Key Takeaways:

- Bloom Energy (BE) delivered Q1 fiscal 2026 revenue of $751 million, up 130.4% year-over-year, and subsequently raised its full-year 2026 revenue growth outlook.

- The company expanded its Oracle partnership in April 2026, targeting the deployment of up to 2.8 gigawatts of fuel cell capacity for AI data center infrastructure.

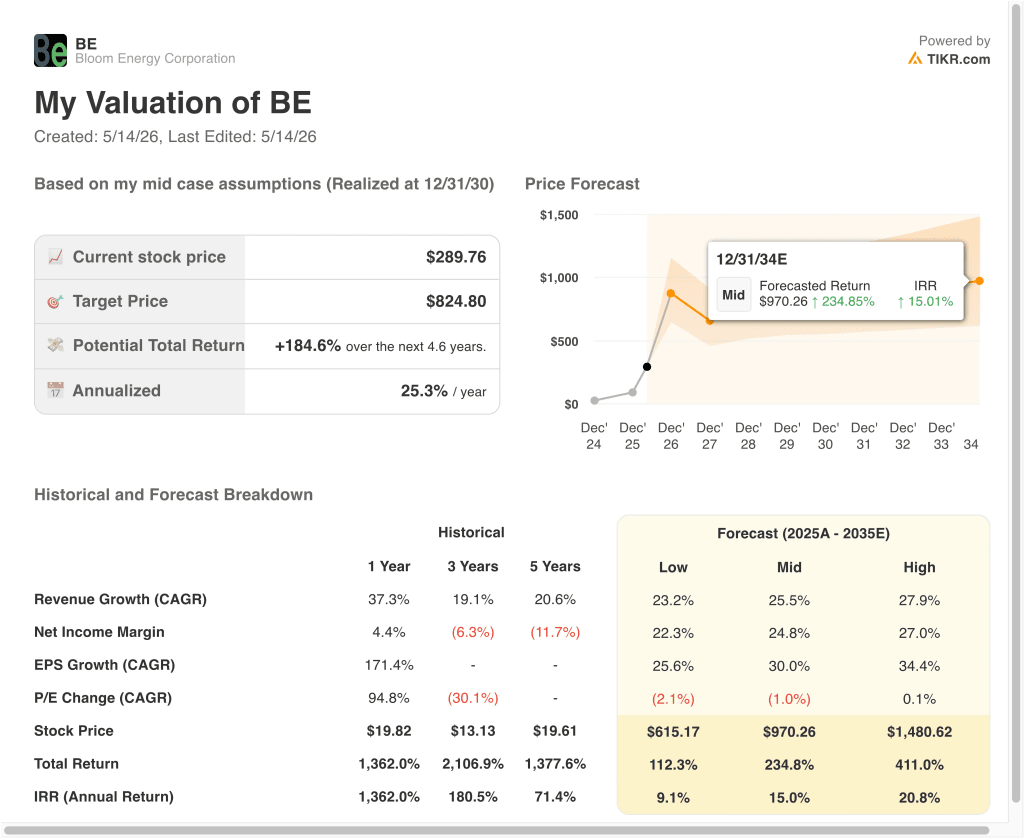

- BE stock could reasonably reach around $825 per share by December 2030, based on our valuation assumptions.

- This implies a total return of around 185% from today’s price of $290, with an annualized return of 25.3% over the next 4.6 years.

What Happened?

Bloom Energy Corporation (BE) has become one of the most dramatic market stories of the past year. The stock surged over 1,400%, fueled by explosive AI data center demand for clean, on-site power. These solid oxide fuel cell systems generate electricity directly from natural gas or hydrogen without combustion, bypassing the traditional utility grid.

So data center operators favor this technology because it delivers reliable power exactly where it is needed, without waiting for utility grid connections. The company reported Q1 fiscal 2026 revenue of $751 million, up 130.4% year-over-year, and net income of $70.7 million. And management subsequently raised its full-year 2026 revenue growth guidance.

The biggest single catalyst was Bloom’s expanded partnership with Oracle. In April 2026, the two companies announced plans to deploy up to 2.8 gigawatts of fuel cell systems to power Oracle’s AI computing infrastructure. A gigawatt is roughly the power output of a large conventional power plant, so 2.8 GW is an enormous commitment.

But investors should also note that several insiders sold meaningful quantities of shares in April and May 2026, including the COO, CLO, and a board director. The current street consensus price target of $237 sits notably below the current price of around $290, so analysts broadly view the stock as fully valued after its extraordinary run.

The broader AI infrastructure buildout continues to accelerate. SanDisk joined Western Digital and Seagate in May 2026 to signal strong AI-driven demand across storage and power. But Bloom specifically benefits because data centers increasingly need power that bypasses congested utility grids.

Here’s why Bloom Energy stock could still deliver strong long-term returns if its AI infrastructure partnerships scale as planned, but near-term buyers face limited upside at current prices.

What the Model Says for BE Stock

We analyzed the upside potential for Bloom Energy stock based on its expanding AI data center fuel cell deployments, growing Oracle and hyperscaler partnerships, and improving operating margin profile as production volumes scale.

Based on estimates of 37.3% annual revenue growth, 10.0% operating margins, and a normalized P/E multiple of 125.6x, the model projects Bloom Energy stock could rise from $290 to around $322 per share.

That would be an 11% total return, or a 4% annualized return over the next 2.6 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for BE stock:

1. Revenue Growth: 37.3%

Bloom Energy’s revenue jumped 130.4% in Q1 fiscal 2026, reflecting rapid fuel cell deployment across AI data center customers. The Oracle deal alone targets up to 2.8 GW of capacity, so the committed pipeline is substantial. And the broader trend of data centers seeking grid-bypass power solutions is accelerating across the industry.

But sustaining triple-digit growth is inherently difficult, and project-based revenue can be lumpy quarter to quarter. Based on analysts’ consensus estimates, we used a 37.3% revenue growth forecast, reflecting the company’s expanding backlog while acknowledging execution risk at this scale.

The one-year historical revenue CAGR of 37.3% also provides a reasonable forward anchor, since AI infrastructure demand shows no sign of slowing in the near term.

2. Operating Margins: 10%

Bloom Energy’s LTM EBIT margin of 7.3% reflects a business still scaling its manufacturing capacity and sales infrastructure. Gross margin of 30.1% shows improving unit economics, but operating expenses remain elevated because the company is investing heavily in engineering and production capacity.

Based on analysts’ consensus estimates, we used a 10.0% operating margin target, reflecting expected improvement as Bloom increases production volumes and begins leveraging its cost structure. But achieving this target will require sustained revenue growth and disciplined cost management.

This target margin also acknowledges that Bloom has historically operated with near-zero or negative operating margins, and the pathway to sustainable double-digit margins is not without execution risk.

3. Exit P/E Multiple: 125.6x

Bloom Energy currently trades at a forward P/E of around 126x, which is an extraordinary multiple by any traditional standard. It reflects market expectations that earnings will grow very rapidly as AI fuel cell deployments scale and margins improve significantly over the coming years.

Based on analysts’ consensus estimates, we maintained a 125.6x exit P/E, acknowledging that this is a growth-stage valuation and that any slowdown in AI infrastructure spending could compress this multiple significantly.

So near-term buyers are effectively paying for a long-term earnings trajectory that has not yet materialized at scale, which is the central risk at current prices.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for BE stock through 2034 show varied outcomes based on AI data center deployment pace, operating margin improvement, and competitive dynamics in the energy infrastructure market (these are estimates, not guaranteed returns):

- Low Case: Slower AI deployments and margin headwinds limit earnings growth → 9.1% annual returns

- Mid Case: Oracle and hyperscaler partnerships scale as expected, and margins improve steadily → 15.0% annual returns

- High Case: Rapid hyperscaler adoption and significant margin expansion drive faster earnings growth → 20.8% annual returns

Going forward, Bloom Energy’s stock performance will hinge on whether its large AI infrastructure commitments translate into consistent, growing revenue. The near-term model implies only a 4% annualized return from current prices, so the stock is not cheap on a short-term basis.

But investors with a longer horizon who believe the AI energy infrastructure buildout is still in its early stages may find the mid and high case scenarios compelling through 2034.

See what analysts think about BE stock right now (Free with TIKR) >>>

Should You Invest in Bloom Energy Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up BE, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track BE alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze the stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!