Key Stats for Capital One Stock

- Current Price: $183.71

- Street Mean Target: ~$207

- TIKR Target Price (Mid): ~$308

- TIKR Annualized IRR (Mid): ~12% per year

- Q1 2026 Total Net Revenue: $15.23B (up ~58% YoY, mostly Discover)

- Q1 2026 Adjusted EPS: $4.42 (missed $4.51 estimate)

- Domestic Card Charge-Off Rate: 5.1% (down 109 bps YoY)

- CET1 Capital Ratio: 14.4%

Value your favorite stocks like COF with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

Why GAAP Net Income Fell 80% While the Underlying Business Grew

Capital One (COF) operates as a bank holding company providing credit cards, auto loans, and consumer banking services. It completed the acquisition of Discover Financial in 2026, making it the largest credit card issuer in the US by purchase volume and, more importantly, giving it direct ownership of its own payment network rather than relying on Visa or Mastercard to process transactions.

That distinction matters enormously for the long-term thesis. Owning the rails means keeping more of the interchange economics on every transaction that runs through the Discover network. But getting there has been expensive, and the GAAP results have reflected every dollar of that cost.

Net income tells the story of the transition. Capital One earned $12.39 billion in 2021, rode post-pandemic spending strength, and then watched earnings decline every year as credit costs normalized, funding costs rose with interest rates, and Discover integration expenses piled up. By 2025, GAAP net income had fallen to $2.45 billion. That is an 80% decline over four years in a company that actually grew significantly.

The important context is that normalized earnings stripped of acquisition-related adjustments look very different. Adjusted EPS of $4.42 in Q1 2026 implies roughly $6 to $7 billion in annualized earning power once you exclude the purchase accounting, intangible amortization, and integration costs that flow through GAAP. The gap between GAAP-reported results and what the business actually earns on a run-rate basis is the central thing to understand about Capital One right now.

See analysts’ growth forecasts and price targets for COF stock (It’s free!) >>>

What Analysts Think About COF After the Q1 Miss

Q1 2026 results were mixed on the surface. Revenue of $15.23 billion beat the prior year by 58%, though most of that jump came from adding Discover’s loan book and related revenue. Excluding Discover, underlying revenue grew about 7%. Adjusted EPS of $4.42 missed the $4.51 consensus by roughly 2%, which sent the stock lower after hours.

Street consensus sits around $207, implying modest upside from the current price. Most analysts remain constructive, viewing the miss as integration noise rather than a signal that the underlying business is deteriorating. CEO Richard Fairbank was direct on the call: “Our results in the first quarter reflect solid top-line growth and strong credit performance. The Discover integration continues to go well, and we continue to build momentum from this game-changing acquisition.”

The integration timeline targets completion by the first half of 2027. Until then, results will continue to include adjustments that make quarter-to-quarter comparisons difficult.

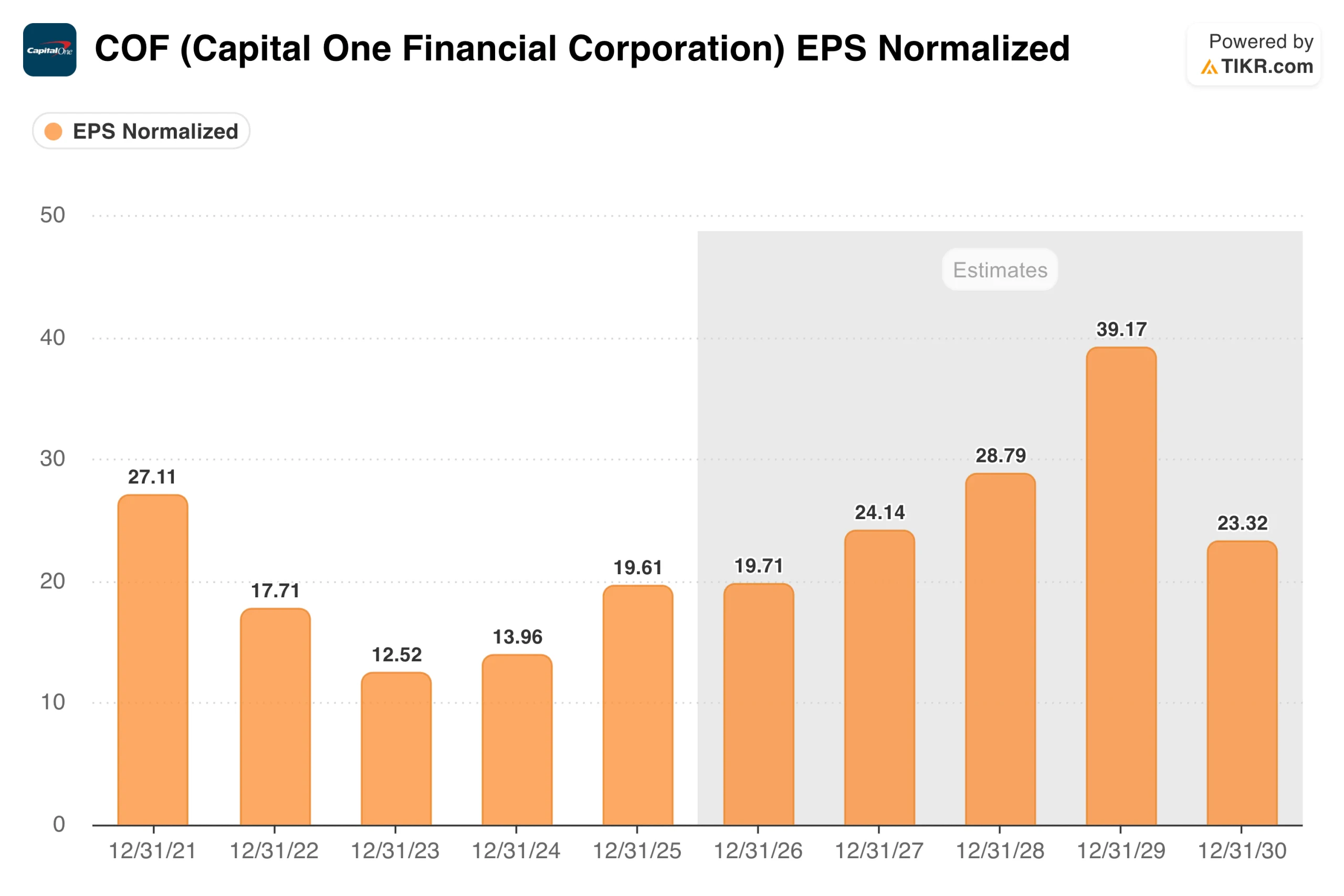

What the EPS Recovery Timeline Looks Like

Normalized EPS peaked at $27.11 in 2021, compressed through 2023 as credit costs rose and the business digested the rate environment, then began to recover: $13.96 in 2024 and $19.61 in 2025. Consensus then projects around $20 in 2026, with integration costs remaining elevated, stepping up meaningfully to around $24 in 2027 and around $29 in 2028 as synergies materialize and charge-offs continue to normalize.

The 2026-to-2027 step is the key inflection to watch. That is where the expense synergies from the Discover technology conversion are expected to start flowing through, and where the domestic card charge-off rate, which has already improved 109 basis points year over year, should normalize further.

If that happens on the timeline management has laid out, the EPS acceleration becomes real, and the current stock price looks like it is pricing in a scenario that is more pessimistic than the data supports.

Value COF instantly (Free with TIKR) >>>

What the TIKR Model Implies at the Current Price

The TIKR model targets around $308 in the mid-case, implying a total return of roughly 68% over about 4.6 years, or about 12% annually.

The model uses revenue growth of around 6% per year, which is roughly in line with Capital One’s underlying growth rate excluding the Discover acquisition bump. Net income margins of around 21% reflect normalized profitability as integration costs fade. EPS growth of around 7% annually captures steady compounding as the combined company reaches steady state.

The low case targets around $314 at roughly 6% per year. The high case reaches around $412. The range of outcomes is wide, which is typical for a company in the middle of a major integration and a credit cycle, but even the low end implies meaningful upside from the current price.

The Case for COF: Network Economics, Direct Rails, and a Credit Cycle in Progress

The Discover network is the long-term value driver that neither of the prior articles fully quantified. When Capital One routes transactions through the Discover network rather than Visa or Mastercard, it keeps the interchange fees that would otherwise go to the network. At Capital One, transaction volume is a structurally higher-margin business. It takes time to convert cardholders and merchants, which is exactly what management is working through right now.

The domestic card charge-off rate has been improving steadily. Down 109 basis points year over year in Q1 2026 is a meaningful move. Charge-offs were the primary reason the market lost confidence in Capital One’s earnings power, and their directional improvement matters more than any single quarter’s adjusted EPS figure.

Capital One also just completed the acquisition of Brex for around $4.5 billion, adding a commercial payments platform that extends the network’s reach into business spending. It adds near-term integration complexity, but it expands the addressable market.

The Risks: Charge-Offs, Integration Complexity, and a Wide Range of Outcomes

Credit quality is the variable that matters most. If the domestic charge-off rate stops improving or re-accelerates on a weaker consumer backdrop, the EPS recovery timeline slips, and the earnings assumptions in any model are quickly revised lower. Consumer credit is more sensitive to economic conditions than most investors appreciate until it moves against them.

The integration has a deadline: the first half of 2027. Every quarter between now and then will include acquisition-related adjustments that obscure the underlying earnings picture. That creates ongoing volatility and makes it harder to read the fundamentals clearly.

And the Brex acquisition, closed just after Q1, adds another layer. Managing three large integrations simultaneously while maintaining credit discipline is a high-execution-risk environment for any management team.

Is COF Worth Buying at $184?

Capital One is not a straightforward stock to evaluate right now. The GAAP numbers look like a business in serious trouble. The normalized numbers look like a business in the middle of a costly but strategically sound transformation. Figuring out which frame is more accurate is the work.

What the data does show: charge-offs are improving, the Discover conversion is progressing on schedule, and management has not walked back its earnings power expectations on the other side of the integration. The TIKR mid-case of around $308 at roughly 12% per year reflects a scenario where the integration executes as described, and the credit cycle cooperates. That is a lot of things to go right, which is why the stock trades where it does.

For investors who are willing to do the work and hold through the noise, the current price offers a wide margin between where the stock sits and where the model says it could go. Whether the integration delivers is ultimately the question that determines if that gap closes.

See analysts’ growth forecasts and price targets for COF stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!