Key Stats

- Current Price: $102 (May 13, 2026)

- Q3 FY2026 Revenue: $15.8B, up 12% YoY

- Q3 FY2026 Non-GAAP EPS: $1.06, up 10% YoY

- Q3 FY2026 Non-GAAP Net Income: $4.2B, up 10% YoY

- FY2026 Revenue Guidance: $62.8B to $63B

- FY2026 Non-GAAP EPS Guidance: $4.27 to $4.29

- Q4 FY2026 Revenue Guidance: $16.7B to $16.9B

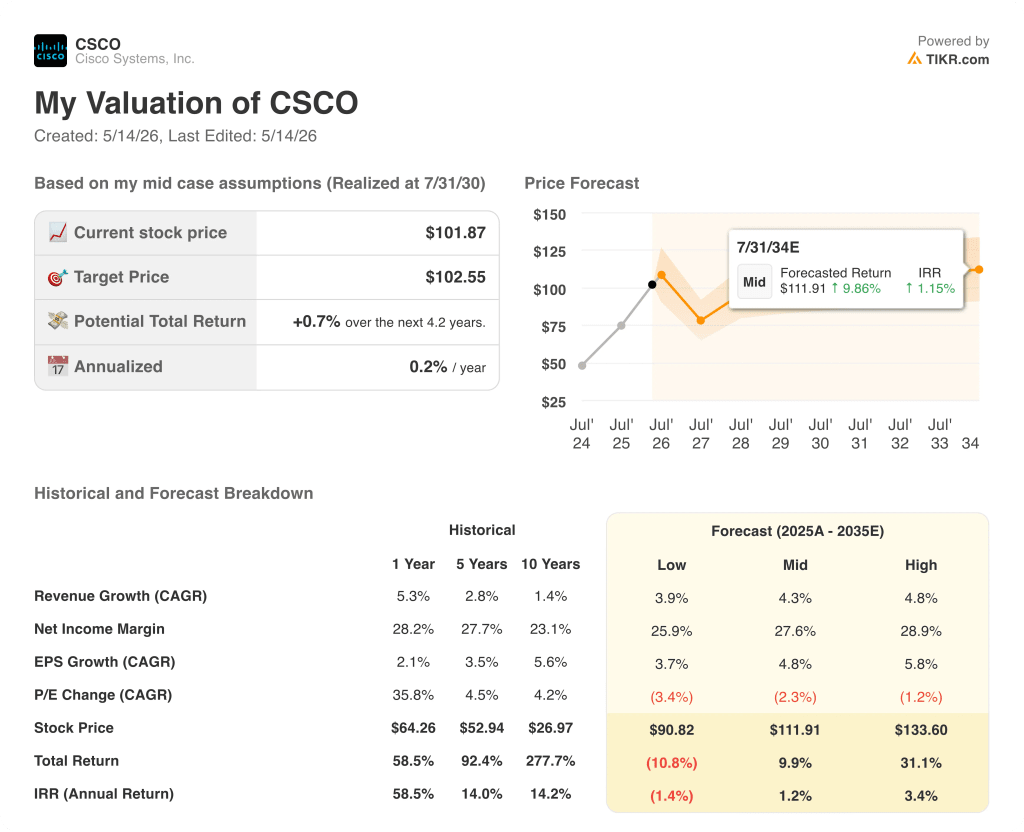

- TIKR Model Price Target (Mid): $112

- Implied Upside: ~10%

Cisco Stock Posts Record Revenue as AI Infrastructure Orders Triple

Cisco Systems (CSCO) delivered record Q3 FY2026 revenue of $15.8B, up 12% year-over-year, with non-GAAP EPS of $1.06, up 10%, both above the high end of guidance.

Product revenue of $12.1B grew 17%, led by networking, which accelerated to 25% growth driven by AI infrastructure buildout and campus refresh demand.

Total product orders surged 35% year-over-year, with hyperscaler orders growing triple digits and non-hyperscaler orders up 19%.

AI infrastructure orders from hyperscalers reached $1.9B in Q3, up from $600M a year earlier, with 5 of the top hyperscalers each growing in triple digits, according to Chuck Robbins, Chair and CEO, on the Q3 FY2026 earnings call.

Year-to-date hyperscaler AI infrastructure orders totaled $5.3B, already surpassing Cisco’s prior full-year expectation of $5B, and the company now expects approximately $9B in total AI hyperscaler orders for FY2026, or roughly 4.5x FY2025’s total, according to Robbins on the Q3 earnings call.

Cisco also expects to recognize approximately $4B in AI infrastructure revenue from hyperscalers in FY2026, according to Robbins.

Acacia, Cisco’s coherent pluggable optics business, had its strongest quarter on record with over $1B in Q3 orders and is on track to grow more than 200% year-over-year in FY2026, according to Robbins.

Campus networking set a quarterly order record, growing more than 25% year-over-year, with wireless orders up more than 40% and WiFi 7 representing half the wireless mix.

Security, excluding Splunk, saw double-digit order growth, though revenue was flat as legacy product declines offset new portfolio growth. The Splunk business continued its cloud subscription transition, creating a near-term revenue drag that management expects to persist into Q4.

Non-GAAP gross margin came in at 66%, down about 3 percentage points year-over-year, with the product gross margin decline driven primarily by unfavorable mix from accelerating hardware shipments and elevated memory costs, partially offset by productivity programs, according to CFO Mark Patterson on the Q3 earnings call.

Q4 FY2026 revenue guidance was set at $16.7B to $16.9B, representing approximately 14% year-over-year growth at the midpoint, with non-GAAP EPS guided to $1.16 to $1.18, up more than 10% at the midpoint.

For full-year FY2026, Cisco raised its revenue guidance to $62.8B to $63B and non-GAAP EPS guidance to $4.27 to $4.29.

Cisco also announced a restructuring plan to reallocate resources toward silicon, optics, security, and AI, with up to $1B in pretax charges expected, with $450M recognized in Q4 FY2026 and the remainder in FY2027.

The company returned $2.9B to shareholders in Q3, consisting of $1.7B in dividends and $1.3B in buybacks, bringing the year-to-date total to over $9B returned.

Cisco Systems Stock: Financials

Cisco Systems stock is delivering an operating leverage story: revenue is recovering sharply from a prolonged trough while cost discipline is converting that top-line growth into expanding operating income.

Revenue bottomed at $12.7B in the April 2024 quarter, when growth was down 13% year-over-year, and has climbed each quarter since, reaching $15.35B in the January 2026 quarter with 9.7% year-over-year growth.

Gross margin has held in a 63% to 66% range across that recovery, dipping to 63% in the July 2025 quarter before recovering to 65% in January 2026.

Operating income has risen sharply from a trough of $2.65B in July 2024 to $3.82B in January 2026, with the operating margin expanding from 19% to 25% over that same span.

The operating margin trajectory on the income statement aligns with what Patterson described on the call: a sustained focus on driving operating leverage even as gross margin faces mix and memory headwinds, with OpEx declining from 34% of revenue a year ago to 32% in the most recent reported quarter.

What Does the Valuation Model Say?

The TIKR mid-case model prices Cisco Systems stock at $112, implying roughly 10% upside from the current price of $102, based on a 4.3% revenue CAGR, a 28% net income margin, and a 4.8% EPS CAGR through 2035.

The model assumes modest P/E multiple compression of about 2.3% annually, which is the load-bearing assumption: the mid-case is not pricing in a structural re-rating from AI infrastructure exposure, only that Cisco’s earnings grow steadily while the multiple drifts slightly lower.

The investment case for Cisco Systems stock is stronger after this report than before it, not because the valuation gap is wide at current prices, but because the earnings growth trajectory is now substantially better-defined through FY2026 and the early indications for FY2027 AI hyperscaler revenue suggest at least $6B.

The earnings report is structurally strong, but whether Cisco Systems stock re-rates depends on whether AI infrastructure revenue growth is durable past FY2026 or concentrated in a window of hyperscaler buildout.

What Has to Go Right

- Hyperscaler AI orders of approximately $9B in FY2026 and at least $6B in expected FY2027 revenue recognition must convert to bookings without material slippage or cancellation.

- The five Silicon One design wins across two P200 scale-across hyperscalers, and a third win already confirmed in Q4, must expand into full-scale orders as next-generation deployments ramp in FY2027.

- Gross margin stabilization at approximately 66%, supported by 20-plus memory reduction programs and DDR4-to-DDR5 conversions, must hold even as hardware mix grows and memory costs remain elevated.

- Campus networking, up 25% in Q3 orders and with wireless orders at a record high, must sustain refresh demand through a multiyear cycle that Robbins described as still in early innings.

What Could Still Go Wrong

- The 3-percentage-point gross margin decline year-over-year is primarily mix-driven as hardware accelerates. If the AI infrastructure product mix continues to weigh on product gross margins, the company’s ability to hold 34% operating margins will require persistent OpEx discipline.

- Security revenue remains flat despite double-digit order growth in the refreshed portfolio, as Splunk’s on-premise-to-cloud transition creates a compounding near-term drag that management has not yet quantified in revenue terms for FY2027.

- The 19% non-hyperscaler order acceleration in Q3 included an estimated 4 to 5 percentage points from price increases, according to Patterson, meaning underlying volume growth was closer to 14% and the sustainability of that rate through tougher FY2027 comps is untested.

- A restructuring charge of up to $1B, with $450M landing in Q4 FY2026, adds noise to near-term GAAP results and introduces execution risk in the resource reallocation.

Should You Invest in Cisco Systems, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Cisco Systems stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Cisco Systems stock alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CSCO stock on TIKR for Free →