Key Stats

- Current price: $5 (May 12, 2026)

- Full-year FY2026 revenue: $5.0B, down 4% YoY

- Full-year FY2026 adjusted diluted EPS: $0.12

- Q4 FY2026 revenue: $1.2B, down 1% YoY

- Q4 FY2026 adjusted diluted EPS: ($0.03)

- FY2027 revenue guidance: down slightly (roughly flat ex-Curry brand exit)

- FY2027 adjusted diluted EPS guidance: $0.08 to $0.12

- FY2027 adjusted operating income guidance: $140M to $160M

- TIKR model price target: $10

- Implied upside: ~91%

Under Armour Earnings Breakdown

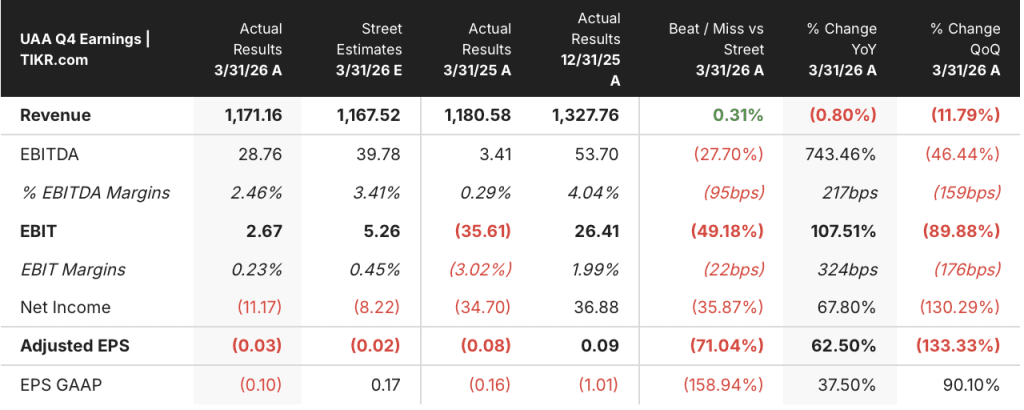

Under Armour stock (UAA) posted Q4 FY2026 revenue of $1.2B, down 1% year-over-year, alongside an adjusted diluted loss per share of ($0.03).

North America remained the primary drag, with revenue declining 7% in the quarter, driven by a decrease in wholesale and a slight decline in the direct-to-consumer business, according to CFO Reza Taleghani on the Q4 earnings call.

EMEA provided a partial offset, with revenue up 7%, though Taleghani noted approximately 3 points of that growth reflected shipment timing that shifted from Q4 into Q1.

APAC was the standout, with revenue up 13%, or 8% in constant currency, with growth across both direct-to-consumer and wholesale channels.

By channel, wholesale revenue declined 3%, while direct-to-consumer grew 5%, including 8% growth in owned and operated stores and flat e-commerce.

Gross margin declined 360 basis points on an adjusted basis to 43%, driven by 315 basis points of supply chain headwinds, of which approximately 260 basis points came from U.S. tariffs, according to Taleghani on the Q4 earnings call.

Adjusted SG&A decreased 14% to $503M in the quarter, primarily from lower marketing spend due to timing shifts and reduced incentive compensation.

Adjusted operating income for Q4 was $3M, while the adjusted diluted loss per share came in at ($0.03).

For the full fiscal year 2026, revenue declined 4% to $5.0B, with adjusted gross margin down 220 basis points to 46%, and full-year adjusted operating income of $107M, according to Taleghani on the Q4 earnings call.

Under Armour also disclosed it is expanding its previously announced restructuring plan, bringing the total anticipated cost to approximately $305M, with the plan now expected to be substantially complete by December 31.

On the balance sheet, inventory ended the year at $915M, down 3% year-over-year, while the company closed fiscal 2026 with $309M in cash and $605M in restricted investments earmarked to cover senior notes due this June, according to Taleghani on the Q4 earnings call.

For fiscal 2027, management guided revenue to decline slightly, noting that excluding the approximately 1-point drag from the Curry brand exit, the underlying trend is closer to flat.

Adjusted operating income for fiscal 2027 is expected in the range of $140M to $160M, which assumes approximately $70M of benefit from a refund of IEEPA tariffs expensed through the P&L in fiscal 2026, according to Taleghani on the Q4 earnings call.

Full-year FY2027 adjusted diluted EPS is expected in the range of $0.08 to $0.12.

For Q1 FY2027, management guided revenue down 2% to 3%, with Q1 expected to represent the weakest revenue performance of the year and growth rates improving progressively through the balance of fiscal 2027, according to Taleghani on the Q4 earnings call.

CEO Kevin Plank cited the brand’s back-to-back Boston Marathon victories with the Velociti Elite 3 as evidence that Under Armour makes pinnacle performance footwear, while acknowledging the company is not improving its bottom line fast enough and has no sacred cows in its approach to cost and assortment discipline.

Under Armour Stock: What the Financials Show

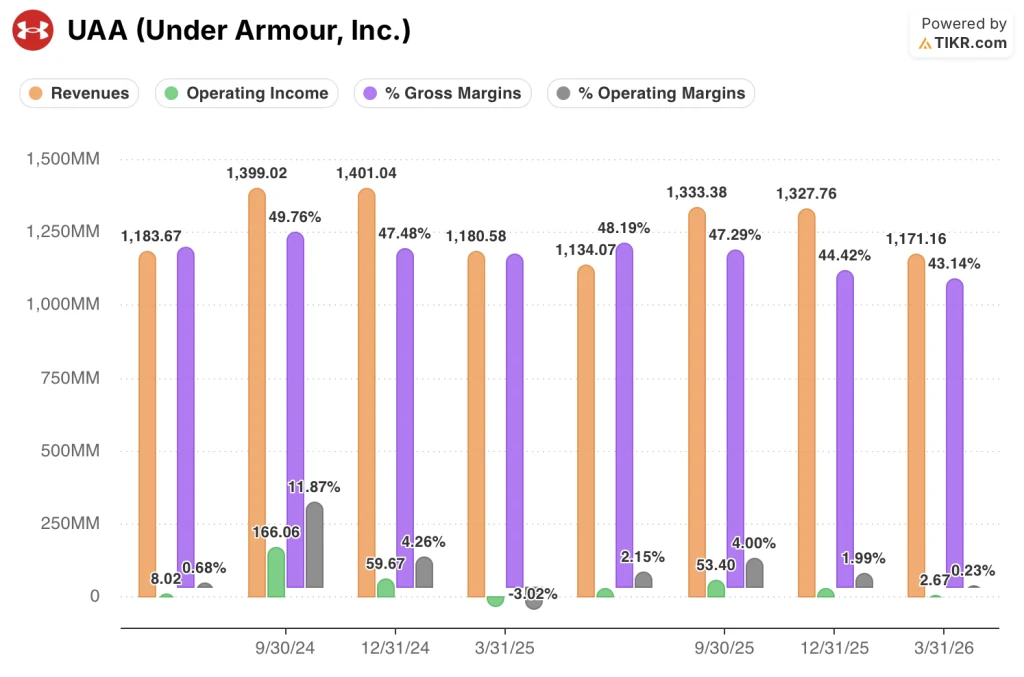

The income statement over the past eight quarters tells a consistent story of revenue under pressure, gross margin compression, and operating income hovering near zero.

Revenue peaked at $1.4B in September and December 2024, then decelerated steadily: $1.2B in March 2025, $1.1B in June 2025, $1.3B in September 2025, $1.3B in December 2025, and $1.2B in March 2026.

Gross margins followed a similarly difficult arc, compressing from 49.8% in September 2024 to 43.1% in the most recent quarter, with the steepest single-quarter decline coming between December 2025 (44.4%) and March 2026 (43.1%).

Operating income deteriorated sharply over the same period: $170M in September 2024 fell to $60M in December 2024, turned negative at ($40M) in March 2025, recovered modestly to $20M in June 2025 and $50M in September 2025, then declined again to $30M in December 2025 before landing at approximately zero in March 2026.

Operating margin in the most recent quarter came in at 0.2%, compared to 2.0% in December 2025 and 4% in September 2025, with the Q4 SG&A efficiency gains offset almost entirely by the gross margin compression from tariffs and promotional activity.

What Does the Valuation Model Say?

The TIKR mid-case model prices Under Armour stock at $9.62, implying roughly 91% upside from the current $5.03 price over the next 4.9 years, with an annualized return of approximately 14%.

The mid-case assumes a revenue CAGR of approximately 2.4% and a net income margin of 2.2%, both modest figures relative to Under Armour’s historical peak but reflective of a business still early in its margin recovery.

The model also embeds a P/E multiple compression assumption of -0.4% annually in the mid-case, meaning the return is driven almost entirely by earnings recovery rather than valuation re-rating, and the stock would still need the profitability turnaround to materialize on schedule to hit $9.62.

This earnings report does not materially strengthen the investment case in the near term: tariff headwinds clipped Q4 gross margin by 260 basis points, operating income for the year was $107M, and fiscal 2027 guidance for adjusted EPS of $0.08 to $0.12 implies the earnings recovery the model requires is still several years away.

The investment case for Under Armour stock is essentially unchanged: the model upside is real if management executes on margin recovery, but fiscal 2027 is a structurally limited year with earnings artificially supported by a one-time $70M tariff refund.

Whether Under Armour stock can justify the 91% model upside depends entirely on whether tariff-adjusted gross margin recovery materializes beyond the one-time FY2027 refund benefit.

What Has to Go Right

- Gross margin expands 220 to 270 basis points in fiscal 2027; excluding the 150-basis-point tariff refund, the underlying improvement of 70 to 120 basis points must hold through fiscal 2028 and beyond without a repeat one-time tailwind

- North American wholesale stabilizes as guided, with order books for fall 2026 showing early positive response per Plank on the Q4 earnings call, translating into a low-single-digit decline that does not worsen

- The $30M incremental marketing investment against the Bouncy Tee and core apparel franchises drives improved full-price sell-through, particularly in e-commerce, which Plank characterized as the brand’s most important traffic metric

- The Curry brand exit removes approximately 1 point of revenue drag from the base, improving the quality of the remaining revenue mix and supporting DTC margin improvement

What Could Still Go Wrong

- Fiscal 2027 adjusted operating income guidance of $140M to $160M assumes $70M of IEEPA tariff refund; strip that out and underlying adjusted operating income is in the $70M to $90M range, barely above fiscal 2026’s $107M on a like-for-like basis

- North America guided down in low-single digits in fiscal 2027, with Q1 North America expected to decline 7% to 8%, and Plank acknowledged the retail environment is cautious and consumer confidence remains uncertain

- The restructuring plan has expanded to approximately $305M total anticipated cost, adding further charges through December 2026 and extending near-term earnings pressure

- Middle East supply chain conflict is expected to generate approximately $35M in fiscal 2027 headwinds, and any escalation in U.S. tariffs beyond the current 10% incremental rate is not absorbed in guidance

Should You Invest in Under Armour, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Under Armour, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Under Armour, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze UAA stock on TIKR for Free →