Key Stats for Prologis Stock

- 52-Week Range: $103 to $145

- Current Price: $142

- Street Mean Target: $151

- Street High Target: $165

- Analyst Consensus: 10 Buys / 4 Outperforms / 9 Holds / 1 No Opinion

- TIKR Model Target (Dec. 2030): $199

What Happened?

Prologis (PLD), the world’s largest logistics real estate investment trust with 1.3 billion square feet across 20 countries, delivered a record-breaking Q1 2026 that pushed Prologis stock to within striking distance of its 52-week high of $145.44.

The company reported Q1 core FFO (funds from operations, the standard REIT profitability metric) of $1.50 per share, ahead of analyst expectations of $1.49, while revenue came in at $2.30 billion against estimates of $2.21 billion.

Net effective rent change on leases commenced during the quarter hit 31.9%, and occupancy closed at 95.3%, with management raising the full-year average occupancy outlook to 95.00% to 95.75%.

CEO Dan Letter stated on the Q1 2026 earnings call that “we also advanced our data center platform with $1.3 billion of build-to-suit development starts, and we are scaling digital infrastructure and energy to support our next phase of growth,” tying the results directly to what has become the company’s most watched new revenue stream.

Prologis also closed $1.6 billion in new joint venture commitments with Singapore sovereign wealth fund GIC and Canadian pension La Caisse, adding strategic capital partners across U.S. and European logistics, which expands the company’s investment reach without tapping equity markets.

The data center pipeline now stands at 5.6 gigawatts of power either secured or in advanced stages, with 1.3 gigawatts currently under letter of intent, and CFO Tim Arndt confirmed on the earnings call that every megawatt deliverable over the next three years is in active discussion with a hyperscaler customer.

Prologis stock now carries full-year core FFO guidance of $6.07 to $6.23 per share, with the midpoint sitting a penny above consensus at $6.14, and the logistics leasing pipeline has replenished to record highs even after the company logged its best signing quarter on record.

Wall Street’s Take on PLD Stock

Prologis stock enters the back half of 2026 with a leasing inflection that is no longer theoretical: three of the last six quarters have produced all-time records, and the pipeline closed Q1 at new highs despite absorbing 64 million square feet of signings.

At the Q3 2025 actual of $1.54 billion, EBITDA was growing 7.4% year over year, and the Q1 2026 actual at $1.56 billion came in at 6.3% growth, with consensus estimates projecting EBITDA of around $1.67 billion by Q2 2026, representing around 10% growth as occupancy recoveries compound into the rent roll.

Analysts covering PLD stand at 10 Buys, 4 Outperforms, 9 Holds, and 1 No Opinion, with a Wall Street mean price target of $151 and an implied upside of around 6% from current levels; BMO upgraded Prologis stock to Outperform in May with a $162 target, pointing specifically to accelerating FFO growth in 2026 and 2027 driven by improving occupancy and re-leasing spreads.

The target spread runs from $130 to $165, a range that maps almost perfectly onto two distinct views of data center monetization: bears who see logistics recovery as the only real story in near-term earnings, and bulls at BofA who model around $400 million in annual data center sale proceeds over the next five years, growing to over $900 million in the following five-year period.

The embedded lease mark-to-market of 17%, which CFO Tim Arndt quantified as approximately $750 million of NOI at spot rents, means Prologis does not need a single new tenant to grow cash flows: it simply needs existing leases to roll at current market rates.

If logistics recovery stalls or tariff-driven demand uncertainty bleeds into the second half of 2026, re-leasing spreads could compress, slowing same-store NOI growth below the 4.75% to 5.5% guidance range.

The next number to watch is Q2 2026 core FFO per share, where consensus sits at around $1.56; anything at or above that level, combined with a data center vehicle announcement, would close the gap between Prologis stock and the $162 high end of analyst targets.

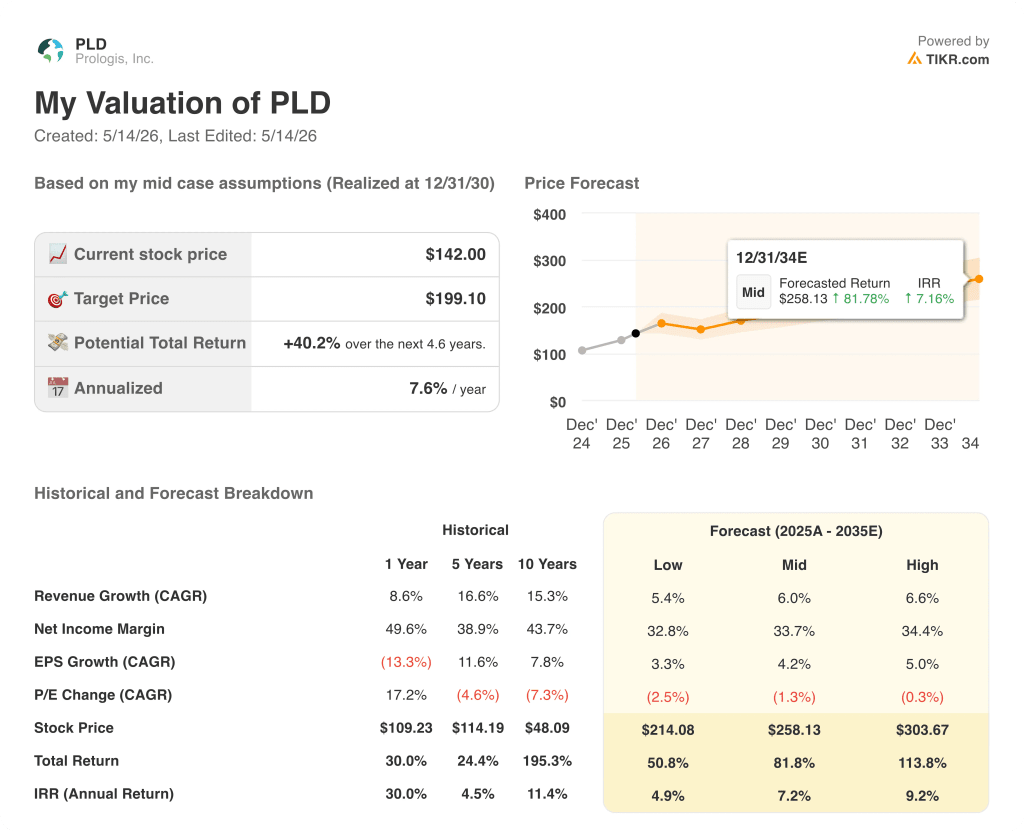

What Does the Valuation Model Say?

The TIKR model prices PLD at a mid-case target of $199.10 by December 2030, assuming a mid-case revenue CAGR of around 6% and net income margins stabilizing around 34%, implying an annualized return of around 7% from the current price of $142.00 and a total potential return of around 40% across the forecast horizon.

At a current price of $142 against a mid-case intrinsic value of $199 and high-case value of $304, with EBITDA growth reaccelerating toward around 10% in 2026 as embedded rent mark-to-market begins flowing through, Prologis stock appears undervalued for patient capital operating on a multi-year time horizon.

The single question this stock hinges on: can Prologis convert its 5.6-gigawatt data center power pipeline into a durable third earnings engine before the market assigns it full value, or will logistics recovery alone carry the stock to fair value at a slower pace?

The Opportunity

- The embedded lease mark-to-market of 17% represents around $750 million of NOI at spot rents, requiring no new leasing to materialize, only time and contract rollovers.

- The data center pipeline, even under a conservative power shell format at $3 million per megawatt, represents a potential investment base exceeding $15 billion, and BofA models data center sale proceeds reaching over $900 million annually within 10 years.

- Prologis raised development start guidance to $4.5 billion to $5.5 billion for 2026, with around 40% allocated to data center build-to-suits, giving the earnings mix a higher-margin tilt going forward.

- Three all-time leasing records in the past six quarters, a replenished proposal pipeline at new highs, and large-format space 98% leased globally point to an occupancy recovery that is structurally underway, not cyclically manufactured.

- The A2/A-rated balance sheet with $6.7 billion in liquidity and 4.8x debt to adjusted EBITDA gives Prologis the financial firepower to execute this build-out without equity dilution.

The Risk

- Southern California, which represents approximately 20% of the portfolio, is still moving through its bottoming process with vacancy yet to definitively peak, creating a drag on U.S. same-store growth metrics through at least the first half of 2027.

- The data center vehicle structure remains unannounced, and until the capitalization format is confirmed, roughly $15 billion in potential pipeline value sits in a strategic grey zone that the stock cannot fully price.

- Consensus EBITDA estimates show growth decelerating from around 10% in mid-2026 back toward around 5% by mid-2027, meaning the window for multiple expansion is narrow if the data center narrative does not crystallize in the next one to two quarters.

Should You Invest in Prologis, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Prologis, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Prologis, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PLD stock on TIKR for Free →