenue that is structurally more resilient than ticket sales alone.

At the same time, management cut its full-year 2026 adjusted EPS guidance from $12 to $14 down to $7 to $11, citing roughly $340 million in added fuel costs tied to disruptions in the Strait of Hormuz. That guidance cut overshadowed the earnings beat, and the stock has spent much of 2026 digesting the uncertainty, falling roughly 18% year to date.

The EPS chart captures what United has actually accomplished. The company went from losing nearly $14 per share in 2021 to earning just over $10 in each of the last three years. The 2026 estimate steps back to around $9 on the fuel headwind, but consensus then calls for a sharp recovery: around $14 by 2027 and approaching $17 by 2028 as costs normalize and the premium strategy keeps compounding.

The dip looks cyclical, not structural. When Kirby was asked about a recessionary scenario earlier this year, his response was pointed: “When times get tough, more customers migrate to you.” That is not a comment a management team makes if the premium strategy isn’t working.

See analysts’ growth forecasts and price targets for UAL stock (It’s free!) >>>

Why Wall Street Stayed Bullish After United Cut Guidance

Wall Street has stayed broadly constructive despite the guidance cut. The consensus is firmly Buy, with an average price target near $132. UBS raised its target to around $139 following Q1, citing strength in the Newark hub and firm premium-cabin demand. Wolfe Research trimmed its target modestly but kept its rating at Outperform, reflecting the view that the fuel headwind is temporary rather than a structural impairment.

The stock trades at roughly 10 times forward earnings, near the low end of its historical range and below where Delta commands a premium for similar premium positioning. Closing that gap does not require anything heroic: it requires fuel costs to normalize and premium demand to hold, both of which the current data support.

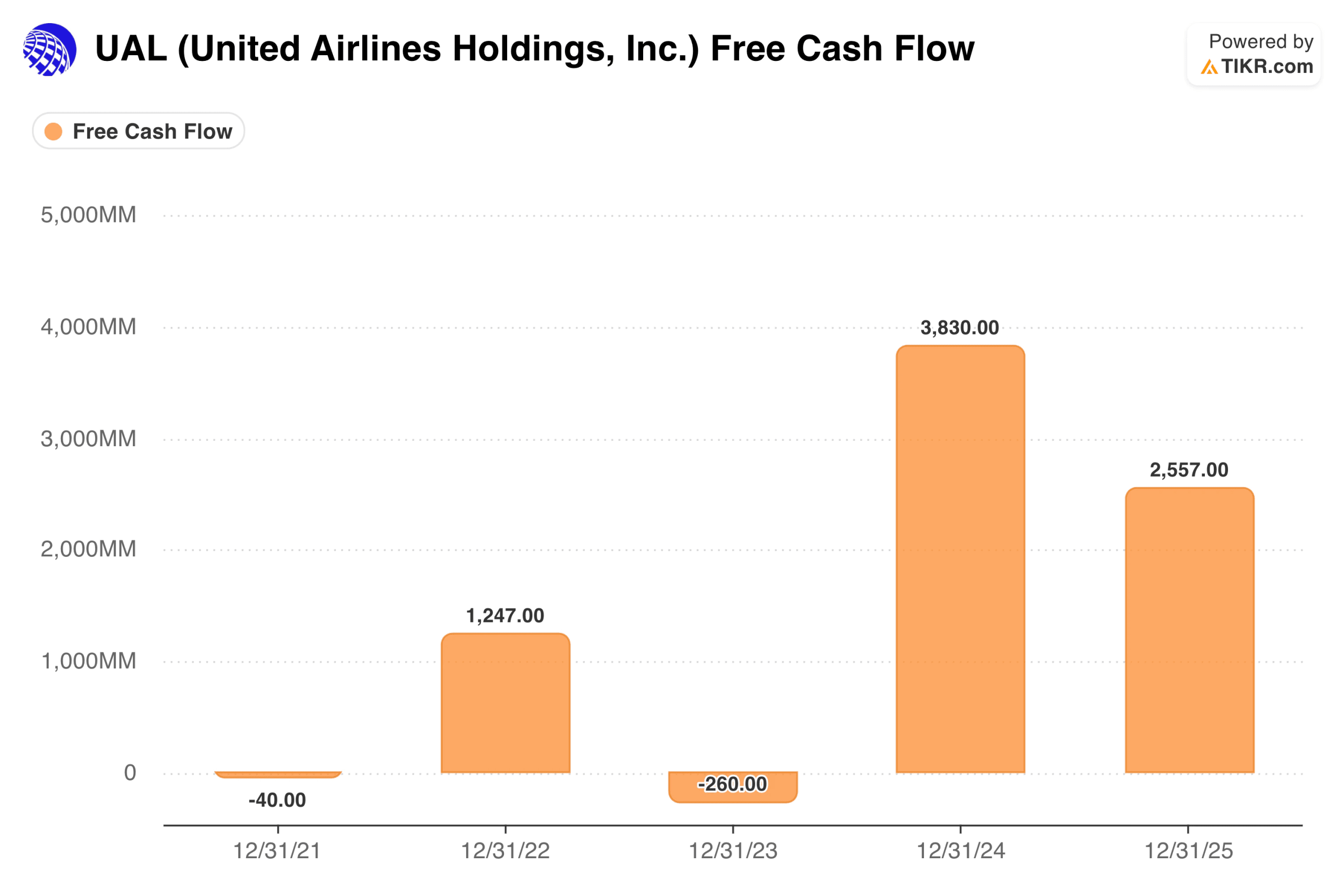

The Free Cash Flow Trajectory That Makes United Hard to Dismiss

United was essentially breakeven on FCF in 2021. By 2022, it generated $1.2 billion. It dipped into negative territory in 2023 as the company accelerated fleet investment and the Polaris cabin expansion. Then in 2024, FCF jumped to $3.8 billion, one of the strongest single-year prints in the airline’s history, before moderating to $2.6 billion in 2025.

Airlines are routinely dismissed as perpetually capital-intensive, low-return businesses. That FCF trajectory tells a different story. The heavy investment cycle is largely behind it; the premium-cabin buildout has been executed, and the loyalty flywheel is operating at scale. The capital cycle is shifting from investment toward harvest. The Atlantic segment generated $11.6 billion in revenue in 2025 and the Pacific segment generated $6.9 billion, both growing year over year on routes where United’s product is difficult for competitors to replicate quickly.

Value UAL instantly (Free with TIKR) >>>

What the TIKR Model Implies at the Current Price

The TIKR model targets around $137 per share in the mid case, implying a total return of roughly 42% from the current price over about 4.6 years, or about 8% annually.

The assumptions are not aggressive. Revenue growth of around 1.5% per year is the base case, well below recent history. Net income margins of around 7% reflect current profitability without assuming expansion. EPS growth of around 4.5% per year reflects modest improvement and some share count reduction.

The model is pricing in a business that keeps doing roughly what it has been doing, not a heroic recovery. Notably, the low case, which targets around $117, still implies meaningful upside from where the stock sits today.

The Case for United: Premium Positioning, Loyalty, and a Temporary Headwind

The premium positioning is durable. Polaris and Premium Plus are not marketing exercises; they represent a structural shift in how United monetizes its highest-demand seats. New tiered fare buckets that let travelers pay for flexibility, bags, and lounge access further extend that monetization. On the routes that matter most, United competes on product quality, not price.

The loyalty flywheel generates resilient revenue. MileagePlus produces co-branded credit card revenue, partner redemptions, and recurring engagement that smooths out the cyclical swings in ticket sales. It scales with membership and engagement rather than seat capacity alone.

The fuel headwind is event-driven, not structural. The guidance cut reflects a specific geopolitical cost shock, not a change in United’s cost structure or competitive position. If fuel normalizes toward 2025 levels, the consensus path to around $14 in EPS by 2027 becomes a reasonable base case.

The Risks: Wide Guidance, Leverage, and a Fuel Cost That Has to Cooperate

The guidance range is wide. A full-year range of $7 to $11 covers a lot of outcomes. At the low end, the current stock price is not obviously cheap.

Leverage remains elevated. A debt-to-equity ratio above 2 amplifies demand shocks, and airlines have high fixed costs and thin liquidity buffers.

The EPS recovery requires fuel costs to cooperate. Management can control capacity and costs on the margin, but the path to around $14 in EPS by 2027 depends on that normalization playing out.

Is UAL Worth Buying at $97?

United Airlines is a macro-sensitive, capital-intensive business in an industry with thin margins and high fixed costs. The stock will move with fuel prices and geopolitical headlines, regardless of how well management is executing.

What the numbers show is that the execution has been real. FCF of $2.6 to $3.8 billion over the last two years, an EPS recovery from -$14 to over $10, premium-cabin yields that are measurably higher, and a loyalty program that continues to scale all represent genuine operational progress. The 2026 guidance cut reflects a cost shock, not a deterioration in business.

The TIKR mid-case target of around $137 at about 8% per year is not a dramatic return. But it comes against an entry point where the current price already reflects most of the near-term bad news. The low case still implies upside. And if the bull case materializes, with fuel normalizing and the premium strategy continuing to compound, the return is considerably better than the mid case suggests.

Based on what the company has actually delivered, the current price seems to be pricing in a worse outcome than the business deserves.

See analysts’ growth forecasts and price targets for UAL stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!